#SPX1dte Sold to Open $SPX Dec 11th 3585/3605-3720/3740 iron condors for .90, SPX at 3671, IV 13.8%, deltas -.06,+.06

Daily Archives: Thursday, December 10, 2020

Diagonal Back Spread – SBUX

Sell 1 x Jan 21 $105 call, Buy 2 x Apr 16 $110 call @ $5.64 debit.

Test case for how this setup performs over time. Ideally looking for structuring the trade so the sale of call finances all, or most of, the cost of the 2 long calls (McMillan thinks it is possible) – but I’m not too sure.

SPX 7-dte

#SPX7dteLong – Bought to Open $SPX Dec 16th 3640/3660-3670/3690 iron condors for 16.65, with SPX at 3663.

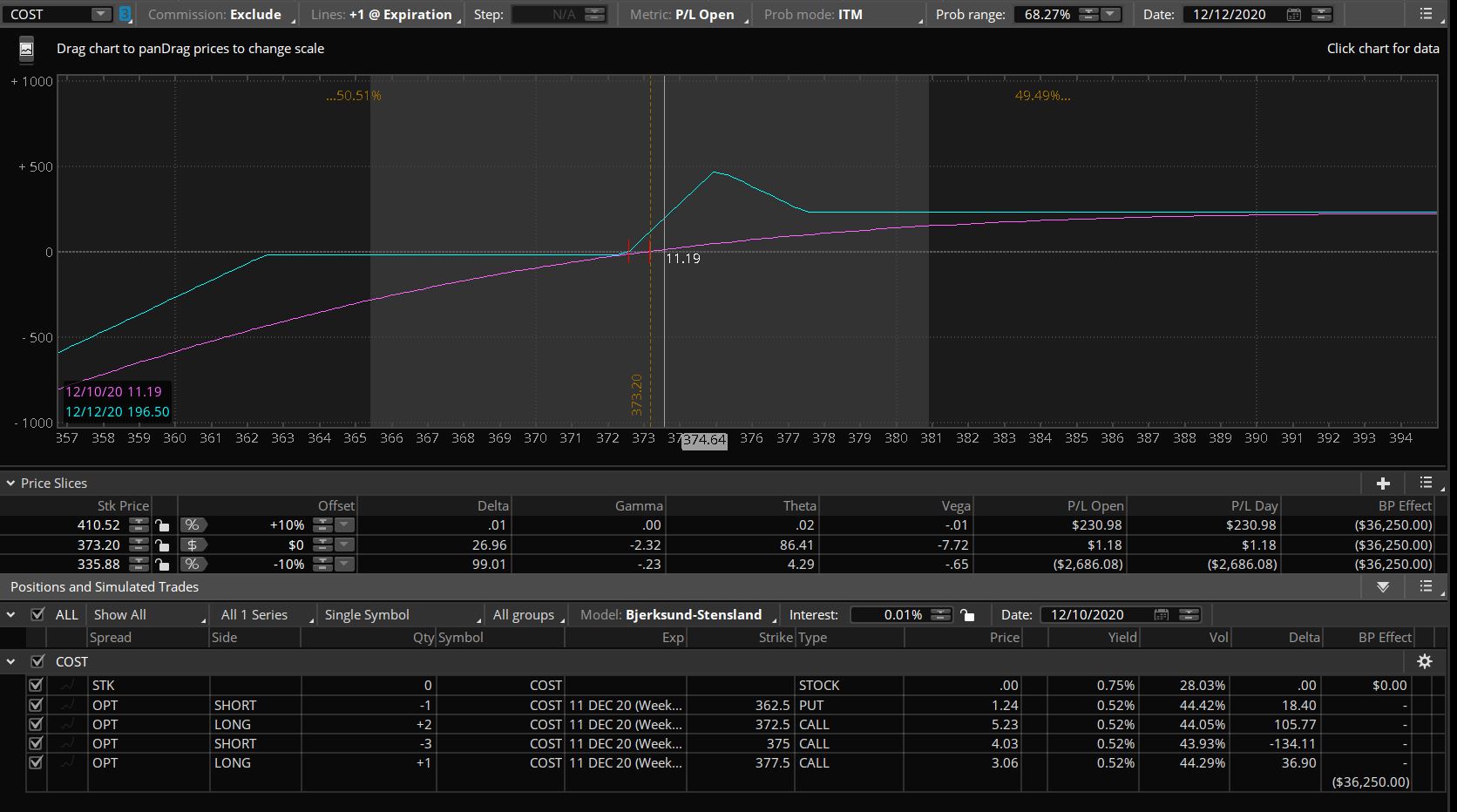

COST #earnings Here’s a trade…

COST #earnings

Here’s a trade I just executed very similar to CHWY. Uses call skew for bullish play, financed by a short put, no upside risk, downside BE is about $362.60, right at expected move. Traded small for assignment. On these trades the T1 line can rise above the max P/L line, if the stock price is close to, but below, the call fly. So on a down move it’s important to be nimble for an advantageous close.

Dec 11 Expiration

Call Skew Fly: 2/3/1 372.5/375/377.5 for 1.43 debit

Short Put: 362.5 $1.24 cr

MRNA

Still has a high IVR. Sold next week’s 210 call for 1.75 to pair with my Jan 110 put. My Dec11 210 and 220 calls should expire worthless tomorrow.

RH

#ShortCalls – Selling against a couple short puts I’ve got floating around out there. Giving Mr. Market something to shoot for…

Sold RH DEC 18 2020 485.0 Call @ 2.35

RH Post Earnings

#ShortPuts – Selling outside the expected move and below the 50ma down near recent lows…

Sold RH DEC 31 2020 375.0 Put @ 4.00

VXX Contango special result

11/24 Bought to Open VXX Jun 18 2021 8.0 Puts / Sold VXX Dec 04 2020 17.0 Puts @ 0.06 Credit.

12/04 Bought to close VXX Dec 04 2020 17 Puts at $0.02. Rolled to VXX Dec 11 2020 16 Puts at $0.10.

Today covered the VXX Dec 11 2020 16 Puts at $0.01.

They won’t trade any lower.

Adding the now “Free” VXX June 2021 puts to my growing portfolio of these with 190 Days to expiration (DTE)