Looks like it was a quiet day for a lot of people here.

1. May I please call these “Fuzzy” trades? I love them and I’m doing a lot of them (#SyntheticStock Diagonals w/ protection and hedge income—From now on known as #Fuzzies. To me, the Fuzzies have two stages, stage one is recovering the net debit of the trade; Stage 2 is recovery of the spread risk. I spent time this weekend looking at and scoring candidates. The “score” is basically the number of weeks of hedge income that it takes to accomplish Stage 1. The fewer the number of weeks, the lower the score. I’m looking for Fuzzies with a score of less than 5, less than 4 even better. I have a picture in my head of having a portfolio of 10 Fuzzies, each with $10 spread risk, bringing in 10-15K a week in income. So I’m testing these aggressively.

I have a TOS scan for finding high-return covered calls and puts, and it turns out it’s a good scan for finding Fuzzy candidates with low scores. Here’s the scan http://tos.mx/vKzR27

So back to Trade #1: CELG. I happened to catch a big bullish fund order for a Jan risk reversal, so a CELG #Fuzzy was my first trade of the day: Mar 110c/-110p/+100p, Dec 15 110 c. Net debit: 1.38 with a “Score” of approx 2.38 (2.38 weeks to cover the core debit)

2. Oh…here’s a nod to @hcgdavis for the Alpha Shark indicator. Got it. Love it. So scalped a bunch of /NQ today while taking it for a test run. Ended up +$305 on small-lot scalps. Enough to pay for the indicator 🙂

3. NTES. Now this was a franken-trade. It started as one 10-lot #butterfly. As it dropped added another 10-lot butterfly. Last week added a 3rd 10-lot butterfly. Was finally able to close it all out today for a $157 loss. Believe me, I’m happy with that!

4. #Bitties Closed! SPX x 20 lot, NDX x 10 lot. Got 50% target on all of them. The SPX bitties were 7DTE, so was happy to close them asap given the gamma risk. Net profit $1150.

5. Reset 17DTE SPX #Bitties. The Dec 27 2630/2625 for .85 cr x 20

6. NTNX I’ve been holding 703 shares, took 603 off for about $950 profit. Some day they’ll be acquired so I’ll always keep a hundred on. Great stock for swing trading, so will load back up on any dip. My max size position is 3000 shares, but I never seem to get the opp to add that many on.

7. QQQ #JadeLizard closed for 50% profit, this week’s expiration

8. SPY 266/267 #BuCS closed for 90% profit. This was bought based on #UOA (unusual option activity). SPY trades massive volume in fund flow, obviously—but it’s almost all put hedges. Every once in awhile a big bullish trade hits the tape, and those are ones for my attention.

9. NUE Closed a BuCS for 50% profit, this is another one that was bought on #UOA

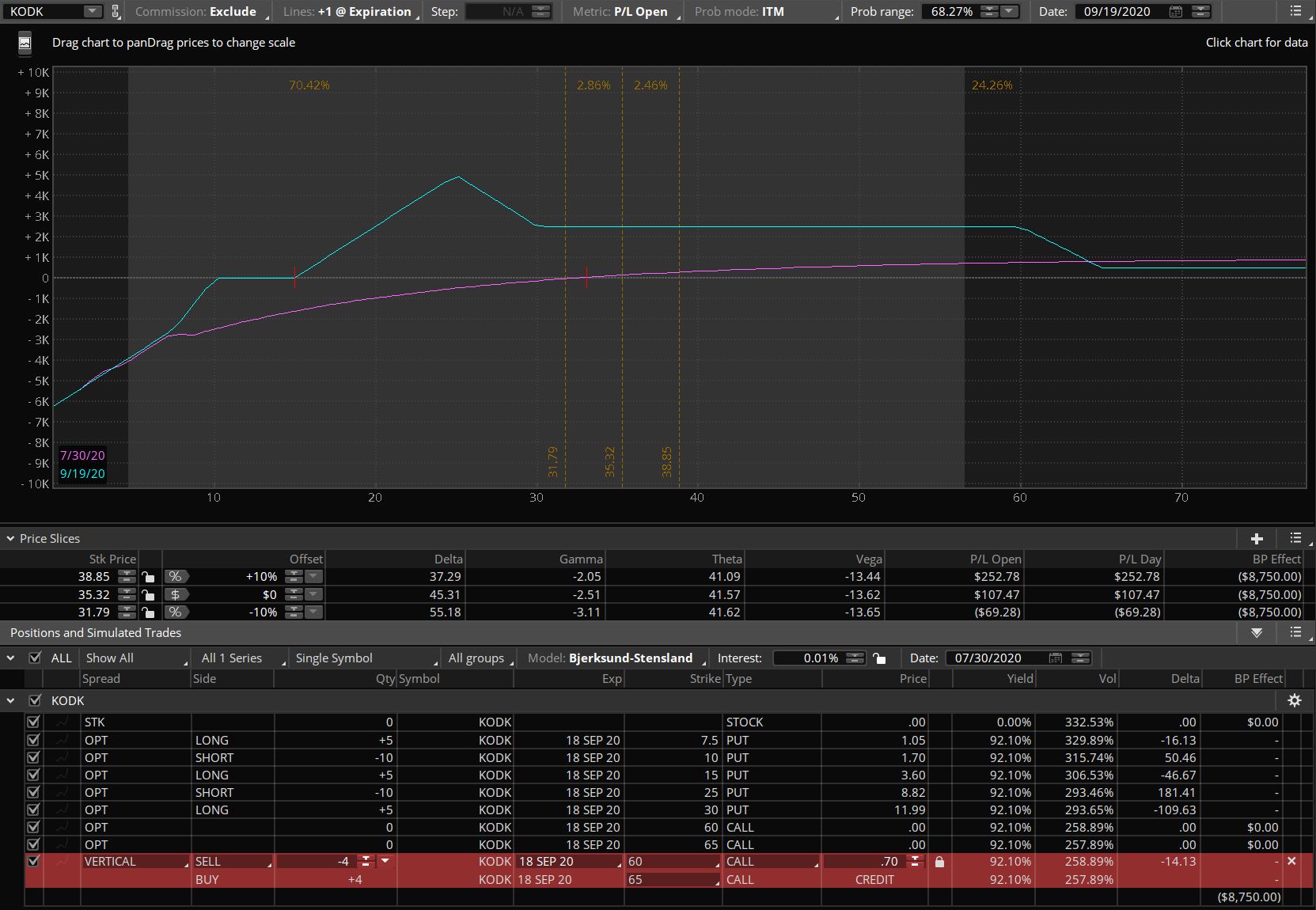

10. NUE Opened a #Fuzzy Apr 60/60/50 for 1.87 core debit, Dec 15 62 call short for .56, Score is 3.3. There was a lot of bullish option flow on this today….all the way up to the 70 call line.

11 NUE spec trade based on #UOA bought 100 Jan 70 calls for .16, just looking for .21 as my target

12 MU #EarningsRunUp added two more calls to the trade from last week. Looking for 30% profit on these and must close before earnings announcement.

13 AMC #UOA There was unusual activity on AMC right before the other cinema merger happened last week. Turns out AMC confirms they’ve been approached too, regarding investment options. I’m glad I sold a few puts when I saw the fund flow. Netted 50%, $370.00 on a 10-lot

14. MSFT I like to layer on a lot of different MSFT trades. I love what they’re doing with Azure. However I saw a lot of January put buying today on MSFT, so I cut a trade short (#BuCS) for 28% profit vs. the 50% I was looking for. I still have on a MSFT #Butterfly that I’m watching closely. 80/85/90 for Feb.

15. ALGN This is the last of my trades from the tech crash. I defended it resulting in half what the max loss would have been. All closed now for $1150 loss. Classic case of thinking it would come back. Could have been handled better, but could have been handled much worse. I wouldn’t mind resetting with a #bitty or #PutRatioSpread the problem is that it’s just really thin. The Market Makers are not the worst I’ve dealt with (ISRG, KORS, ULTA are worse) but it’s still a struggle.

16. TWTR Opened a #Fuzzy in a 401K. I again saw some large bullish fund flow on TWTR and it had a good score. Mar 22/22/18 core for .78, sold Dec 22.5 call for .46, score is roughly 2. Not sure how this one will work out, but I’m still developing the perfect candidate profile for the Fuzzies.

@fuzzballl I hope you are ok being the namesake on these trades. It’s cute!