#ShortPuts – What do you think about this theory?

Looking back over the last 18 months where I’ve been predominately just selling puts and covered calls I realized something. Besides my crazy, high risk, entries I rarely receive any stock. Maybe 1 out of 10 times at the very most.

So, with that in mind, here’s my idea…stealing a little of this from Whiz but with my own twist. Whiz will trade very narrow spreads that are relatively safe but uses many contracts. He either wins or loses and rarely adjusts and his wins seem to outnumber losses enough to where he makes pretty darn good money. I was very skeptical at first but after watching him a couple years he really does do pretty good.

My theory is to do something similar but with my rule of never doing it on something I don’t want to own. I’m thinking that on the put sales that you’re reasonably confident on to crank up the number of contracts and use spreads. Then one of two things can happen…

1. The trade will bring in multiple more times the profit of just the put sale

2. The trade will implode and you’ll get stock at a limited downside

Now my strategy would be to allow assignment of number of shares I’m comfortable with and roll the spread loss into the basis and recover with call selling. (Whiz would just take the loss and move on) To help minimize the damage I would close one of the long puts (or however many shares you are willing to take) right at the close on expiration day. This would lock in profit there and leave one short put to get assigned.

If this losing situation were to only happen once every 10 or so trades the additional profit on the winners would be very nice.

Let’s use LULU as an example. I would only want 200 shares max if everything goes bad so that would be selling 2 naked puts the way I’ve been doing it.

Sell 2 Jan 24th 210 puts @ 2.05 for $410 premium

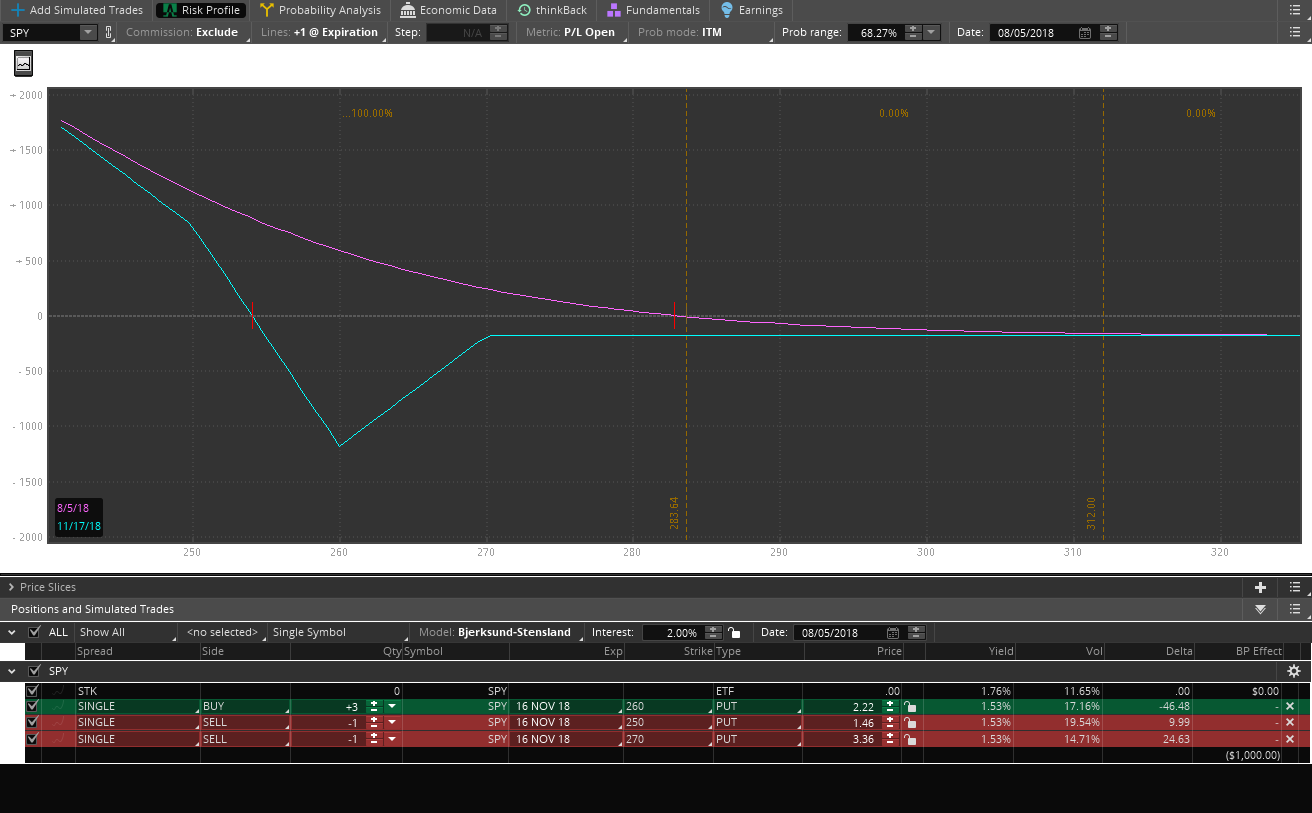

My new trade would be using say a 5 to 1 ratio on the sales vs stock I’m willing to receive and selling 5 wide spreads. You could use more or less depending on risk tolerance. The more you sell the more you have to make back on an implosion but also the more you make on a good trade.

Sell 10 Jan 24th 210/205 BuPS @ .82 for $820 premium.

Based on the TOS analyze of the spreads the max loss would be about 4180 at expiration on an implosion. My theory would be to sell two of the long puts on Friday afternoon and receive the stock from the two naked shorts that would leave. Whatever those puts bring in the 4180 loss would be reduced by that amount. The worse case scenario would be for the stock to end up right at the bottom of the spread where the longs wouldn’t be worth anything and the spreads would be at max loss. Of course the stock is at a higher level to start call writing which is good.

Let’s say at expiration the stock is at 200. The position would be at max loss but the 2 longs I’m selling are worth a total of one grand reducing max loss to 3180 and giving me 200 shares. The stock would be at 200 and my basis would be at about 226 (210 put sale plus 16 dollar loss on the assignment). I would have to depend on call writing to get that back.

So big picture, if you did this trade 10 times total premium would be $8200. If you happened to get stock once you’d be in the hole the one time and have to recover.

If you did the trade 10 times just selling the 2 naked puts the total premium would be $4100 and you’d own the stock at some unknown levels depending on how much it dropped.

With my “theory” at least the starting point for repair would be manageable if the thing were to “pull an ULTA” on me.

Another twist on this would be to buy an extra long put. It would reduce overall profit but really cap losses on an implosion. In fact if the stock were to tank enough you could make money on the drop. Here’s a sell 10 buy 11 scenario. Max gain drops to about 700 but losses start getting reduced as soon as the spread gets blown out. This would probably be well worth the extra buy.

Hope some of this makes sense!!