If anyone has covered calls on TSLA, there may be a little extra assignment risk if your extrinsic value is low on the short calls. Check it out before the close. Earlier this week I converted my TSLA Jade Lizard (took nice profits) to a collar, so I’m watching the extrinsic on the short call. I’m in the clear, but if anyone is DITM with low extrinsic left (regardless of expiration date) there is great demand for the shares.

Author Archives: smasty

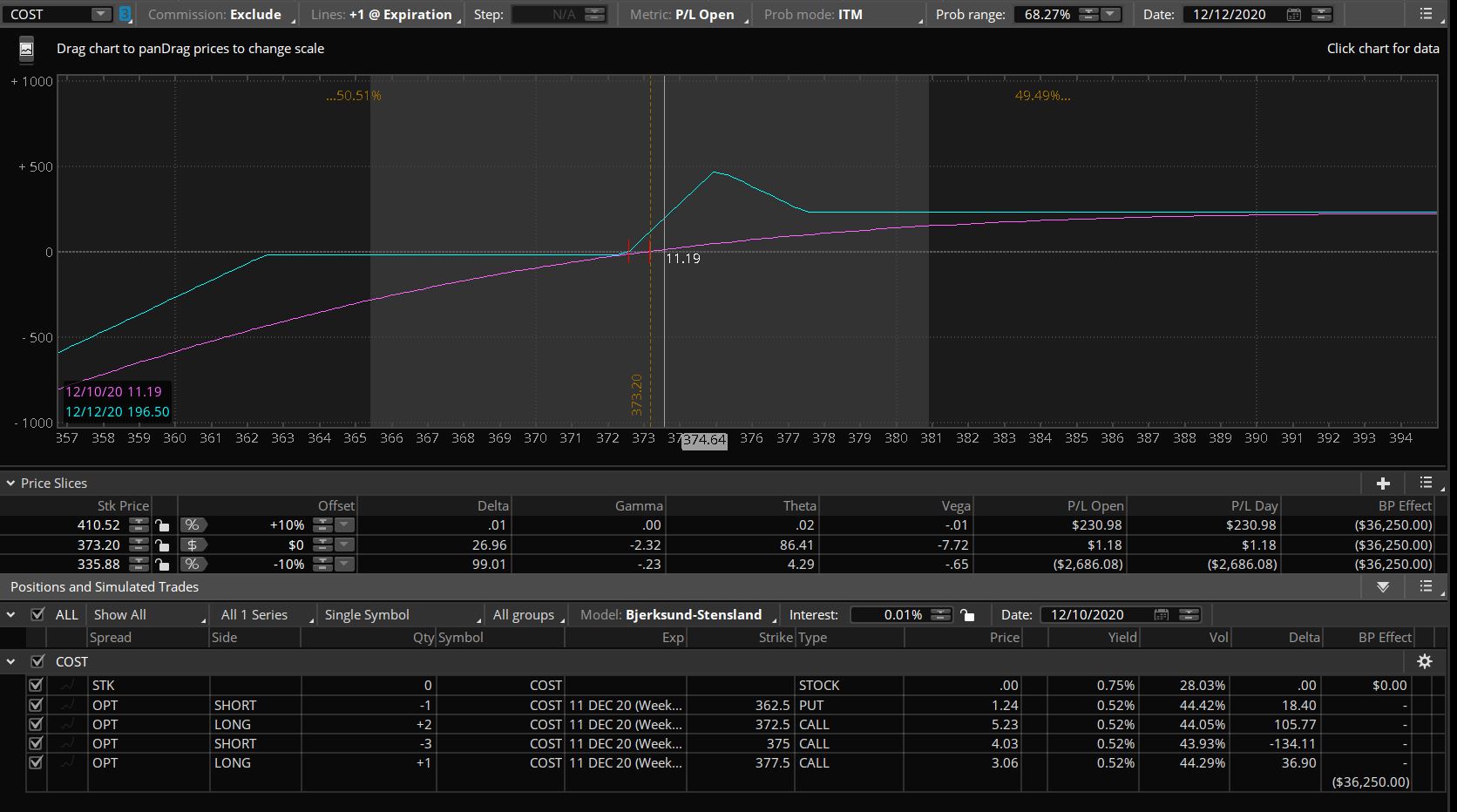

COST #earnings Here’s a trade…

COST #earnings

Here’s a trade I just executed very similar to CHWY. Uses call skew for bullish play, financed by a short put, no upside risk, downside BE is about $362.60, right at expected move. Traded small for assignment. On these trades the T1 line can rise above the max P/L line, if the stock price is close to, but below, the call fly. So on a down move it’s important to be nimble for an advantageous close.

Dec 11 Expiration

Call Skew Fly: 2/3/1 372.5/375/377.5 for 1.43 debit

Short Put: 362.5 $1.24 cr

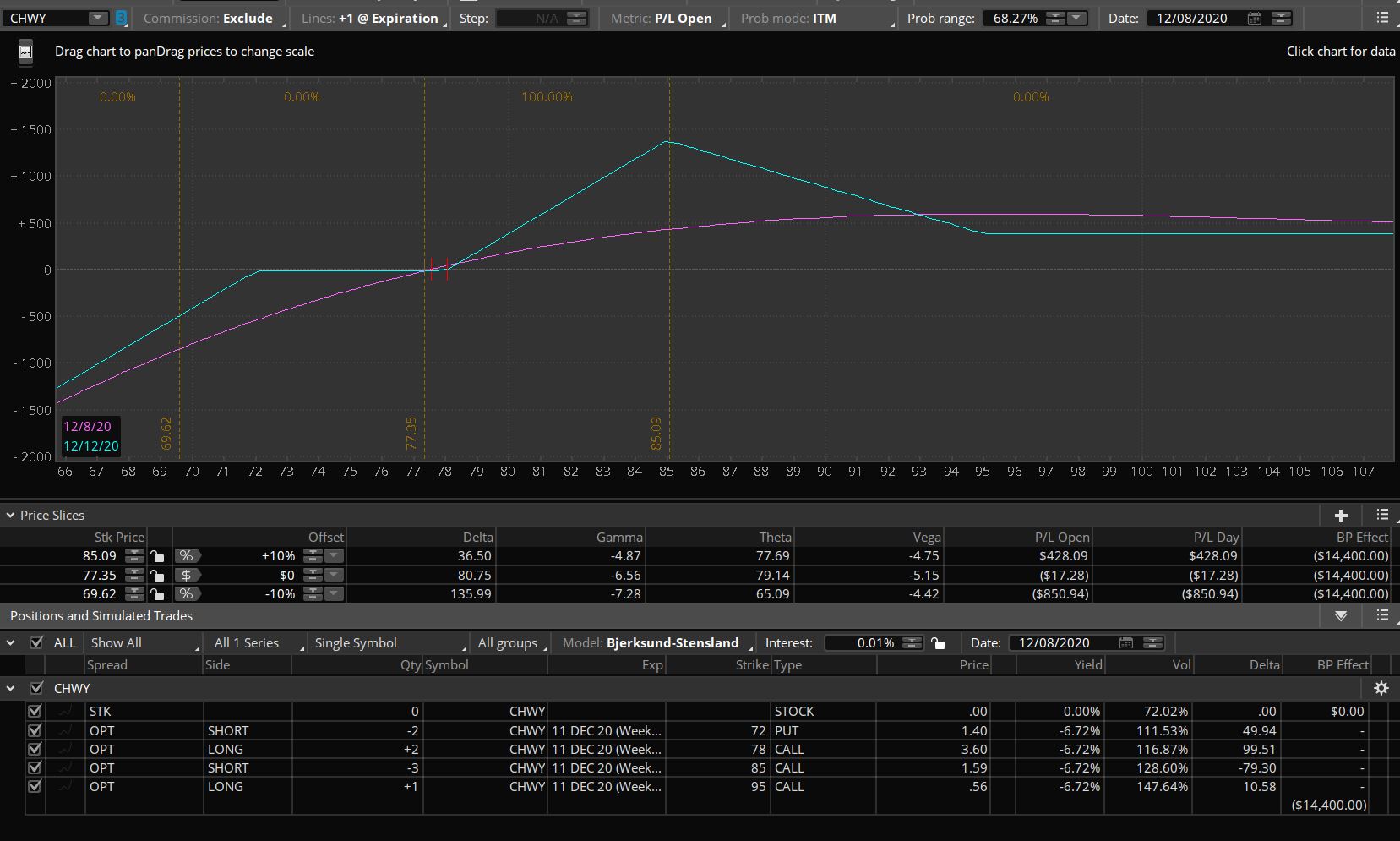

CHWY #earnings I’m bullish, there’s…

CHWY #earnings

I’m bullish, there’s big call skew in this ticker. I’ve been having good success orienting unbalanced flies to take advantage of the skew. Market Mindset on TT has been talking about this a lot too, with their “broken heart” trade. Admittedly I usually position earnings for way more downside room, so we’ll see how this goes.

So here’s my executed trade for earnings:

Dec 11

Skew Fly (with net 4.42 volatility edge, found via vol sum):

Bought qty 2 78 call

Sold Qty 3 85 call

Bought qty 1 95 call

Net Debit 2.99

For finance:

Sold qty 2 72 put @ 1.40

No upside risk, downside risk is assignment of 200 shares

TSLA #jadelizard Put Rollup: Original…

TSLA #jadelizard

Put Rollup:

Original trade on Nov 23

Sold qty 1 380 put (Jan 15)

Sold qty 1 740 call (Jan 15)

Bought qty 1 750 call (Jan 15)

Net Cr 9.80

Adjustment today: rolled up the put

Bought to close $380 put for 5.15, orig sold for $9.00

Sold to open $430 put for $8.85

Doubles my delta, removes all upside risk, lower breakeven moves from $370 to $416

TSLA #jadelizard My Dec TSLA…

TSLA #jadelizard

My Dec TSLA Jade came off this morning for 50% profit, here’s a Jan reset:

$380 put (sell)/$740 call (sell)/$750 call (buy) $9.80 credit. $9.80 cr on a $10-wide call spread leaves $20 net risk to upside. BE delta is 9 on the downside. Basically risk free to upside.

Happy Thanksgiving!

Sue

DKNG Anatomy of a Trade

Here’s a Tasty Trade segment done today on how they managed the swings in DKNG to a profit, I thought it was a really good example of “what can be done” with a crazy stock. I’ve got DKNG collared, and am not quite net-profitable on it after the big drop, but I have (and continue to) collected a lot on the short hedges.

Sue

https://tastytrade.com/tt/shows/market-mindset?_sp=f133318e-0cd5-4c2d-a1bb-31c2e60b16b0.1605556482468

Collar Course Recommendation

Hi Everyone! Big winter storm bearing down on us here in Denver. The last time I remember a snow on Sep 8 was about 22 years ago, I was working for a dot-com startup that went public with a billion $ and lost it all. Another thing that happened over 20 years ago was that I was a subscriber to Power Options. I know that because I purchased a course from them a couple weeks ago and had to update my address on the platform….an address over 20 years old in the pacific northwest.

So, I just love collars, and have found several different ways to structure them, as you know. But….I can’t even begin to tally up the amount of $$$ I lost on the collar ceilings in the last quarter. TSLA, AAPL, NVDA, PTON, ROKU, even JNJ. I stumbled onto “The Blueprint” course at Power Options and decided to take the plunge. It’s $339 I think. I am super enjoying the course though, well worth the money. There is so much nuance and depth to collar structures—one might think them simple, pedestrian–but there are layers and layers of beautiful complexity to them. This one (Blueprint) uses very long term (5+ months) and very DITM puts for the married put portion. (Think, a long term $120 put on a $100 stock guarantees a $120 sell price—the only risk in the position is the extrinsic above the strike. The positions start off with no ceiling limitations, just significant downside protection from a higher stock price). Then they have 12 various income methods to cover that extrinsic risk, thus yielding a “bulletproof” position. The income methods—some are obvious, but many are VERY unique in the management of this type of position. Then the course originator (Radioactive Trading, which has partnered w/ Power Options) has hours and hours of highly informative webinars that further train and explain application of the income methods.

Power Options has developed into a pretty robust scanning platform. They have a cool list for covered calls called the “7/11” list. The companies on the scan provide covered call ops with at least 7% return on assignment and at least 11% downside protection. I started using the 7/11 list for collar candidates. WKHS, posted by @honkhonk81 this week is on the list, so I put a collar on it this week.

Along w/ purchasing the Blueprint course Power Options gave me 6 weeks of free trial.

Geez, I know this sounds like an advertisement, but NO affiliation, not looking for any referral credits here….just passing along a good thing, worth the price. The Radioactive Trading site probably has free videos to review if interested.

Sue

EWZ

KODK

EWZ Roll: I’m following along w/ @winstonthink ‘s ITM strangle leap w/ weekly straddle sales. I think you guys are calling these #diagonalbutterfly ‘s I’m rolling the weekly straddles at 50% profit.

Core Strangle Leap: Jan 2022 27 call/37 put @ $16.72. Max risk on a 1-lot is $672

Straddle 1 Aug 7 32’s sold at $1.40, covered at $.70 ($70)

Straddle 2 Aug 14 32’s sold at 1.60 covered at $.80 ($80)

Straddle 3 Aug 21 31.5’s sold at 1.50 today

Once $672 profit is realized on the straddles I will add a 2nd leap strangle. My objective is to get to a ratio sell situation where there is always more net long contracts than short, for a beneficial long vega position where all risk has been covered.

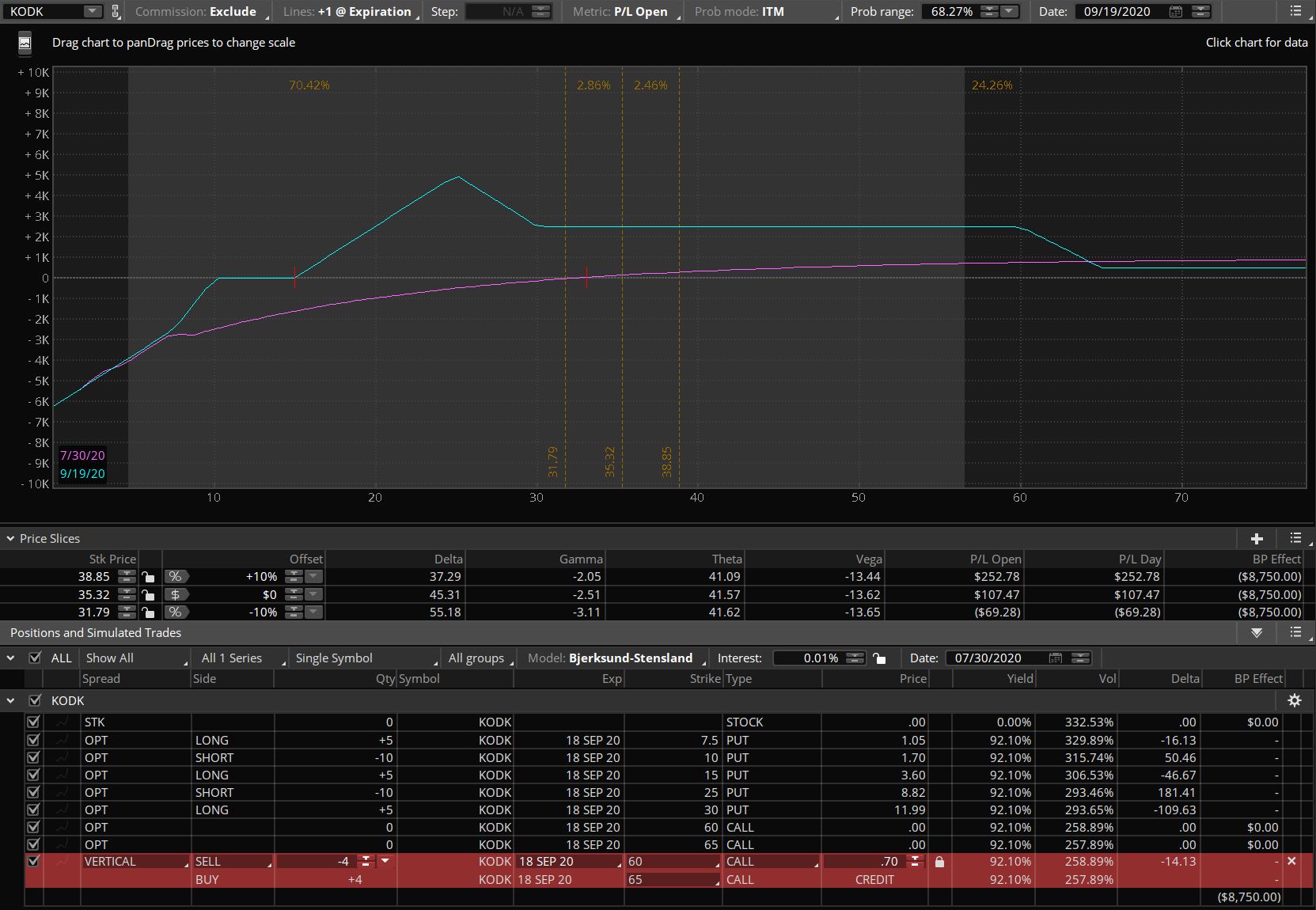

KODK….ugh rookie rookie here!

At about $35 I placed a ratio put spread/combo fly at 25/30 for 5.65 cr and a 15/10/7.5 put BWB fly for 1.25 debit. This gave me a breakeven of about 10.68. And a max loss of $5K on stock assignment with stock going to zero. Subsequently I closed the put debit component of the put ratio (30/25) for 4.85 taking 97% of available max profit.

I added a Sep 15/17.5 ATM (at the time) Call Credit spread for .88, and also added a DITM put Sep 20-strike. At this point it surely looks like a stock assignment is inevitable, so it’s about collecting as much as I can until then to lower the cost basis. These things can reverse on news, so trying to collect cash but not dig too big a hole on a reversal. This will be the classic Option Bistro game–that so many of you have mastered— to patiently and persistently work the basis. What a management team disaster on this. Queue the lawsuits!

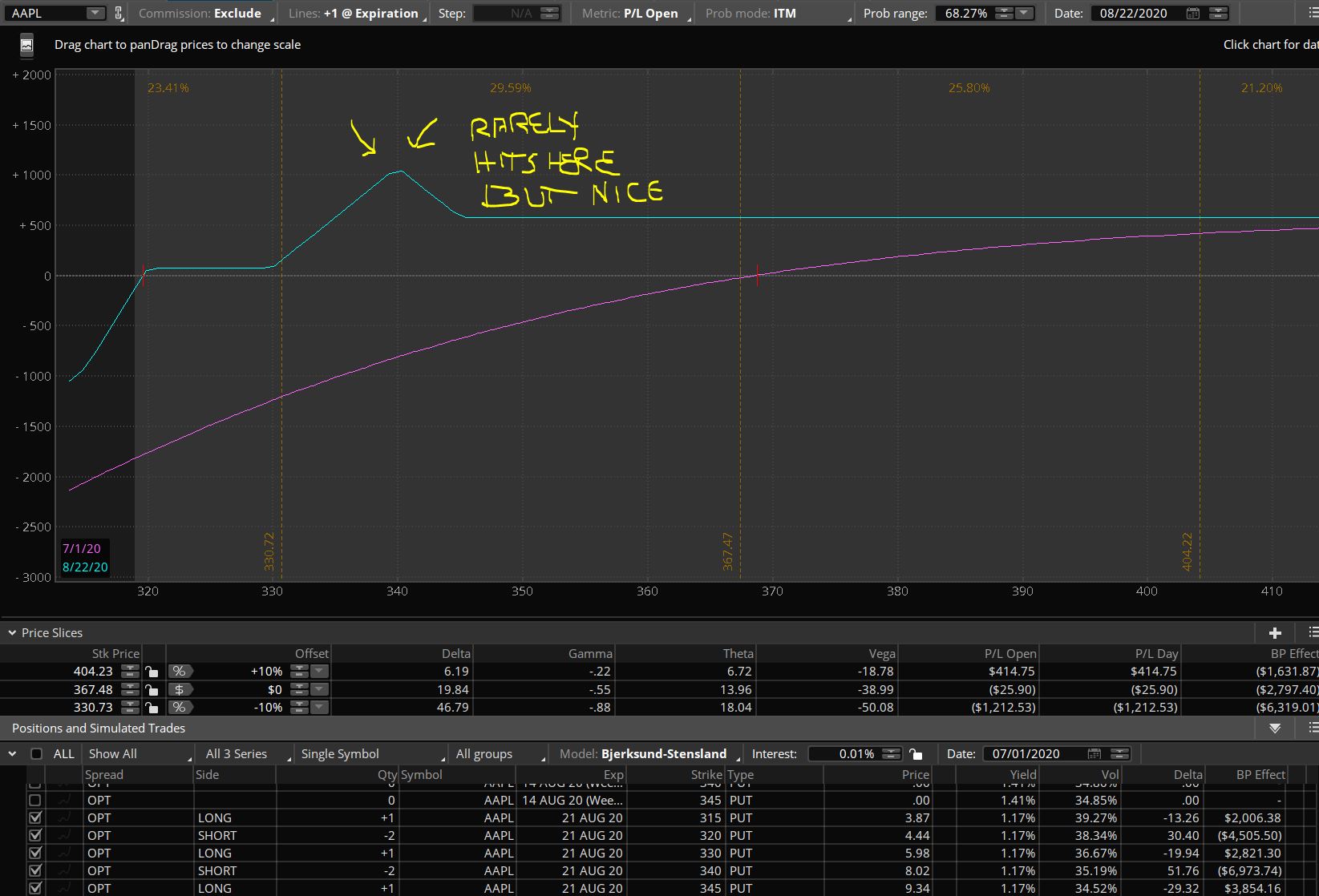

#fuzzyhotair #putratioladder AAPL put ratio…

AAPL put ratio ladder update: ON SUSPENSION

(1×2 credit ratios, 30 delta/25 delta, with a BWB hedge to extend downside)

So I’ve seen this movie before. The last time AAPL split there was a mad run-up in stock demand and price (everyone scratched their head back then, as well). I can make more (with less risk) using collars on AAPL, vs put ratios. Especially since I keep cash allocation for short put assignment anyway. Plus there’s an ex-div on Aug 7th.

So here’s an update on the “rungs.”

Week 1: CLOSED

Aug 21 345/340 sold 6.70, bought 2.32

Wish I hadn’t closed this, the breakeven was super far away…should have let more juice drain off until 20 DTE (right after these words were published AAPL dropped from $400+ to the 360’s on anti-competitive news reports, so closing was a good move in hindsight)

Week 2: Closed on July 31

Aug 28 372.5/365 sold 7.12, put fly hedge 350/340/335 .90: Put ratio closed for 1.45

Week 3: Closed on July 31

Sep 4 360/355 sold 6.05, put fly hedge bought 345/335/330 for .93: Put ratio closed for 1.61

Week 4: Still open

Sep 11 360/355 put ratio sold 6.10, put fly hedge bought 345/335/330 for .99

Breakeven $335

Collars added: 100 share blocks + Sold Sep 18 420 calls @ 20.10, + Bot Aug 28th Put Debit Spreads 400/380 @ $3.99

Split will happen on Aug 31

KODK

#putratiospread

#brokenwingbutterfly

#bearcallspreads

Sep 18 Sold 30/25 put ratio spread for 5.65 (5×10)

Bot BWB 15/10/7.5 for 1.25 qty 5

Trying to execute a ratio bear call spread at 60/65 for .70 qty 4

No upside risk, breakeven w/ the call spread is $10.00

#fuzzyhotair #putratioladder AAPL put ratio…

AAPL put ratio ladder, week 4

(1×2 credit ratios, 30 delta/25 delta, with a BWB hedge to extend downside)

Week 1: CLOSED

Aug 21 345/340 sold 6.70, bought 2.32

Wish I hadn’t closed this, the breakeven was super far away…should have let more juice drain off until 20 DTE (right after these words were published AAPL dropped from $400+ to the 360’s on anti-competitive news reports, so closing was a good move in hindsight)

Week 2: Still open

Aug 28 372.5/365 sold 7.12, put fly hedge 350/340/335 .90

Breakeven $340

Week 3: Still open

Sep 4 360/355 sold 6.05, put fly hedge bought 345/335/330 for .93

Breakeven: $335

Week 4: opened using earnings volatility (earnings are tonight)

Sep 11 360/355 put ratio sold 6.10, put fly hedge bought 345/335/330 for .99

Breakeven $335

I make a practice of always having cash available for assignment on these, so about 3 rungs is the most I can have on this ladder right now. The week 2 position is down to 29 DTE….it is profitable now. Barring any disaster tonight I might be able to close it tomorrow. Though the positions are all staggered by date, they ARE clustered around breakeven. It would be better I think for more breakeven diversification….but the markets have been in some consolidation.

PYPL Earnings

#putratiospread

#brokenwingbutterfly

Jul 31

177.5/175 put ratio, 2×4 1.65 cr

172.5/167.5/165 BWB downside hedge .58 debit qty 2

breakeven $166.93, approx 12 delta

#fuzzyhotair #putratioladder AAPL put ratio…

AAPL put ratio ladder, week 3 (1×2 credit ratios, 30 delta/25 delta, with a BWB hedge to extend downside)

Week 1: CLOSED

Aug 21 345/340 sold 6.70, bought 2.32

Wish I hadn’t closed this, the breakeven was super far away…should have let more juice drain off until 20 DTE

Week 2:

Aug 28 372.5/365 sold 7.12, put fly hedge 350/340/335 .90

Breakeven $340

Week 3–the Sep 4 expiration just opened today

Sep 4 360/355 sold 6.05, put fly hedge bought 345/335/330 for .93

Breakeven: $335

#fuzzyhotair #putratioladder Hi Guys! I…

Hi Guys! I had ankle repair surgery last week….boy it’s been tough! Lots of pain and living on one leg! But was finally better enough this morning to add to my AAPL put ratio ladder. Adding on an up day like this….maybe not the best, but a 46 DTE expiration opened up this morning. (quick recap on my process: 1. delta 30/25 1×2 credit ratio 2. At the BE of that ratio I place a BWB (otherwise known as a venus fly or sumo fly) to extend the BE down a few more delta).

Week 1: Aug 21 345/340 1×2 credit ratio for 6.70 with a butterfly hedge

Current price: $3.375

Break even: About 319.60

Week 2 (placed today): Aug 28 372/365 1×2 credit ratio for 7.12

Butterfly hedge: 350/340/335 for .90

Break even: About $340, about 14 delta

The week one trade has realized 50% profit as of today….I’ll leave it sit a little while longer.

#FuzzyHotAir #PutRatioLadder I really like…

I really like Fuzzy’s work on this. I’ve been doing loads of collars all year, but there’s times on a run up that I don’t want to chase the calls up, so I’ll let the position go. Then I’ll use some type of premium selling as a way to re-establish a position at a discount. Or if I want to add to a position, I can’t stomach buying at highs, but this is a great way to add in.

My favorite put selling strategy is a put ratio. My go-to is 45 DTE, buy 1x 30 delta and sell 2x 25 delta. THEN (since I’m more and more risk averse every year) I’ll often set a broken wing debit fly right at the breakeven on the put ratio to get me a few more $$ of break even room.

The part I’ve been missing though is the ladder dynamic of doing this campaign style.

I have a small AAPL collar position right now that I’ve been wanting to add into. I’ve been doing weekly put ratios on it, but I’d like to flip to a laddering style like Fuzzy laid out in his post yesterday. Why AAPL? It’s the driving force behind both SPY and QQQ…as AAPL goes, so goes SPY/QQQ. But it has higher volatility than SPY, so more $$$ (mo’ money ties into probability).

I’ll do one of these every week, here’s today’s trade (I chose Aug 21 strike at 50 days for liquidity, had problems with fills on the Aug 14 expiry)

Bought to open qty 1 Aug 21 345 put @ 9.34

Sold to open qty 2 Aug 21 340 put @ 8.02

Ratio net credit 6.70, break even: $328.24 (roughly 18 delta)

Additional butterfly (hedge):

Aug 21 330/320/315 @ .97 debit

New breakeven: $319.69 about 13% down, 15 delta

I acknowledge the butterfly hedge eats into profits, but I’m happy w/ the trade off for the extra wide profit structure on these. Plus this is a much more complicated way of executing Fuzzy’s idea, but I really like the risk/reward on it.

CODX roll

I took profit on my CODX diagonal (may/aug) and reset the trade this morning into something you might find interesting. I bought a 1/2 size stock position and sold the June 18 straddle for $8.15. This creates a full size covered call profit structure with just 1/2 the stock size. As you probably know, selling a put equates to a covered call. So I have a full size covered call ceiling with only 1/2 the stock. Takes up less buying power. Got much more selling the put than the call, despite it being ATM at the time. Because of that, the smarter trade would have been just selling puts for a full size position (in hindsight).

I hear earnings are tomorrow….

Sue

CODX

Thanks for the idea guys, I’ve placed the following diagonal:

Bought Aug 9 calls for 6.76

Sold May 15 calls for 1.40

TGIF!

Sue

Market Shutdown Guide for Options

Market Shutdown Guide for Options

Lots of conjecture around the market shutting down, what happens to open option positions. Tos directed me to this guide (remove the quote marks and copy/paste the link):

“https://www.theocc.com/components/docs/about/publications/unscheduled-market-closings-guide.pdf”

It used to be that the option owner would have to provide execution instructions, but now OCC executes every option that is ITM at expiration. I’ve had an issue with collars, where at the last minute the protective put drops ITM, gets assigned—taking my long stock away, and I’m left with naked short calls. So on my collar positions I’ve been trying to spread the short calls with something, anything, cheap to protect against that scenario on a surprise shutdown with ITM puts ready to expire.

It’s also important to be aware of how spreads will be affected on market shutdown if the stock price is between the spread strikes at shutdown (with looming expiration), it could cause execution/assignment of one leg leaving a potential dangerous situation.

So the way I read this is that on a shutdown, the options that expire during the shutdown will be assigned based on the last regular traded price of the stock before shut down. So….let’s say you have a AMZN Call Credit Spread, short 1800 long 1810, and the last traded price of the stock is 1805…..you WILL end up short 100 shares of AMZN at 1800, the 1810 will expire. This is quite dangerous with no ability to manage.

#fallingknife Couldn’t resist selling MSFT…

#fallingknife

Couldn’t resist selling MSFT Apr 3 105 puts for 1.35….will be much higher in the morning it looks like.

#Fuzzy VXX Bot Dec 17.5…

#Fuzzy VXX

Bot Dec 17.5 Fuzzy last week for tariff hedge, .18 net debit

Sold at the open for .20 net credit

Basically a scratch

Sue

#Fuzzy VXX Charlie McElligot at…

#Fuzzy VXX

Charlie McElligot at Nomura is issuing a lot of gamma red flag warnings for a vol shock. What the heck…a nice time to dust off a fuzzy in VXX.

Dec 20 Bot 17.5 call

Dec 20 Sold 17.5 put

Dec 20 Bot 15.5 put

Net price: .18 debit

I would guess vol stays steady here due to upcoming tariff increases on Dec 15, so I think not much decay on this–it’s a cheap way to get on some long gamma.

CRM Short

Did anyone catch Benioff’s interview two nights ago w/ Cramer? I found it troubling. I’ve always been a Benioff fan, but I’m seeing that he’s maybe losing focus. He spotlighted a stupid “Einstein Doll” that is supposed to talk and answer questions “you can buy it on Amazon”….huh? The doll didn’t work, it was an awkward moment. He seems to be losing touch w/ any kind of shareholder focus. I put a short on yesterday by selling shares and buying a protective call. I sold shares at 163.25, the call was an expensive January 165, so I need a sharp move down to make money, but it was in the 140’s not too long ago. Earnings coming up. Curious if anyone else saw it, if it hit you differently.

Sue

#SueCollar new TGT I needed…

#SueCollar new TGT

I needed a new position in one of my accounts and went back to the well on TGT. The vols and spreads are bumping around big time this morning on TGT, I probably should have waited before locking this in. But I saw favorable vol spreads so grabbed it. Jan 3rd opened up on TGT, but the spreads and liquidity were really poor, so I went with a Dec 27/Dec 13 starting setup.

I’m spending a lot of time now looking at the volatilities on the chain for the setup, and comparing them to realized volatility. The most expensive part of this strategy is buying puts, if you can buy puts “cheap” relative to realized volatility it should help the overall success (that’s also why I’m now comparing put vol to the call vol being sold–trying to eek out a bit more edge). As you know, OTM puts have a higher volatility, and that vol drops as you approach ATM. It’s typically opposite on the call side of the chain (except for tickers with upside danger like Vix and Gold)–ITM calls have a higher vol than OTM calls. It dawned on me recently that tightening the vol spread between the short call/long put strikes would further tighten risk on these. It does in fact lower the delta even more, which is great risk control, but further restrains the upside in grind-or-melt up conditions. That’s the trade off. I’m looking to keep the vol spread now at 3 or less points. The put buy continues to be a balancing act though between volatility and price….since in normal market conditions it’s throw-away insurance. So I don’t want to overpay on price just to get a lower volatility.

If you use TOS, you’ll see the option chain has a different vol than the analyze tab. I keep wanting to ask the trade desk for an explanation on that, but I’ve chosen to use the analyze tab volatility for my record keeping.

TGT Entry: Starting P/L in this account for TGT is zero

BOT 300 shares @ 127.08

BOT 3 Dec 13 121 put @ .95, at the time of purchase vol was 22.37%, 90-day realized vol is 43.1%

SOLD 3 Dec 12 126 call @ 4.00, vol was 24.16%

This was a vol inversion that I grabbed, usually the put vol is higher than the call vol

You can see I’ve sold well in the money calls to get a higher volatility.

Max risk at the onset is $909.00

#SueCollar TGT One of the…

#SueCollar TGT

One of the collars I had set up was on TGT, which of course had earnings today. The original stock purchase was at $111.84, and after a roll last week, was protected down to around $96. It’s really run away to the upside. There is plenty of premium in the position still, especially since the Dec13 short 96 puts have become very illiquid. It looks to me that the 300 share position will net out around $503 in profit (including the dividend) by the Dec 13 expiration, a hold of about 2 months. This would equate to roughly an 8% annualized return….right in my target. The ROR is huge given the risk controls in this strategy.

A couple comments on this:

1. TGT is an interesting hold for this strategy due to their dividend timing. Since the ex div is the day before earnings, it is really hard to lose shares to someone wanting to take the dividend—since the short calls retain such high premium the day before earnings.

2. This is a perfect example of having to stay focused on a low-risk/low-return strategy. If the loss of the put premium is too much to bear, it’s the wrong strategy for you (you might be saying “coulda woulda shoulda made $4600 just holding shares vs $503 on the collar”). I get it, it’s valid. But I really appreciate the controlled risk on these things, the easy sleep at night.

On a side note, since I’ve been training intensely on vol for a couple years at Option Pit, I decided there needs to be more vol strategy folded into the collars. I’m now trying to keep the vol spread at less than 3 points between the calls being sold and the puts being bought. To accomplish this the calls need to be sold ITM, vs ATM. ITM calls have a higher vol to counter the higher vol of OTM puts.

Let me know if there’s any interest in this going forward–I get if it’s too boring 🙂

Sue

#SueCollar CMCSA Adjustment Here is…

#SueCollar CMCSA Adjustment

Here is the opening trade I did on Oct 11:

1. Bought 600 shares @ 45.02

2. Sold Nov 22 45 call @1.46 x6

3. Bought Nov 1 43 put @ .46 x 6

Net delta is 145 on 600 shares

Here is the adjustment:

1. Underlying price is 44.25 right now

2. Nov 1 43 puts: bid is 0.00, expiration at full loss is expected (-276)

3. Bot 6 Nov 22 43 put @.42

4. Bot 6 Nov 22 45 call @ .52, to close ($564 profit)

5. Sold 6 Dec 13 44 call @1.35

Net options trades $846 credit / 600 = 1.41 cost basis adjustment to $43.61. As before, not fully realized.

Thought process:

1. On Oct 11th the position delta was 145 on 600 shares. This morning the position delta was 350 on 600 shares….quite a bit more risk in the position (due to short-delta decay). I like to keep deltas below 30% of the underlying share delta (600 in this case).

2. Rolling calls and puts, instead of just puts) can be an effective way to reset the delta, I had 65% decay in the calls, so decided to take the profit and roll them out. My delta is now 77 instead of 350.

3. I had been planning on doing this adjustment tomorrow after NFP, with the thought that volatility would decrease. However vol has been steadily rising in CMCSA, and with that high position delta I wanted to get some better risk control on.

4. There are no divs left in CMCSA this year, so not a consideration

5. Crash protection with 43 puts

#SueCollar TGT adjustment Here’s the…

#SueCollar TGT adjustment

Here’s the opening trade I did on Oct 15:

TGT

Bought 300 shares @ 111.84

Bought 3 Nov 8 110 put @ 1.65

Sold 3 Nov 29 112 Call @ 4.70

Whenever the puts are over a double, I look to adjust and take that profit, lowering cost basis.

Here’s my adjustment:

1. Sold 3 Nov 8 110 puts @ $3.84 ($657 profit)

2. Bot 3 Nov 29 112 Call @ 1.71 ($897 profit)

3. Bot 3 Nov 15 105 puts @ 1.31

4. Sold 3 Dec 13 106 calls @ 4.45

Thought process:

–Puts had more than doubled, calls had decayed over 60%. That’s what I like about this structure, the gamma in the short-dated puts can really cause a big move, yet the long dated calls still have really nice decay.

–Normally I would have bought Nov 22 puts, but that is earnings week and the puts are too expensive for me that week

–TGT dividend is the day before earnings, my short calls should have very adequate premium in them to be able to sustain a move up into earnings but still collect the dividend (.66).

–The math on this can be simple or complicated. Doing the simple math, my net debits and credits now across all options trades is $2496 credit, divided by 300 shares = $8.32 in cost basis reduction. That takes me to 103.52 for cost basis on shares purchased at 111.84. Obviously all of that cost basis reduction is not yet realized, and will change with the next adjustment—so $103.52 is “blue sky” at this point.

–I chose the Dec 13 calls to sell based on the dollar-strikes, I like to get right ATM

–I’m crash protected with the 105 puts.

#Augen In case you missed…

#Augen

In case you missed it (I did) there was a 3-in-5 Augen signal on Oct 9th. That’s the first signal since Aug 2018–roughly 14 months. It “should” mean that the rally has some legs. However I still watch the rolling 20 day score on 1-standard dev up moves. We were at 6, we’ve dropped to 5….over 6 can mean things are a little hot. The higher the rolling score gets, the more likely for a correction (manic buying).

I only count Augen signals the first time they hit after a 4% or more correction. So multiple Augen signals I don’t count after the first one. It stays in place until a 4% drop (however there was a 2nd Augen 3-5 signal on Oct 19).

#SueCollar Here’s a new one…

Here’s a new one I just added, this one has less than zero risk at the onset–it’s hard to get this design but I really like it, call premium is elevated due to earnings the week before. Notice the tight put, less than $2 away from stock purchase price, at close to 1/3rd the call premium. Good risk control here. The put roll might be tricky though with earnings looming in the new roll cycle, but we’ll deal with that the week of Nov 8, if not sooner.

TGT

Bought 300 shares @ 111.84

Bought 3 Nov 8 110 put @ 1.65

Sold 3 Nov 29 112 Call @ 4.70

Initial max risk is -$363, meaning I make $363 on a crash in the initial timeframe (Nov 8 expiration).

Earnings 11/20, Ex div 11/19

update: one thing though, the delta on this is only 36 on 300 shares, that’s usually lower than I like, I like around 25-30% delta. I can always sell some put spreads to bump up the delta if I want.

#SueCollar Good morning lovlies, TGIF!…

#SueCollar

Good morning lovlies, TGIF! I thought I’d start posting a little again on my collar strategy. Life has been hectic, March 1 I executed on a move to Iowa, regretted the house purchase from the first minute I took possession. Regretted being in Iowa at all. Desperately missed the mountains. Aug 30 executed a move back to Colo, without selling the Iowa house. I’m finally settled back in Colo, though still trying to sell Iowa. I am SO HAPPY to breathe Colorado air again.

So…re trading. I started doing 13-week Tbills over a year ago. The T-bills made me realize that as I’m older, I have less appetite for risk. They also taught me patience. I would make (risk free and state-tax free) as much in 13 weeks as a 1-week Jade Lizard can turn over. But, with a ladder, the risk-free money was rolling in every week. The T-bill rate hit a high last December then started dropping. Once it got close to 2% I realized I needed a new low risk strategy.

So I went back to the #collars . This is a slow, steady, low volatility, limited risk strategy. My goal is to net out about 3-to-6 times the Tbill rate. So 6 to 12% a year. The return-on-risk is much higher, around 50-100% due to risk being so controlled.

I have a very specific process I follow that seems to be working well, that’s why I’ll call it #SueCollars

I use the term “collar” pretty generically. Some would call this “married puts.” I also call it a “rev con” (Reverse Conversion). To me they are all interchangeable. The premise being that there is a stock position, a short call, and a protective put.

My process is 1. Buy stock (I have a tight list of high yielding stocks with good balance sheets—I’m limiting buys right now to PEP, WMT, VZ, CMCSA, CSCO, EBAY, AMD, INTC, BX, MSFT, TGT, UPS, JPM, TGT). I also size every buy for the same amount of stock risk, i.e. all of them around $30K in stock for example. That way capital allocation across tickers is roughly equal.

2. Sell ATM calls around 45 days out. Collect the max you can

3. Buy OTM put 22 days out, targeting 1/3rd of the premium collected on the calls for the buy-price. The thought being that the calls can finance a couple rounds of puts, with enough left over on calls for net profit.

Here is a trade I put on today in CMCSA:

1. Bought 600 shares @ 45.02

2. Sold Nov 22 45 call @1.46 x6

3. Bought Nov 1 43 put @ .46 x 6

Net delta is 145 on 600 shares….so it’s still a bullish trade, but look at all that risk control! Risk is reduced by 75% (obviously any time risk is reduced, profitability is reduced, but remember my benchmark is the 13 week t-bills).

At the outset my max risk on this trade is $612 if there’s a crash. I calculate max risk this way: (600 * 45.02)-(43*600)+(.46*600)-(1.46*600). Basically (stock risk) less (put protection) plus (put cost) less (call premium). Max gain on this trade is $590.88. Roughly with dividends this can yield about 10% a year with pretty good risk control.

There’s a lot of nuance with this trade that I’ll try to capture

–Most people do shorter dated short calls and longer dated puts, I found the opposite works well to finance the puts. On a down swing, the shorter dated puts are a gamma play, they can just explode in value, and longer dated calls very quickly decay, so it’s very nice for collecting realized gains.

–When the protective puts at least double in value (sometimes I can get 7x on them) then I’ll roll everything down. I’ll take profits on the puts and short calls, roll calls to a new 45 DTE ATM and buy new puts. On a big downdraft it’s hard to get new puts at 1/3rd the call value, since these are strong companies I’ll do a very wide put spread to reach the price target. On a bounce it’s easy to buy back the short put and re-establish the full put protection. These rolldowns really do a lot to keep pace with the stock decline.

–A lot of these stocks run up into ex-div and it can be hard to hold the shares. The big thing to always remember with ex div approaching…you CAN be ITM on short calls into ex-div as long as EXTRINSIC IS MORE THAN THE DIV. People tend to freak about ex div and ITM short calls, but it’s an easy rule to remember. I’ve found placing the short calls a couple weeks later than ex div can really help with holding the shares through ex div to collect the dividend. VZ has always been tricky to hold into ex div.

–Once the extrinsic is all gone on short calls I used to self-assign on these to avoid assignment fees….but all that is gone now w/ TDA, no more assignment fees!

–On ITM short calls with no remaining extrinsic, sometimes I’ll roll them up (debit roll) but mostly I take the profits and wait for a down day to re-establish positions.

–I love Fuzzie’s approach of using short puts to re-establish after losing a covered call position but mostly I just re-establish with new stock positions since I’m all about risk control on these.

I’ll keep posting updates on this, and when new positions are established.

Everyone have a safe weekend.

Sue

Buh Bye NFLX #CostBasisReduction Winner…

Buh Bye NFLX #CostBasisReduction Winner

My NFLX saga ends today…with a bottle of champagne after the close. After the last earnings report when NFLX soared, I got the “great” idea to buy 100 shares at $358 and sell DITM calls for a guaranteed win. Within days there was a massive crash. I took inspiration from seeing @fuzzballl accomplish significant cost basis reduction with patience and perseverance. I vowed I would stick with this until it was profitable. Every single week I sold calls, and bought put butterflies (BWB debit flies). Most of the time they brought in nice credits, there were a few weeks that were debit rolls (debit rolls would step back cost basis those weeks), but I steadily took Cost Basis from $358 to $272. Today I was able to close out the full position for a net $1547 gain.

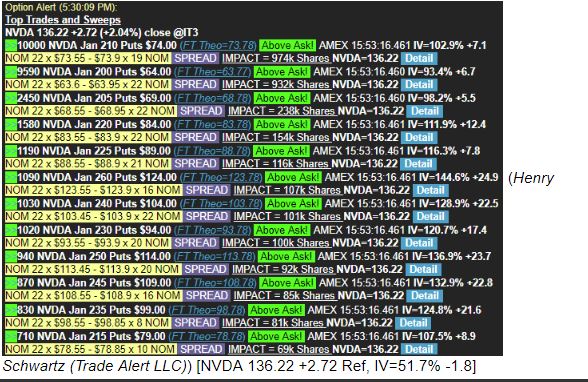

Dodeka-Stupid on NVDA

Here’s a note that Trade Alert put out tonight:

Market Color NVDA – Interesting 12-leg Nvidia put spread minutes before the close totals nearly quarter-billion dollars premium. Over 31K deep puts traded in NVDA at 3:53PM ET today in an odd spread that involved 12 deep-in-the-money puts expiring Jan 18th. Stock was $136.22 at the time, and the package consisted of offer-side blocks in the 200 to 260 strike puts, priced from $64 to $124. Weirdly, size of each block is very near the open-interest of each contract and the price on each block was a whole dollar figure, 22c over parity, with total premium just under $244M. If the package was a buyer of all legs, the delta is nearly 2.4M shares, or 9% the adv of the stock. With negative AAPL headlines out after the close, NVDA shares are down nearly $4 to $132 which could be a gain near $9M if the spread was a dodeka-stupid.

Follow up info

Here’s some follow up info to the post I did a couple days ago:

1. Scott Ruble is currently at www.stratagem.com His courses are good, but expensive. His “POT” (Practical Options Tactics) subscription is VERY expensive ($299/mo) and generally not worth it, very frustrating (You can get a 30 day trial of POT for free though). He has moments of brilliance, but you have to weed through a frustrating delivery style. @kathycon and I call it “finding gems in the poo.” Aeromir offers a 10% discount for Scott’s stuff, I think the coupon code is “AEROMIR10” or maybe “AERO10”. Scott is a bit like “Whiz-Lite.”

2. Scott used to be at Random Walk and the Random Walk website has some of Scott’s classes…some are even FREE…so I recommend going to www.randomwalktrading.com before doing anything at Stratagem. The “Layered Spreads” class at RW for $95 (on sale right now) is a must investment I think. Very very good, and taught by Scott. You get a very detailed pdf book with the course. If you buy the course, you get access to many videos immediately, but the PDF takes a couple days to receive while they do the ID encoding. All the doc downloads at RW are encrypted with your personal ID…so you can get in trouble if caught sharing them. Ed T. at Random Walk has the “OIA” subscription for $50/ mo….excellent value for what you’ll learn and his professional delivery.

3. Aeromir www.aeromir.com (Aeromir took over the defunct “Capital Discussions” group) has a free membership that gets you two week access to tons of videos (rolling two weeks)…definitely do the RTT 1 month trial for $25.00. You’ll learn a ton of good stuff. After the first month it’s $155. I think you can learn enough in the first month to go it alone. The trial will inundate you with info though….tons of email updates, risk graph images, texts on every update, videos to watch. They’ve recently launched two new services based on RTT, that give you “light” versions of info for a cheaper monthly expense. Just do the full trial and you’ll be on your way. RTT’s have struggled a bit with us in backwardation right now, so they have needed a lot of management…which is actually good to see the approaches they take for defense (Risk Reversals, Rolling Thunder hedges, Reverse Harveys). Aeromir does a lot of roundtables bringing in various trade experts to talk about their designs. If you search on YouTube for “Aeromir Scott Ruble Roundtable” he recently did a really good session on Rolling Thunder. I’d classify Aeromir as kind of a “bulletin board” type core, surrounded with different trade services. Low tech website, but they do bring in some good roundtable speakers, and “Trading Group 1” in the videos are usually worth listening to.

I think that’s about it, I’ll add more if I think of it.

Below is a snap of an article in Stocks and Commodities magazine about the RTT. I have the pdf if anyone wants it, drop me a line. smasterson@yahoo.com Or you might be able to google it.

Sue

Happy New Year!

Hi Everyone! I just couldn’t find a new bread-and-butter trade this year that justified reporting, so I lost track of a lot going on here. I did find some good new approaches though. I found Scott Ruble (Stratagem) to be an excellent teacher on structured courses, but a terrible terrible subscription provider. @kathycon and I have used several of his approaches in the last few months to make money…#AdvancedRiskReversals, #SpikedCollars, #LayeredSpreads, and #RollingThunder. Scott was with Random Walk for awhile before having a falling out. Ed has taken Scott’s place at Random Walk and has a $50/mo subscription service that I quite like. Very reasonable for what you get. Ed’s approach is #PregnantButterflies which layer in spreads in a way to provide wide profit ranges, often risk free. The #RTT (Road Trip Trade) trades at Aeromir are good (BWB), and they manage them very dynamically using a lot of Scott’s teachings. The one month trial of RTT is very worth it. Option Pit is still great….but VERY deep and takes a ton of cerebral work….especially if you think you know it all already (like I did).

The only update I’ll give is on NFLX. I made a solemn vow in @fuzzballl ‘s name that I would stick with this until I was even. I started at $358 a share and am now down to $272….that’s a ton of cost basis reduction! I’m accomplishing this two ways…. 1. using weekly debit wide broken wing put flies (Ed calls them “Venus Flies” for the downside collar, and. 2. using weekly covered calls to finance the flies. As you can see I’m still off the mark on break even….but I’m being mechanical with the income collection and tracking every cent against the cost basis. I’ve only got 100 shares of NFLX so the ride down has been manageable.

Hope we all get what we want from the market next year! This last year is one of those that seriously refines you as a trader. Survive….and you come out a much better trader.

Sue 🙂

Hi Guys!

It’s been awhile since I posted, thought I’d pop in here and say hi! I’m deep in the weeds at Option Pit. I’m in their pro group now. My trading is changing quite a bit, to a style that is more “book management” than “trade management.” Using low volatility to build a catalog of long puts and calls, then selling around them to pay for the decay, and selling out the longs as the market demands (for example I have a bunch of IWM puts that are getting close to being up 100% now, so I’m metering them out). I’m doing a lot of ratio calendars to acquire the longer dated options at a discount. This would be impossible to do with the old commission structures that had a ticket fee + contract fee. Thank goodness Tasty Trade caused a lot of pricing innovation! It’s less stress knowing a big move in either direction pays out nicely….it’s just managing the middle that’s important. It’s going to be an interesting quarter with everything going on. I’ll try not to be such a stranger!

Sue

#Zebra Trade I caught a…

#Zebra Trade

I caught a rare Liz & Jny this morning “Calling All Millionaires” and caught their #Zebra trade (Zero Extrinsic Back Ratio). This is a little similar to the #Cobras I was doing a little while back (Covered Back Ratio). It looks like a good way to keep some short delta in the portfolio.

My trade today: BTO SPX Sep 26 2940 put (30DTE, 70 Delta) @51.70 x2, STO Aug 29 2900 put @ 6.80 x1. These get rolled every two days (keep track of accrued credits against the longs).

Good video here explains the trade and management:

https://www.tastytrade.com/tt/shows/calling-all-millionaires/episodes/zero-extrinsic-back-ratios-in-2-easy-steps-08-22-2018

M Earnings

Here’s my trade for tomorrow am:

1. STO qty 10 sep 34 puts @.44

2. BTO qty 1 sep 41/39 put debit spread @ .85

3. BTO qty 1 38/36 put debit spread @ .51

BE $33.30, profit levels: step 1 $304, Step 2 $504, Step 3 $704. 50% of step is my target.

ROKU Earnings

I’m doing something a little different here.

BTO: 1,000 shares @46.25

STO: Aug 10 46.5 calls @ 3.40 x10

BTO: Aug 24 43 puts @2.67 x12

EM up = approx $1400 profit, EM down = approx $200 loss Max loss= approx $700 No upside risk, Diagonal-type risk graph, $3000 max profit on no movement.

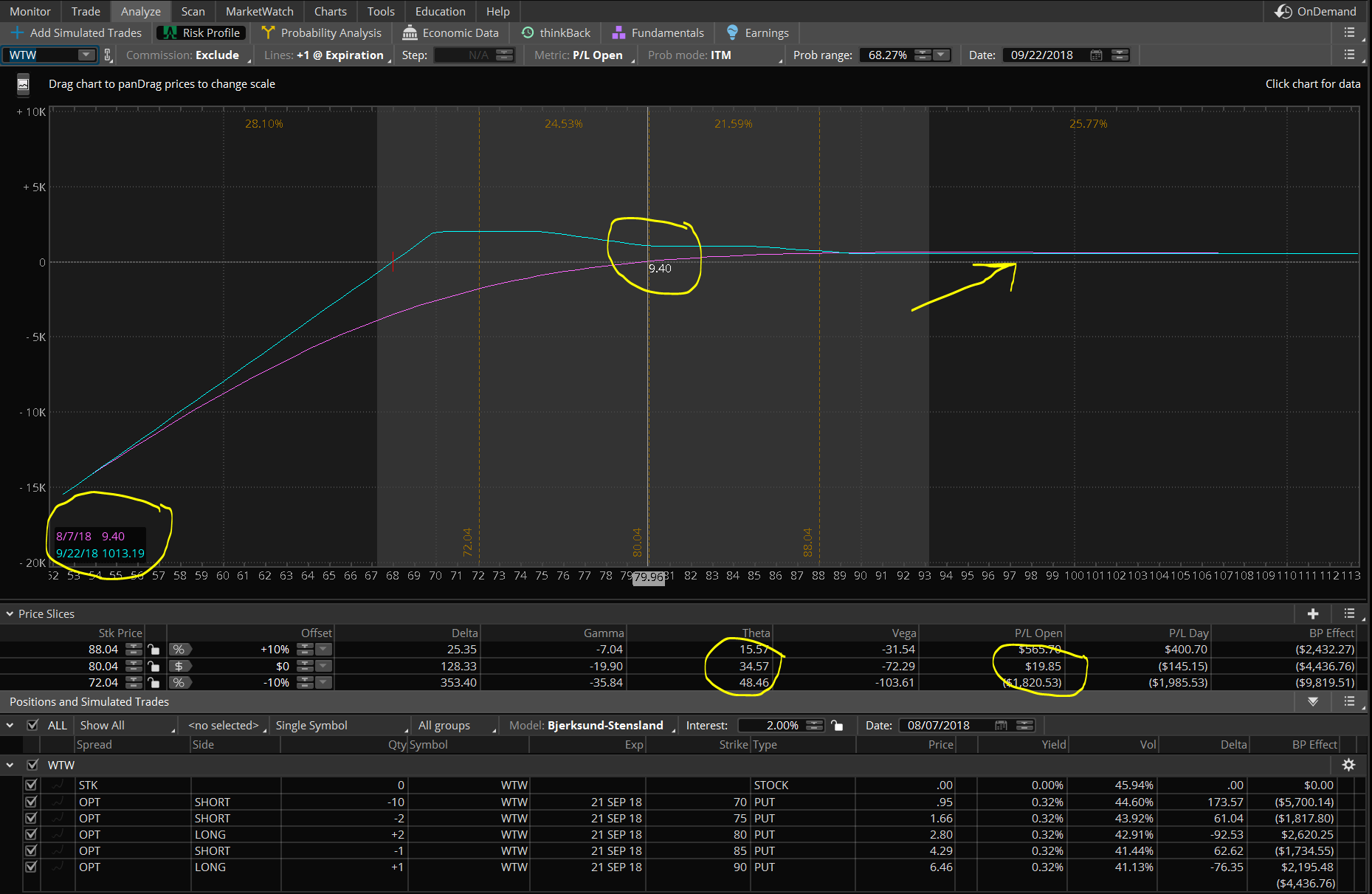

WTW earnings

I just wanted to show y’all how well this trade performs for earnings. WTW has been down as much as almost 15% today, yet my trade is profitable. On top of that, since it is in the “second step” I have a max profit of $1013 to shoot for. My target profit is 1/2 of max. If there is a whipsaw recovery on this stock, my max profit doesn’t drop below $505 (no upside risk).

SHAK/WTW earnings

SHAK closed for over target, $315 profit on #stairstep

WTW: Opened Stairstep for earnings today. STO Sep 70 put @.95×10, BTO Sep 90/85 put debit spread @ 2.17 x 2, BTO sep 80/75 put debit spread @1.14 x 2. Break even is $68, 25% down from current spot.

These trades are 100% winners so far

SHAK Earnings

#Stairstep STO Sep 50 puts @ .75 x10, BTO 62.5/60 put debit spread @1.10 x 1, BTO 57.5/55 put debit spread @.69 x2.

Break even 48.75, which is getting close to 34% downside with no upside risk.

Important note on these trades: The breakeven is very far away, but on a significant down move there are short term losses that require duration in the trade for theta to overcome. As price drops, the “stairstep” profit levels go up.

EA

The EA trade was bonehead yesterday. The long vol crush was 23%, it killed the trade. Lost $644, but I made $380 scalping 10 AMZN shares after hours last night, and took $350 profit from the BA trade this morning. On EA, the risk graph was just not showing the danger, but the vega level was the warning. In the future I will split the time frames for analysis and apply better vol crush to each one.

The backtester shows an almost 100% success rate on BA (5 year test) with this trade: 1. 45DTE 2. sell 10 delta put x 10 3. buy 30/20 delta put debit spread x 2 4. close/reset at 50% profit. So I will be placing this trade this morning on a rolling basis. I will probably do 5/1 on qty. Excuse the “mouse writing” on the pic.

Recent ALGN/LMT/BA trades

ALGN from yesterday is up $475.00 but the market makers make exit on this a little hard, so I need a little more to cover the exit slippage.

LMT: This is currently up $180, target around $250.

BA: This is currently up $284, target is $350 for closing.

EA Earnings

Ratio Straddle Time Spread

STO 143 Straddle @ 7.95 x8 BTO 143 Aug 3 straddle @ 8.83 x10. Sold 93% vol, bought 49% vol. Ave vol crush is 8% on EA.

GOOGL #Supercharger Opened this morning,…

GOOGL #Supercharger

Opened this morning, closed just now for .30 gain, $300, 4.40. Just wanted to take the present of a nice one day profit before a big tech night.

ALGN Earnings

STO Sep 270 put @1.40 x9, BTO 370/360 Put Debit Spread @ 3.70 x1, BTO 320/310 Put debit spread @1.25 x 2. Break even: 266, 30% from spot.

July 25

My last two earnings trades in LMT and BA are looking fine. They are theta duration trades now.

GOOGL: #supercharger BTO Aug 3 1230 STO Aug 3 1235 for $4.10, target $4.55

GRUB: #StairStep STO Sep 21 100 put @.70 x10, BTO 115/110 put debit spread @1.05 x 2, break even: $98.50. Plan to roll the 100 puts to 105 to collect more premium.

BA Earnings

STO Sep 310 put @2.06 x5

BTO Sep 340/325 put debit spread @3.33 x1

BTO jul 27 330 p @ .44 x 3

This is a similar trade to LMT yesterday, but resolves the T+1 line drop. If there is a radical drop in BA the breakeven due to the extra Jul 27 puts is all the way down to 276, 23% down from spot.

I’m honestly not entirely sure how this will really play out…I’ll report on it!

LMT Earnings

STO Sep 280 put @1.35 x5

BTO Sep 305/295 put debit spread @2.12 x 1

Break even: 277.08 13.3% down from spot, 5x expected move

Hello!

Hey everyone, my dad has been having some serious health issues where I’ve found myself called to the hospital on a moment’s notice, a couple times. So my trading is more position-oriented now, less active, longer term focus, until I get past this. I’m still trying to read everyone’s posts as I can! I was sad to miss the 3-in-5 trigger a week ago.

Sue

TGIF

Hi Everyone! Hope you’ve had a good week! This has been a rest and reset week for me. Ditching #Saf-T trades and back to #AtomicFuzzy for me. The atomics are good for higher vol environments. When vol drops back down below 13-14, then regular fuzzy will work.

Just wanted to pop in and say today will bring 2-of-5 1-standard deviation moves up. Looking for that 3rd. The last signal we got was May 10 and about a 95 pt rally ensued. Mon/Tue/Wed are all candidates for a signal.

Sue

ATM call flaw

My mind is ruminating on the flaw of this strategy (rolling calls down to ATM with fewer contracts). I’m out running an errand, but my mind is telling me there is a flaw tied to low delta on the longer dated long calls. Just wanted to toss out a caution. I’ll explore when I’m back in the office.

June 27 Sue Trades

I’ve got about 50 filled orders today on hedge rolls. If anyone is tracking details on a particular position, let me know.

My go-to strategy on these #Undies is to roll hedges to ATM for significant premium collection BUT reduce contracts sold. On BA I started with a 7×5 and rolled it to a 7×3 now. I realized I can collect a lot of premium doing that, but still have a risk graph that is friendly to an upside reversal.

That’s all I’m going to post due to vast quantity of orders today.

Sue

June 25 (anniversary of Custer’s Last Stand, plus smasty BD :) )

A lot of trades today, rolling down short calls. I started the week this morning with $22,516 in short call premium to collect. That provided a cushion for today, but of course it’s not a 100% hedge.

1. AMZN rolled the 1745 calls down to 1720 for this week, collecting $1661 on the original calls and another $7.25 on the new one.

2. Closed the SPX #UndieBear for $5090 profit, if you add Thursday’s $1290 profit onto this, that’s $6380 in 3 days. This was a small 2×1.

3. GS and QQQ: got the butterfly fill on my Put In/Out trades from about 10 days ago. This locks in partial profit and cuts risk on them. I start with a skip-strike in-and-out spread, then look to butterfly it w/ a broken wing for half the price of the first spread.

4. MU rolled down calls from 62 to 57.5 (25 delta) for $1523 profit on the original ones and an add’l $376 on the new.

5. TSLA closed out the put fly and put spread for around $80 profit I think, wanted to simplify book this morning.

6. SPY #Saf-T rolled Wed calls out to next wed, collected $1536 on this week’s calls. My protective puts on #Saf-T are up a collective $32,800. They are sentries for me right now.

7. MCD added a put diag to my #Undie to balance deltas and bring in some premium for next week, cuts risk.

Don’t get me wrong, big losses across the board here, but all these trades are easy for keeping your head on straight. Just collect the hedges and reset.

Sue

June 22 TGIF!

SPX: The first trade I got off at the open was a new #UndieBear Aug 2785p x2 @52.00 Jun 29 2750p x -1 @ $10.80. No profit ceiling on a downside move.

CVX: Rolled calls into strength from jun 22 to jun 29, netted $330 on roll of 3 calls. Jun 29 126 @ 1.68.

IWM: I have a #Saf-T on this with short calls at 168.50…so dancing around the roll on this to get as much premium collection as I can.

LMT: The bulk of my calls were rolled on Wed, but I have two stragglers that I will let expire and sell new near the close (naked for an hour).

Oh, RHT: I got cute on the dive last night and bought 100 shares @ 150 expecting a snap back. So now I have a #CoveredCall . Sold Jun 29 $150 call for $1.10.

That’ll be about it for today.

Sue

IWM rolled Jun 22 168.5 to Jun 29 168 (went down, itm). Netted $494 on a 13-lot.

I ended up keeping 82% of premium sold for this week: Collected 17,917, kept 14,722.

Oh, almost forgot. The #Fundie maybe not so bueno. Rolled down calls for jun 29 on NVDA/ADBE/BABA to collect some add’l premium for next week. Kept same expiration.

Jun 21 Happy Summer!

1. SPX #UndieBear I just took $1290 profit in one day. This is a highly responsive trade to the combo of vol increase and price decrease. Market Profile is showing a developing 45 degree line for today, meaning folks are getting short in the hole. So decided to take profits. (Whoops scratch that on the 45 degree line, it looked like it was holding as support, but it broke)

2. Was at the hospital all day so took off the AMZN “vol fly” at the open so I wouldn’t have to manage it. Saw an $88 loss. I slipped in the close order before the drop in AMZN…it would have been fine in my fly range, but would have had some short term pain on it.

3. New AMZN trade: AMZN/XLY #DoubleRatioUndie AMZN is too expensive to double-undie, so I’m using XLY as a proxy for the put side. AMZN: Aug 1700c x2@106.15/Jun 29 1745c x-1 @19.30 XLY Aug 113 p x10 @2.93/June29 111p x -8@.63. The XLY side removes about 20% of the risk on the AMZN side.

4. TQQQ roll #Saf-T : Rolled Jun 22 to Jun 29, netted $4660 on the Jun 22’s. Rolled same qty but dropped to 62.5’s for 1.38.

5. Added an MU #DoubleRatioUndie at the open this morning: Sep 57.5c x10 @7.65/Jun 29 62c x -8 @1.39, Sep 62.5p x 2 @5.35/Jun 29 60 p x -1 @1.15. Max loss about $4800, gain at $62 next week is $1302. Premium sold for next week = 16% of risk.

Only two things left to manage tomorrow: CVX and IWM.

Jun 20 Sue Trades

AMZN “vol fly” Price is sliding down the T+1 line slope, so flattened delta by buying 10 shares of stock @ 1750.11.

SPX: #UndieBear I needed a little downside balance against my long portfolio, so here’s the first Undie bear. Bought Aug 2800 put x2 @ 60.50, sold 1x Jun27 2750 put @10.00. The ratio means there is no profit ceiling on a downside move. 20-day historical vol is under 10%, so buying low here. The trade has over 700 vega, any down move and this should explode.

AAL: Abandoned this position due to poor technicals. Net loss $434.00 on a 10×8 #Undie with a couple rolls. This was a July long too, so wanted to get as much salvage value as I could on the long before accelerated decay. This was a Mark Sebastian pick that I followed. At one point it had very nice profit, but I was piggie 🙂

GS: Rolled calls from Jun 22 to Jun 29, 235 to 232. Netted $946 on 5 lot on Jun 22, Jun 29 sold for $1.52x 5. This is another position I’m not happy holding. Earnings coming up in a few weeks, so I’ll collect some additional rolls on this. GS: Added an in-out put bear spread for more short delta: jul 13 230/225 @ 2.36 x4. I like to butterfly these after a favorable move to lock in some profit.

ROKU: Closed #Fundie for target 20% profit, $165 net. Will evaluate a reset. ROKU is dropping off the Fundie list, Ms. Cash and I have a list of about 22 good Fundie candidates, and ROKU didn’t make the cut.

MSFT: New #Fundie in the earnings cycle for a pre-ER price/vol run up. Jul 20 100 c x6@4.05/Jul 6 103c x -4 @ 1.04. Target profit is 20%, $805 (this target might be a bit high).

PYPL: Closed #Undie for $817 profit. I’ve had a couple of these lately where nice profits evaporated. Plus just found out I might be called away from the trading desk temporarily, so decided to TTMAR. It was a 16×13…so had higher risk.

MA: Closed #Fundie for $135 profit….might be called away on an emergency so clearing out a few things. This was a 3×2.

SPOT: Closed #Fundie for same reason as above. Up $540 today, net $70 profit. 3×2.

Jun 19 Sue Thread

Hi Everyone! I’ve got a little rolling activity here:

BA: First this was a #DoubleUndie from Jun 14. In two accounts I had to close the 2×1 put ratios due to the extrinsic on the short puts running out of gas. This brought a profit of about $2900. Then I rolled my Jun 22 365 and 372 calls to July 6 365 calls, and added extra calls to convert the trade from an Undie to a #Diagonal . I netted $2742 on the Jun 22 calls. My net credit accrual on BA = 73% of the losses (I rechecked my math, was way better than I thought). So there is damage control to be done. One of my longs is Aug, one is Sep….so lots of rolling opps here. I have the spirit on this one to fight it out 🙂 I’ve got good starting baseline numbers, so I’ll always know where I am in recovery of losses.

SPY: Rolled some #Saf-T trade calls from Jun 20 to Jun 27. Netted $737 on the rolls. The Jun 20 calls were pretty cheap due to divs last week and lowered premium. I rolled from 278 to 277 for .71 on the new 277’s. BTW, all the Saf-T puts are up huge…they be doing their job.

Coming into the week I had $17,917 in short call premium (Jun 22 exp)….it’s helping, but it’s quite an ugly day here.

MCD: Rolled Jun 22 calls to Jun 29, collected $444 on the jun 22 170’s and rolled to 167.5 @.94 and added qty 2. This converts Undie to #Diagonal.

NFLX: Converted #Fundie to #DoubleFundie using this strong day to cut risk. Added a Jul 13/Jun 29 2×1 put ratio. Before add on max risk: $4000; after add max risk: $1110. Nice profit opp still in the trade, $800-$1200 on small continued upside. Downside BE shifted to $386. Jul 13 397.5 p x2 @14.05, Jun 29 390 p x -1 @7.05.

NFLX: Closed full position for $789 net profit

LMT: I guess the senate blocked their delivery of jets to Turkey. Did a partial roll of calls (qty 4 in 2 accts) from Jun 22 to Jun 29 rolled from 317 to 315. Netted $1208 on the Jun 22. Sold Jun 29 for only .68. Still have 2 calls at a diff strike to roll this week.

June 18 Sue Thread

ADBE: First #Fundie close for 20%, $425 in one day. This was a 30/14 3×2 time ratio. Trade reset immediately as per the backtest: Jul 13 252.5 x 3, jun 29 257.5 x -2 @ 18.35. I am starting with positive gamma/positive theta on this trade…which is kind of a unicorn 🙂

ROKU: Closed #Undie for $844 profit, reset as a #Fundie Jul 13 43.5 call x3, Jun 29 46.5 call x-2 @8.07.

On both of these trades I should have shifted dates to Jul 20/ Jul 6.

SPOT: #Fundie new test trade here: Jul 20 170 call x3 @10.20 Jul 6 177.5 c x -2 @4.30, target profit $440 for 20%.

MA: New #Fundie Jul20 197.5c x 3, jul 6 202.5 c x -2, @15.20 $300 target profit for 20%.

Here’s backtests on these (parameters: 30 day 63 delta long, 14 day 45 delta short, take profit at 20% and reset):

June 15 Trades

Happy Friday Everyone!

I didn’t have a ton going, ‘cept for one big thing. That later.

IWM: #Saf-T 1000 shares called, net profit $1200. Reset 1500 @ 167.66, 14x jul 27 166 puts @ 2.10, Jun 22 168.5 calls x13 @ .70

I was squirming bad this morning with a ton of SPY shares on and no short calls against them. Luckily the market rebounded, I got some short calls for next Wednesday in the book. I can sleep at night when I know my short calls are on. I’m not kidding when I say it felt really uncomfortable not having them. I will change this strategy next quarter so that calls are always on regardless of dividends.

BA…ugly, but I’m not too concerned. Got lots of hedges on, got a put diagonal kicker, so far it’s looking like a retracement. Maybe even the handle of a cup forming.

Ok…beware when @kathycon MamaCash and I open the lab. We can stay up all night online battering trade designs about and running backtests. We are ALWAYS taking established designs, or other people’s ideas, and reworking them for the best success rates, highest profits, lowest risk.

We reworked the dates and ratios on #Undies last night. I think you should let us test these out a bit. But what we discovered by backtesting is that a 30day long with a 14 day short in a .66 ratio (3×2, 6×4, 20×13) yields a much higher return on margin than using the longer dates. Because the 30-day longs are cheaper, there is less risk, which directly affects the return. These trades go on with a slight positive gamma, slight negative theta, positive vega…so kind of nice greeks on these. All of the 1-year returns we are looking at are really high, like 300% to 1200% (return on margin risk).

Consider these “petri dish” trades right now…we’ll run ’em down and report on effectiveness.

Between the two of us we have a lot of 3×2 tests on now in NVDA, ADBE, BABA, NFLX…and some others. We will report on the effectiveness of this.

Here is an example of one I have on BABA: Jul 13 202.5 call 3x @ 9.20/Jun 29 210 call 2x @ 3.40.

Everyone have a safe weekend!

Sue

p.s. premium collection this week was $14,811, 90% of what I sold. Good week!

TQQQ Dividend next week…..not

TQQQ for Div’s has been a little confusing. TOS shows a 6%+ yield, but the TQQQ pro shares website shows only 3 dividends have been paid in 10 years, for a fractional penny. TOS could not help me w/ an answer to this, they suggested I email ProShares. I received a fast response confirming that they are on a quarterly distribution schedule, but the last div paid out was in 2015. So anyone in a TQQQ covered for next week, almost minuscule div risk on that.

IWM div is next week though!

AMZN Experiment

I posted a couple times that I’m trying to embrace volatility analytics more in my opening trades. It’s an area I’ve been aware of, but not fully embraced. Last week’s AMZN trade worked out ok, but in hindsight, I bought higher volatility than I should have on the long leg, and when AMZN had a lull (with dropping vol), it really started to hurt me.

I wanted back into AMZN today, but here’s what I looked at before designing a trade:

1. The IV right now on AMZN is at the 12th percentile for the year, very low

2. The HV right now on AMZN is at the 1st percetile for the year. Uber low

3. The IV/HV ratio is 189% though, meaning that IV is almost double HV(20).

This is the trouble I got into last week, buying when IV was very elevated over HV.

So instead of a diagonal, I’ve decided to do a July 13 Butterfly. I used the square root calculation to define my own expected move for July 13: $92.00 (Square root of DTE/365 * IV * Stock price). That gives me a 1630/1720/1810 fly. But I didn’t like the T+1 line slope on the right side, so I broke the wing to flatten the line.

Bought to open: Jul 13 1630/1720/1800 AMZN call fly @ 36.22 1x2x1. It’s got a 49% probability of profit, max profit is $5350, max loss $3622. I usually target about a 15% profit on these. This is delta neutral at almost zero. Very small negative gamma, 34.60 a day in theta, -123 Vega to play for a vol contraction back to HV.

This will be a smart trade if IV drops back towards HV. BUT HV being at 52 week lows means that IV could be leading HV higher. Either way, it will be a fun experiment….stay tuned.

Jun 14 SPY (con’t)

Yesterday I posted a plan for SPY with ex-div tomorrow. The plan involved the assignment of all my #Saf-T SPY shares, then replacing those with short puts for tomorrow expiration….which happen to have the div already priced in, along w/ a little premium.

As it turns out I had about 1000 shares called, but most of my short calls for last night’s expiration expired for full profit.

So I sold tomorrow’s 279 puts to replace the 1000 shares that were called yesterday, at $1.65.

Unless the market goes bonkers tomorrow, this is a guaranteed assignment due to the SPY price action on ex-div day (a $1.10 drop in price is guaranteed).

I have also done the required long put coverage for #Saf-T trades, buying Jul 27 276 puts.

So, for tomorrow: 1. I collect SPY dividend on 2000 shares, $2200 (pay date is actually next friday I think). 2. I collect the put premium on 10 puts $1650. 3. I take assignment of 1000 shares @ 277.35 (adjusted). 4. I can re-commence selling weekly premium on the shares.

TAL

Muddy Waters is Short TAL Education Group (NYSE: TAL US)

Muddy Waters is short TAL Education Group. Investors might recall the dark days of 2010 and 2011, during which numerous U.S.-listed China companies went down as frauds. According to the recent documentary, the China Hustle, there were approximately 400 frauds from China listed on U.S. exchanges. Out of literally hundreds of blatant frauds, almost no company chairman did any prison time. Charlie Munger is fond of saying “Show me the incentive, and I’ll show you the outcome”. Defrauding U.S. investors from China has proven to be a “heads I win, tails you lose” proposition. So, it does not shock us when we see that TAL began fraudulently creating profits as early as FY2016. Since the beginning of FY2016, the value of Chairman Zhang’s shares have skyrocketed from $900 million to close to $7.5 billion. The prospect of becoming Bobby Axelrod rich is a powerful incentive, especially when you have no downside if caught.

Jun 13 SPY Plan

Good Morning! Who agrees with me that the best commercial EVER was the Geico Wednesday (Hump Day!) camel?

So the #Saf-T trades are performing better than I expected, with very high degrees of protection. I have quite a lot of SPY that I had sold calls against for today, so the calls would be cleared by pre-ex-div tomorrow. They are in the money so I’m going to let the shares get called (if FOMC cooperates). Then I will clear and reset the 45-day 40-delta puts (protection is cheap again). I see that the Friday SPY puts have the dividend in them, so rather than hold shares for a div, I will sell a boatload of 1-strike ITM puts for Friday. Selling ITM puts is the same trade as a covered call, so this will be a way of getting the virtual dividend, coupled with extra premium that a call would bring in. Due to the upcoming drop in stock price on Friday for ex-div, I should get the assignment I want to re-populate the share position.

BTW, here is a pic of the price slices on my 3000 shares of SPY. Note the risk control in place on a 10% drop. A 10% market drop yields a 2% capped drop. This is great for higher yield cash storage…way higher than a CD/Money Market, but safe.

I’ll update here when my reset is complete, including the realized profit for the week on this trade.

Here’s a Hump Day remix….actually it’s a tad creepy 🙂

Jun 12

TWTR: Virtual Call Assignment (position closed) for $688 net profit on a 10×8 #Undie . Extrinsic value ran out on the 40.50 short.

Jun 11 Trades

My only trade so far today is a “Ratio Double Undie”…commence rolling eyes 🙂

Playing around this weekend on Undies #UnbalancedDiagonals I found that adding a 2×1 put undie to the mix lowered risk even more without sacrificing a ton on the upside profit.

Work this up in your analyze tab to check it out. This is my actual trade:

NVDA: I picked July 27 expiration for the long to avoid the earnings volatility. July 27 + 8 255 calls @ 14.30, July 27 + 2 270 put @ 14.10, Jun 15 -6 265 call @ 2.10, Jun 15 – 1 275.5 put @ 1.69.

Stats: Theta for this week alone: $1429, Max risk: About $6300, Profit @ $265: $2080

Without that little put add on max risk is just over $9900, so it really cuts risk while maintaining high profit capability.

Today is shaping up to be a theta day…not a lot to do.

Sue

IBD Watchlist

Hi Everyone, here is an updated IBD watchlist with IBD50/Sector Leaders/Big Cap 20. I update this every weekend and would be glad to share.

http://tos.mx/0OPGCo (remember for opening TOS shares: copy link, open TOS setup, “Open shared item”, paste link)

If you don’t have TOS: ABMD,FIVE,HTHT,TTD,TWTR,BZUN,GRUB,TAL,ALGN,NFLX,SIVB,SEDG,ETFC,NVDA,ZTO,LGND,VNOM,HQY,MOMO, GOOS,KEM,PANW,NOW,ZBRA,ADBE,RHT,LULU,ANET,SUPN,PAYC,ILMN,CPRT,ODF,MA,TEAM,NOAH,MU,FND, ENTG,PGTI,IPGP,PLNT,IBKR,TRU,BOFI,GMED,BABA,IDTI,MTCH,HCC,CRM,RP,ULTI,YY,TIF,OXY,FB,INTU,AMZN,PYPL,ISRG,CLR

IBD50 has an ETF: FFTY

There’s a lot of great names in the list now for wonderful synthetic covered call opps–my favs: TWTR, GRUB, ALGN (I haven’t done anything lately in this, can be a little hard to exit), NFLX, NVDA, PANW, RHT, MU, BABA, CRM, AMZN, ISRG, MA

My favorite indicators right now are pretty simple: MACD in a buy config above the zero line for any new longs, the “Sue AD Score” that was shared in the last week, and Ichimoku, oh-and recently the “DMI Oscillator” with an ADX overlay vs the regular DMI. If you have the Sue AD score, just read the description inside the code for more info on it. Indies come, indies go, but “Sue AD” stays on my charts all the time–in fact I’ve added it as a column on watchlists for sorting–very useful for sort/scan.

I have a big desire to help other people be successful in the business. The first step in doing that is finding my own success, then sharing with others. This is a very hard business. There are no shortcuts. It takes seasoning, mastery of self, lack of emotion—but plenty of passion. Constant learning, developing, testing. Riding highs, riding storms. Embracing risk, but controlling risk. But, I’m preaching to the choir, because, from what I see…everyone here at Bistro knows this already 🙂

Sue

Jun 8 trades

Busy day here! Every single one of my #Saf-T trades is in the money for expiration, so I’m executing share calls and resets on them in multiple accounts.

LMT: I rolled into strength this morning, which means I rolled at the day’s high. This means that I didn’t collect a whole lot on the jun 8 calls ($222 of $1416) but I sold really high for next week, $2550 worth. If you recall, I’m now using LMT as a proxy to recover RTN losses (apples to apples in just one account). Last Friday the LMT-RTN was $-3858. Today it is $-3157. Gettin’ there.

My total premium sold for today was $14,894. It looks like I will collect $10,184 for a 68% retention.

I almost forgot my note-to-self about ETF divs next week and started a roll into next week. I quickly fixed that. All my SPY rolls are to Jun 13, the TQQQ rolls are to Jun 22, pretty far OTM.

Everyone have a fun and safe summer weekend! It’s been a great week for covered’s.

Oh…anyone in TWTR short calls….just keep an eye on extrinsic value, no action today necessary.

Jun 7 Trades:

ADBE: This started as an Aug/Jun 15 #UnbalancedDiagonal 7×5, until I realized I had forgot about earnings next week. So I scratched the qty 5 short calls for Jun 15 and sold 7 instead for this week. I took profits out the gate this morning for $602 total. I’d like to thank @mamacash for the idea to flip it to this week. Update: I did NOT see this drop coming, fully admit I had some luck jumping on profits at the open for my exit. My closing timestamp was 07:31:19, one minute after the open.

AMZN: Opening trade, protected #UnbalancedDiagonal 1. Bought July 1650 call x2 @ 80.05 2. Sold Jun 15 1700 call x1 @ 18.87 3. Bought Jun 15 XLY 108.5 puts x10 @ .38. One thing I’m learning at the pit is using partial profits on one trade setup as a sacrificial hedge (aren’t all hedges sacrificial…it was fun to say 🙂 ) in either the same or different/correlated product. It seems obvious, but I haven’t been doing much of that. So the XLY puts take $380 of the Amazon profits for a little extra downside protection. I continue to peel away more and more risk for trading this behemoth. Just a few weeks ago I was taking $160K risk, now it’s down to around $10-12K of risk.

Still to manage this week: I still have zero assignments on the Saf-T’s, LMT x2 (LMT lookin’ good! Will definitely put a dent in the RTN loss), that’s it!

June 6 trades

BA: I’ve got two of these on, a #CoveredBackRatio and an #UnbalancedDiagonal . The CBR had a virtual call assignment today, closing the full position for a net $2964 profit on an 8×4 setup. The UB I put on right before the close yesterday and is up smartly today.

TWTR: Opened a new Unbalanced Diagonal: Aug 37 call x10 @ 5.25, sold Jun 15 40.5 call x8 @.92. I’m really loving these unbalanced diagonals, how you can really bring the long strike up closer to ATM, thus lower risk, and at the same time bring the short call down closer to ATM (collect more $$), but the ratio makes the trade work so well.

SPY added a few more #Saf-T contracts. I’m still waiting for Saf-T shares to get called so I can reset them. I decided I make more profit waiting for full profit and paying the assignment fees, vs front running the assignment myself and giving up a few cents in order to save the fees.

I expect a really slow day from here on. It’s a “theta day” where I just sit back and catch the pennies.

Sue

ETF Dividends Next Week

Don’t forget about dividends next week if you are rolling any calls on ETF’s. Remember the div rule on call assignments: The div has to be more than the extrinsic value for your position to be vulnerable. IF you are assigned for the dividend, you also are PAYING the dividend to the new share holder, if you didn’t know.

June 5 Trades

TWTR: Out the gate executed a virtual call assignment for $1889 profit on a 10×7 #UnbalancedDiagonal . That’s multiple thousands of profit (in a couple accts) since I suggested the TWTR stock replacement idea to y’all about 10 days ago. Flat TWTR right now.

June 4 Trades

Ahhh, I love June!

I have 2 “Virtual Call Assignments” today due to extrinsic losing most of its value:

TQQQ 6×3 #CoveredBackRatio netted $837 (closed entire position)

MSFT 14×8 #CoveredBackRatio netted $1120 (closed entire position)

Rolled MU Jun 8 to Jun 15 qty 5 calls for $670 profit on jun8

MA debit rolled calls from Jun8 192.5 to Jun15 195 for -$654 on a 2-lot

“Thongs”

@MamaCash is the one that comes up with all the creative trade names (Atomic Alligators). She just told me we’re going to start calling the “Theta Long” trades (like covered calls, etc) “Thongs”. I won’t hashtag this, but thought you’d all laugh with me.

Sue

Augen Score

I’m watching the SPX Augen score inching up into high territory. It will hit 6 today. As you recall, the score is the number of 1-Standard Deviation up moves in a 21 day period. The higher that score gets, the more it points to a little too much frantic buying. I’ll look through everything this weekend for clarity on that score going up after a big correction. But anyway, for right now my plan is to stop any new buying at a “7”, take profits at “8”, flatten at “9”, get VIX calls or SPX short delta at “9-10.” In fact I have already taken steps to look through my whole portfolio and ask myself if I really want to hold certain positions. In the last 20 min I have cut:

ISRG $1215 net profit

IBM $200 net loss after many many income rolls

CARB $472 net gain on covered call

SBUX cut my short for $100 gain

TSLA $ not sure, don’t have a baseline

Took profit on VXX puts.

SHAK $244 net profit

I’ll write more this weekend about observations on the Augen score going up after a correction.