So my 5 week full time trading experiment has been over for about 4 weeks now. Not trying to brag, but had my second best trading month ever even in a very choppy market. Over 9% returns for the month on my total portfolio and now up 38% for the total portfolio for the year as of this last weekend. Several losing trades in there as well.

So ran a few experiments and noticed a few things about the market in live time.

1. While tastytrade has found that the best time to sell options is 45 DTE, it takes a long time for the decay to occur, especially if the ticker moves. I found that there is a huge theta crush from 21 DTE to 14 or 7 DTE for OTM options. You will be closer to the money than 45 DTE, but the theta decay is huge. I may have posted this already and if so sorry for the repeat, but I was in EXPE and several other trades. Had opened both 45 DTE and 21 DTE. It took 3-5 weeks for the 45 DTE options to crush 50% but only 10 days for the 21 DTE to do the same. Recycle capital faster, make more $.

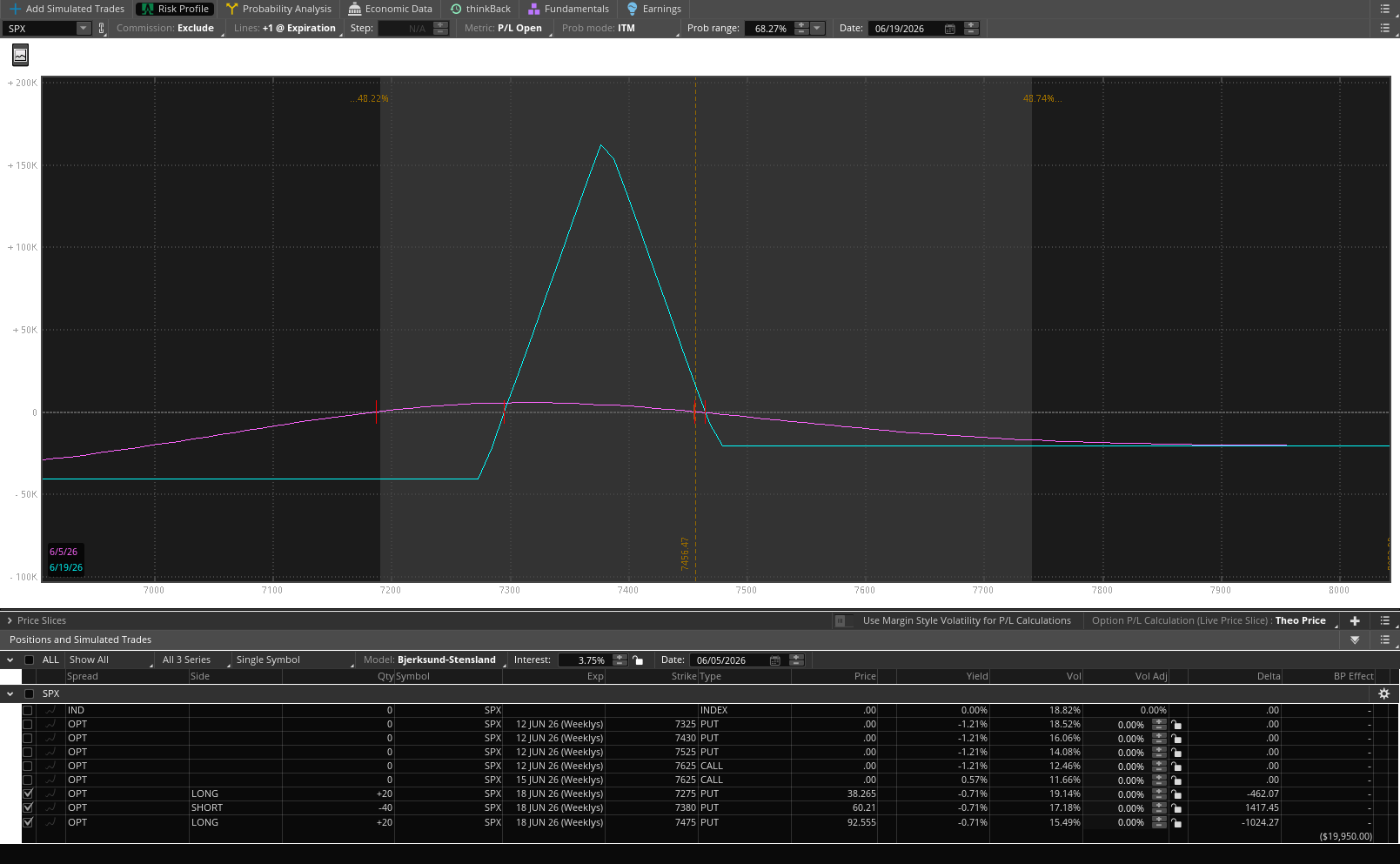

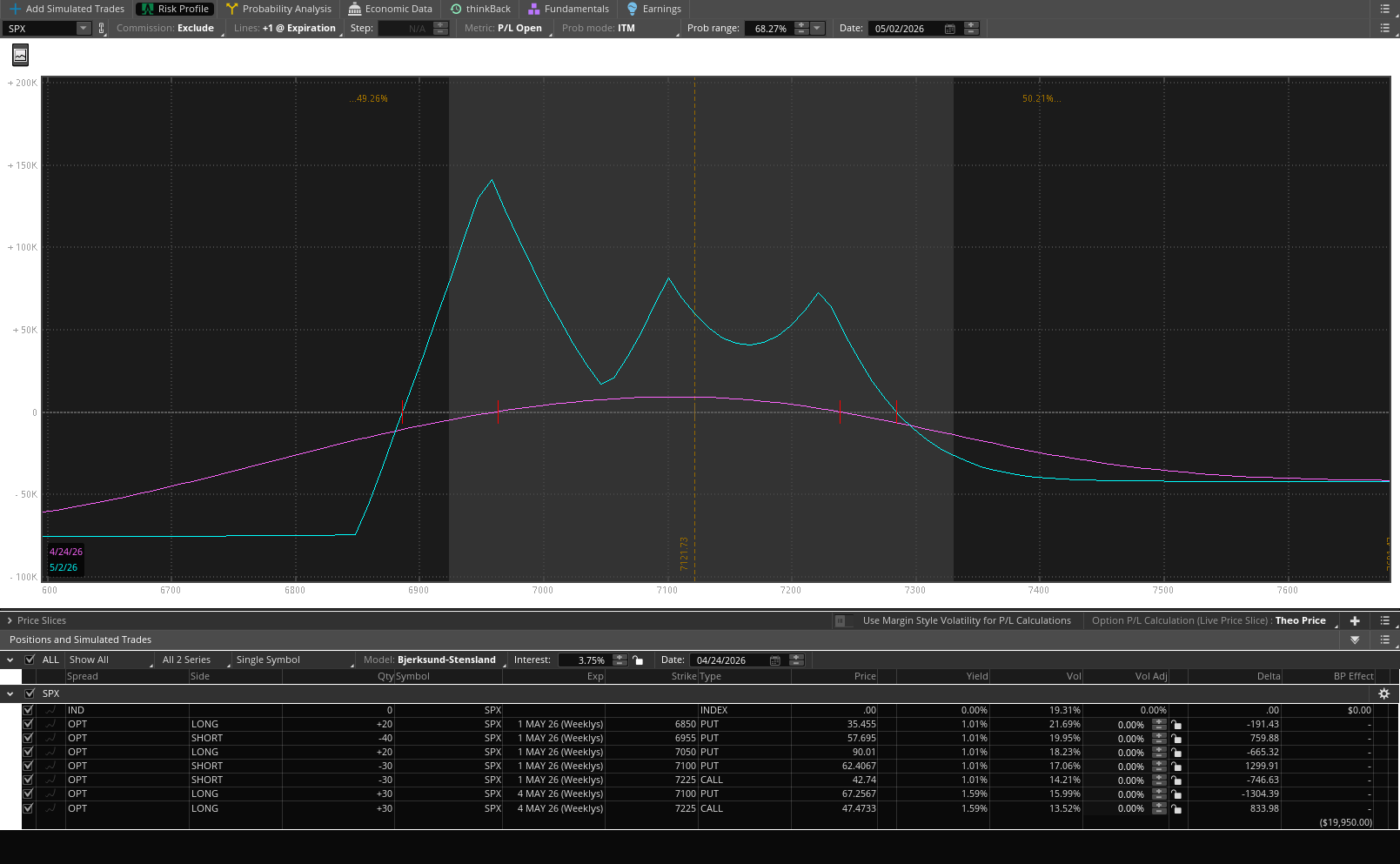

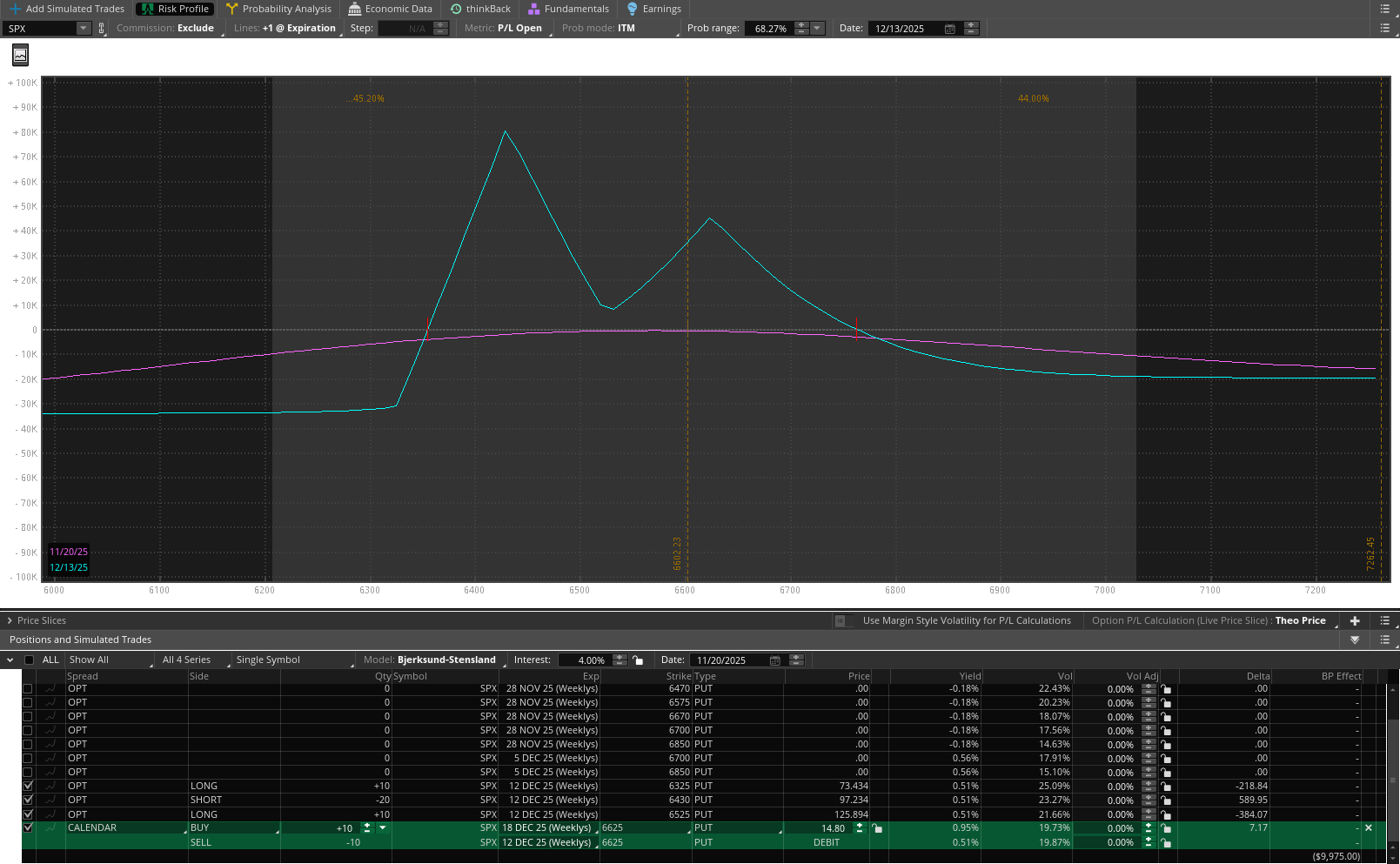

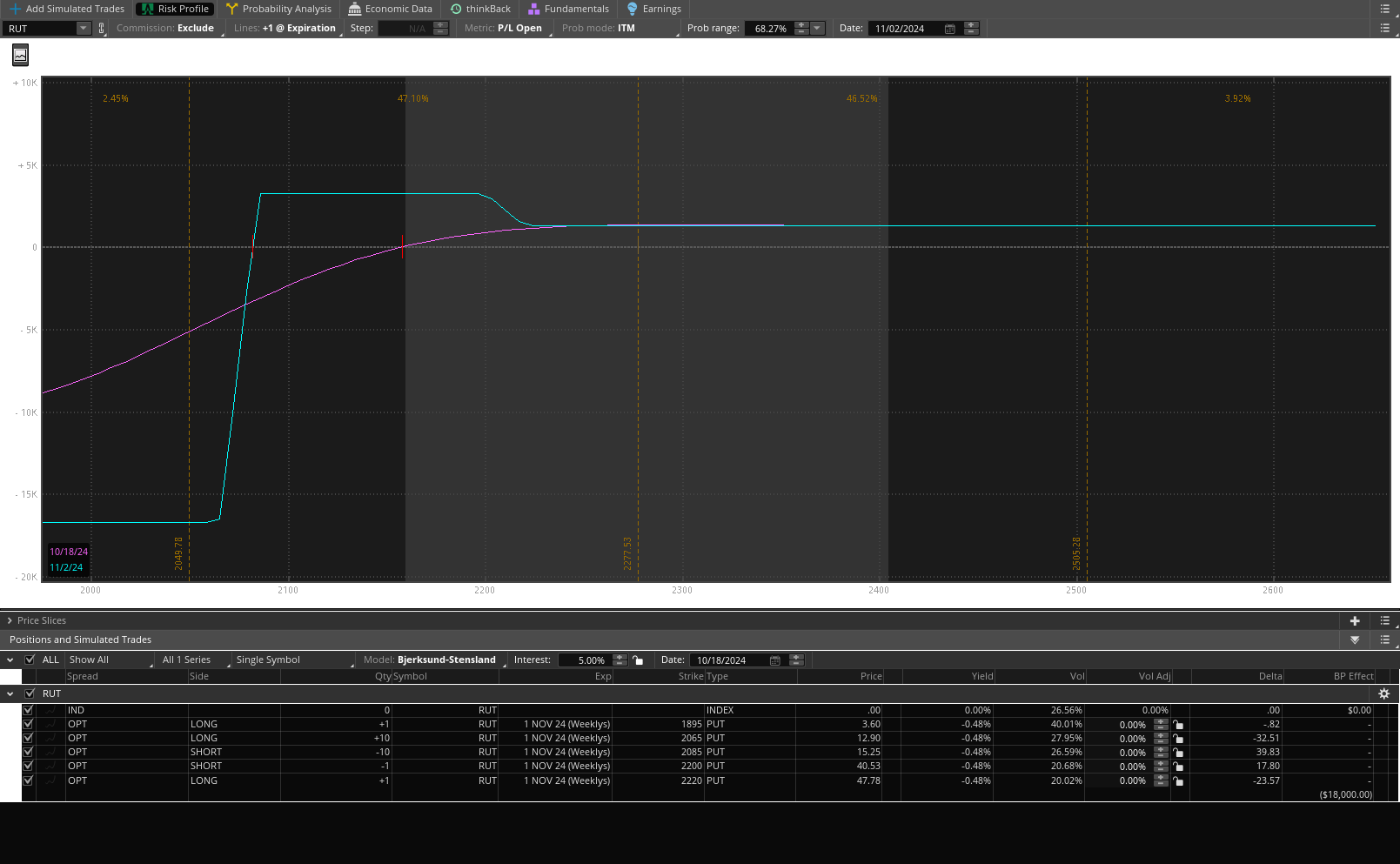

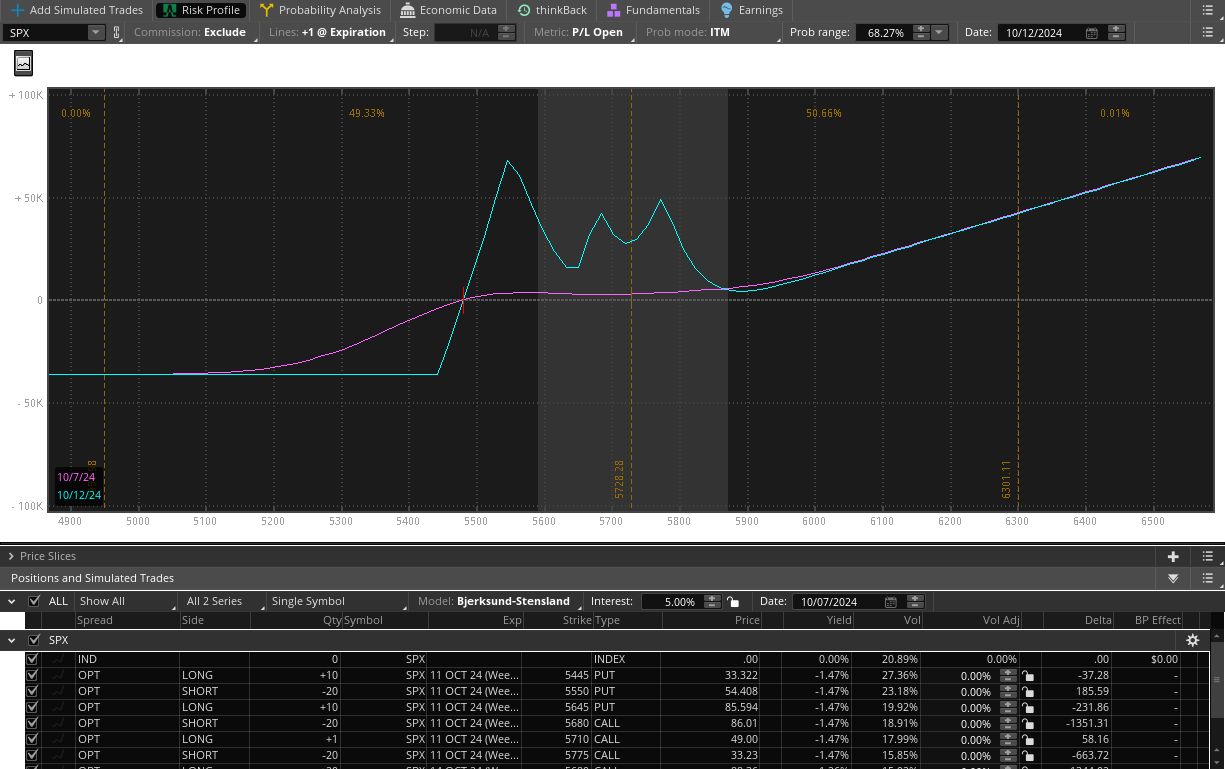

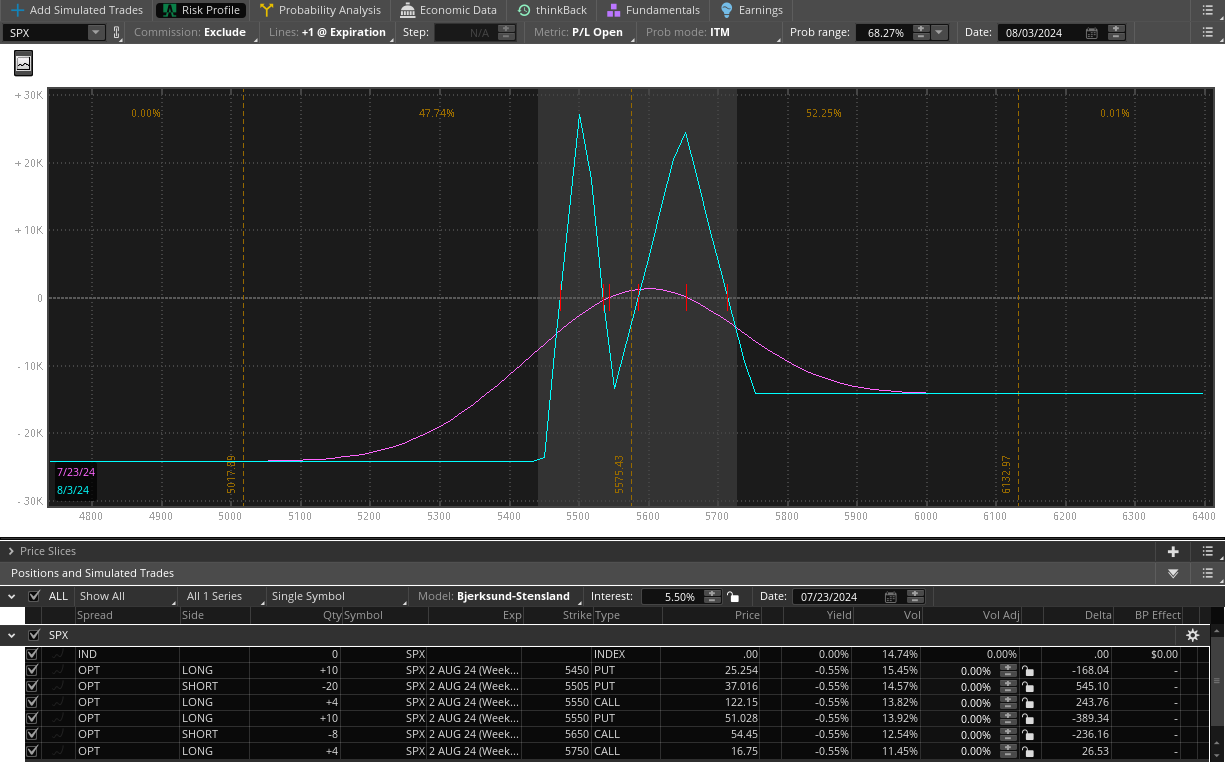

2. #spycraft version 5.1 or so idea. The weekly income is awesome, but then the 5 STD moves crush all your profits and then some. I have been setting up hedges using /ES and SPX and keeping them on almost all the time now. On the big moves down, you can roll for cash and reset the hedge to new levels. You can set up a longer term hedge 90 DTE or so to cover you max loss basically scratching the trade. It will cost more but will prevent the losses. I have not figured out the ideal ratios yet but stay tuned. Plan is to sell 21 day IC or credit spreads, use the cash to buy a few hedges, then roll weekly and keep cash coming in to reduce the hedge cost basis to zero. Other option is convert the spreads to ratios or butterflies. The butterfly seems to limit the losses faster and then if whipsaw no additional losses.

3. Keeping hedges on allows you to be a much more aggressive trader. If the SPX goes to zero, you hedges will be worth much more than your portfolio was. Because of the volatility expansion you can also buy cheaper options than you thought. I have been planning for a 10% drop as my starting point. Then figure out which option would be worth 10k at a 10% drop. Then you can figure out how many contracts to cover your portfolio. Best to do when the VIX is 12. The black swam events seem to be occurring on average 2 times a year since 2015 but are only supposed to happen once every 5 years. I will always have a hedge and will pay for it by selling options or rolling profits from the hedges.

4. #jadelizard and #lizardpies are hugely adaptable. You can often move 3-5 strikes and still take in a credit. You can also skew it to up or downside and really increase returns. If runs through the upper strikes just let it all expire, take the cash, and reset the next week. If it moves down, reset the straddle ATM.

5. #pietrades are still the cash machine but can convert to jade lizards or LEAPs if it really implodes on you.

6. Staying out of earnings trades has been helpful to my equity curve.

7. Staring at 1 and 5 minute charts is mind numbing. Congratulations to those of you that can do it and trade directionally. I can’t and have a lot more fun things to do. I will stay mostly non directional with a slight directional bias and enjoy life and my free time. Most of my trading is on my free time so the less I have to spend trading is more time to do other things. I personally will not take any trade on anything shorter than a 15 or 30 minute chart but my real triggers are now hourly or 4 hour for the weekly trades.

8. Spreads can save your bacon in really volatile markets.

9. Keep enough cash on the sidelines for adjustments and opportunities.

10. There is always another trade or opportunity. If you feel pressured to make a trade, it is probably a bad idea. The less emotional you can be also the better the adjustments/recovery you can make. Think before hitting the confirm and send button and have a plan and stick to the plan if the trade goes against you. Be mechanical in your trading and adjusting. It may seem boring to some but the reason I trade is to make money. I want adrenaline I will go kiteboard or ski and hopefully not break my face again.

11. Having a group to trade with is like extra eyes on the market. Everyone sees different opportunities. Thanks for sharing 🙂

12. Being a specialist pays off. I am a family practitioner but specialists make more in the medical field. Also true in the market. Have a handful of tickers you know, watch and trade. They all have their own personalities and once you know them it is easier to trade them. I think once you have above 10-12 names you are probably trying to do too much. Trading the same tickers over and over has improved my consistency and results. Sure, play the occasional lottery ticket but to pay the bills stick with what you know. And also make sure your tickers are diversified.

Cheers, Chris 🙂

#spx1dte, #spzx1dte