Unhedged #Fuzzy (this is really long!!)

My good friend @MamaCash calls these “Unhinged Fuzzies” and that always makes me smile. Over the past couple of weeks, the power of these revealed itself to me. So that’s why I called Mr @fuzzballl an onion last night 🙂 These fuzzies are revealing very important layers of opportunity to apply in different circumstances.

Yesterday morning I woke up remembering one of John Carter’s classes from a few years ago where he talked about “HPTM” High Probability Moments in Time. Couple that with Jeff’s upside VIX warning and Eureka! HPTM is here. My immediate thought was “put down all the toys.” No more 2-lot 3-lot 5-lots on various tickers. Time for BIG laser focus on SPY/SPX RIGHT NOW. However long this window lasts this is when fortunes are made.

Before I talk more about yesterday though, let me give a couple-paragraph primer on unhedged fuzzies, because I know some people are following this carefully. And when the check-out girl at the grocery store this weekend asks you “why not just buy calls instead of a fuzzy,” here’s your answer:

100 shares of stock = 100 Delta (P/L moves 1:1 with stock, it is stock)

1 At-the-Money call = 100 shares of stock = 50 Delta (only moves 1/2 with stock)

(1 ATM Call) + (- 1 ATM Put) = 100 Delta—this is a synthetic long stock position with 100 delta

A synthetic stock position is a very cheap way to approximate ownership of stock, but there’s not a huge advantage in it. In a 401K you still are required to hold the full buying power risk of the naked puts, in margin accounts there is some buying power reduction on the naked puts. But note that you have a large naked put position with synthetic stock.

SPY 1000 Shares: $273,000

SPY 10-lot synthetic naked put risk: $273,000 (indulge me in being less than precise)

Buying Power required: $273,000

Enter the 3rd leg of the Unhedged Fuzzy: The Protective Put

This is done in the same expiration cycle as the synthetic, in fact on the same order (hold your control key to add the leg). Currently I’m using $4.00 spread-risk on SPY. Here’s what my orders look like:

BTO 273 Call

STO 273 Put

BTO 269 Put

What just happened? All of this is on a 10-lot:

Risk: $4,000 (+ trade cost) vs $273,000

Income: UNLIMITED 700 delta ($700 for every $1.00 move in SPY (vs $500 for ATM calls))

Buying Power: FREE for portfolio margin, $4,000 for IRA vs $273,000

Let me give you a real example of how I recently used this trade that I’ve not yet reported. I really like the Gorilla Trades service. I’ve been a subscriber for probably 10 years. If I’d been a faithful follower I’d probably have $25 Million by now, but I’ve not been a faithful follower. Last weekend they came out with their top 3 picks for 2018, all 3 biotechs, all 3 are take out candidates for 2018: EXAS, EXEL, GWPH. All 3 look awesome to me! Do I want to buy 1000 shares of each and just sit on them for 6 months waiting for a buyout that may or may not come? Some of these have very high vol, meaning the market thinks they are either zoom or doom stocks. Do I want to risk 1000 shares on doom? Enter the unhedged fuzzy. Here were my Tue trades:

EXAS July 55/55/45 for 3.56 x 10 (this position is up $2,740)

EXEL May 31/31/27 for 2.55 x10 (this position is up $150.00)

GWPH May 135/135/125 for 9.65 x 5 (this position is down $1175.00 but only because of weekend b/a spread, it’s been up and down )

Point is….I have nice positions tucked away on 3 biotechs using very small risk and buying power….any one of these 3 could bring in a $40K windfall (or more), but if it doesn’t, what is my risk? I’m not sitting on thousands of shares of speculative stock. EXAS I’m most comfortable with, their product is amazing, so I took bigger risk there with a $10 wide protective put (they present at the big health conf this next week). EXEL I’m less familiar with, less risk. GWPH, less risk with less size.

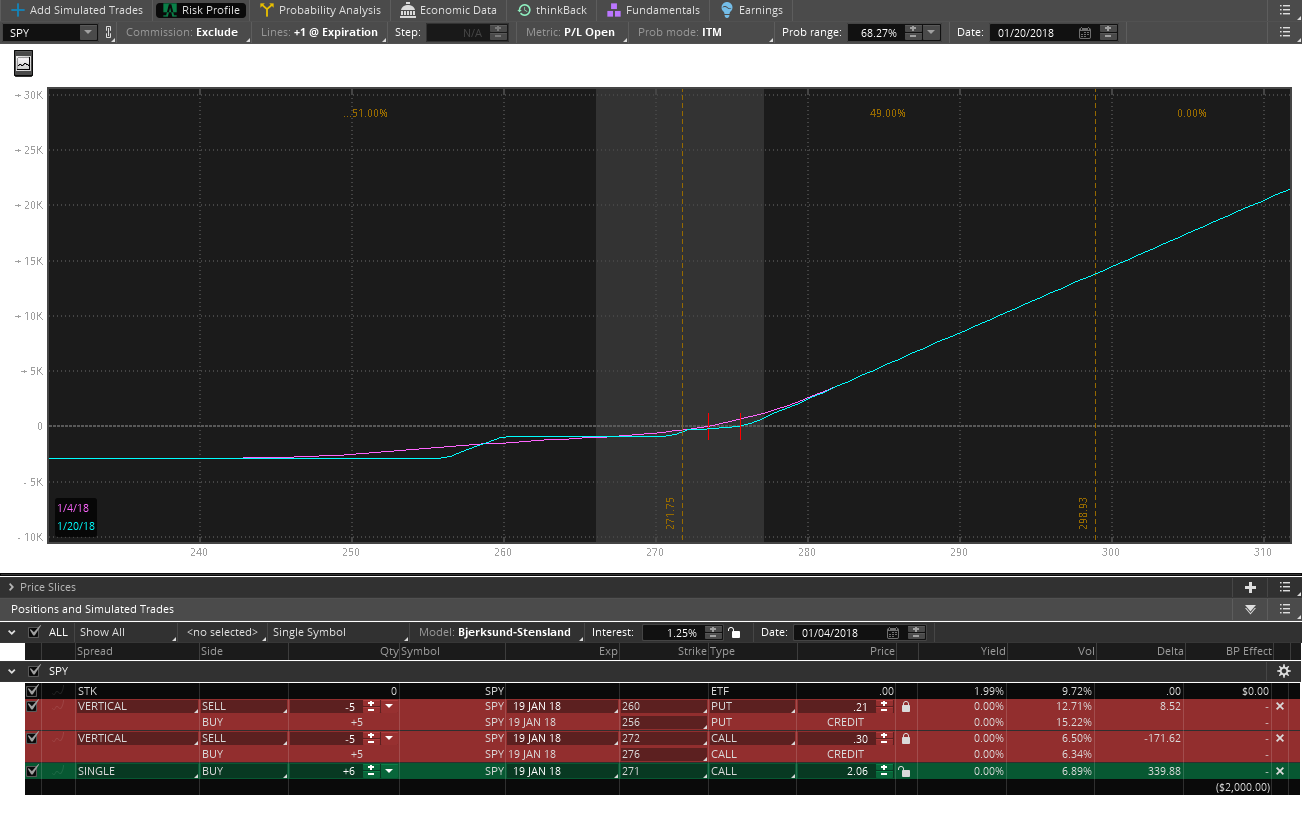

Alright, back to yesterday morning. Woke up, big opportunity still in the markets. But its Friday, we’ve breached key expected move targets (not just for 1 week but 2 weeks). Still I removed hedges from 40 SPY fuzzies that I had, I added 30 Feb SPY Fuzzies for about 2.30. That gave me 70 SPY Fuzzies. 70x $272 x 100 = $1,904,000. Buying power used, next to nothing. Risk: $28,000 + trade cost. I still have a hard time believing the power of this myself. I rode this to the sign of resistance around 2 hours before the close, it was pretty quiet for most of the day. Grabbed about .50 of SPY move = $3500. Then I closed the extra 30 fuzzies and put fresh hedges on the other 40. When resistance broke and we had strength into the close I added another 10 unhedged fuzzies on for Monday morning. So I’m currently sitting on 40 hedged, 10 unhedged. My intent was to keep these trades open longer, but I tend to be a nervous nelly on Fridays. However, this is a tool I plan to use over and over; shorter duration expiries on limited trend trades, longer duration (hedged) on income trades.

This is really long, I know, thank you if you’ve made it this far. These trades, with their limited risk and effective use of buying power, are showing great versatility for trending/contraction/income/momo/long/short/hedge/speculation opportunities. Hope this was helpful for those of you still getting the #fuzzy concepts.

Sue

#spycraft