Obviously what I have been doing the last 4 months has not been working. Hit all time low balance again Jan. 4 this year. So I am going back to what works and has been proven through several market cycles and rebuilding the equity curve. At least last month have recovered and higher than the Feb. 6, 2018 SVXY losses and lowest balance from then.

So I am clearing out losing trades, closing a bunch of #fuzzy, some at profit, some at loss, and re-deploying capital. My trading will mostly consist of #pietrades, #lizardpies, #spycraft and the occasional directional play/scalp and a few #fuzzy

Some closings today, but have 2 more weeks to clear out the primary account.

#fuzzy

EOG 110/110 closed for 5.16 loss per contract. It is so far ITM can’t get decent premiums anymore. My intial loss was 17 so this tactic works.

EXPE closed the back ratio credit spreads, left with 120/120 and 125/126. This is sitting on a profit and will close it over the next 2 weeks as the shorts expire. Cb 9.43 and right now can close for min. 11.45. another week of decay that will be better. Lost $600 on the credit spreads after butterflying to control risk (could have been 2000).

MU 35/35 now ITM Cb 14.80 and will roll next week.

WDC 40/40 cb 18.49 and waiting for the short to implode after earnings today.

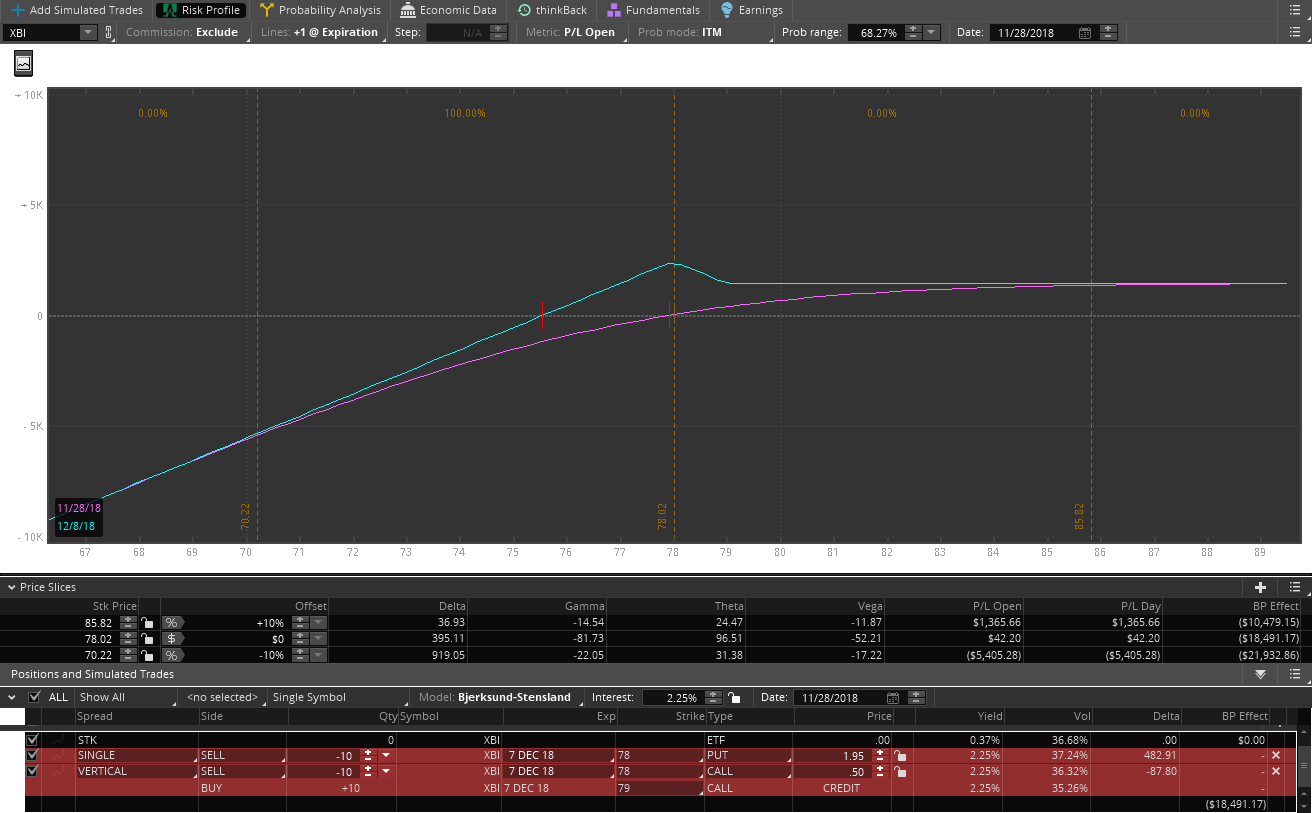

XBI 80/80 cb 13.97

LNG 50/60 rolled 15 DTE for 0.5 credit for 13.56 cb.

GILD 67.5/69 rolled 15 DTE for 1.3 credit. Cb 7.60

#pietrades and #lizardpies

XBI 78 put 82/82.5c 8 DTE for 1.26 credit

TQQQ 50 CC rolled out 15 DTE for 0.45 credit. CB 57.56 so will manage aggressively

TQQQ 50 cc lot 2 cb 57.30 same

LNG STO the 8 DTE 63 put for 0.92. CB 62.08 if assigned. LNG is my best performer for the year so far 🙂

#spycraft

Batch 1 closed for a $214 loss after the back ratio adjustment did not work. SPY reversed.

Batch 2 closed for a $344 profit, but only because tradestation messed up and sold 20 contracts of the put side instead of 10 so even with the back ratio that did not work I made a few $. Now I am on hold in this account until tomorrow. Tradestation does not give you credit for closed trades until after midnight so I only have $614 buying power in this account until tomorrow morning. Another reason I prefer TOS over TS.

What I have learned most recently.

#fuzzy works well but I think the real value of them is to close them once you have a profit. The EOG trade would have worked if I had just closed it early. If you still like the trade, reset the strike prices. I will use these as shorter term trades out 1 week or a month, take my profit and reset. Commissions are cheap enough to do that most of the time. A 6 % return in one month and then resetting is 96% annualized. Instead of trying to take the cost basis to zero will just take profit and reset. Will probably just use a 90 day option for the long side.

#spycraft

I think the best adjustment when the short strike is challenged is to butterfly it. You can set a defined p/l by broken winging it and skewing it if you have a bias. Just to stop losing can simply butterfly it. Seems to be the cheapest way to do it and least affected if it reverses. Yes you may lock in a loss, but much better than a full loss on the credit spread.

#pietrades and #lizardpies

Upside directional bias set it up as a synthetic long.

No directional bias, set up as a straddle jade lizard.

Downside directional bias set it up as a strangle jade lizard.

But I think setting it up as a jade lizard initially gives more flexibility in managing because of the extra credit. I will be doing A LOT more of these.

Can also leg in and out depending on how the stock moves.

Pouring here so going to work out in my garage gym. First bike race is in 8 weeks so need to lose 10 pounds and make friends with my fast again 🙂

Hope everyone has a good expiration!