Sometimes it takes blowing out an account (or 2 on SVXY) to really make you focus. I have always learned more with a 2 x 4 to the back of the head than with a gentle nudge. So I went back to the drawing board, looked at all my trades that worked, what didn’t, and some alternative ways to trade and it has allowed me to concentrate on what works since Feb. 6, 2018. You would have thought I would have kept something in my head from Aug. 24, 2015 but apparently not.

So here is what I have going forward in order of how I am trading in the future.

#pietrades. This is my bread and butter, pays the bills, making some of the losses back, easy to roll and adjust and works week in and week out no matter what the market does. Occasionally get stuck with one for a while, currently GM but can usually roll them to even.

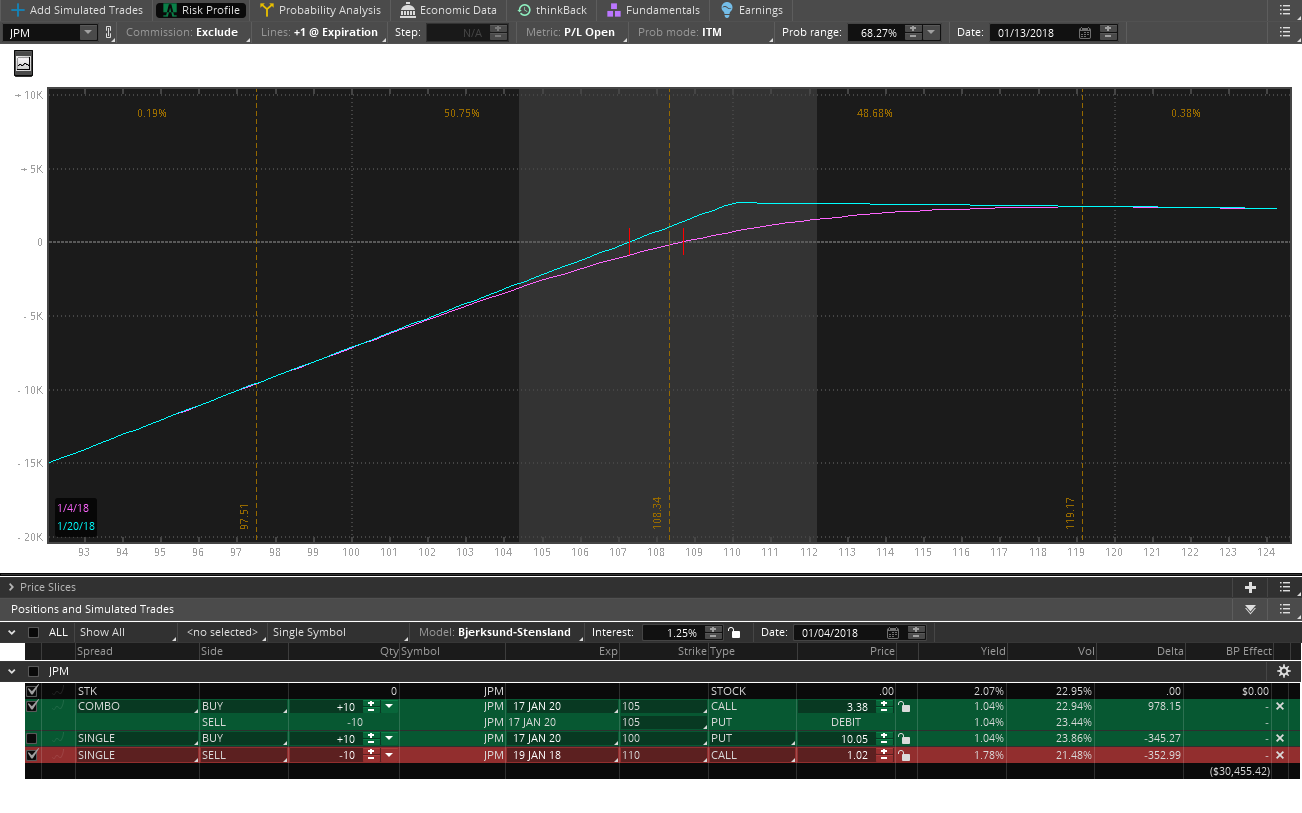

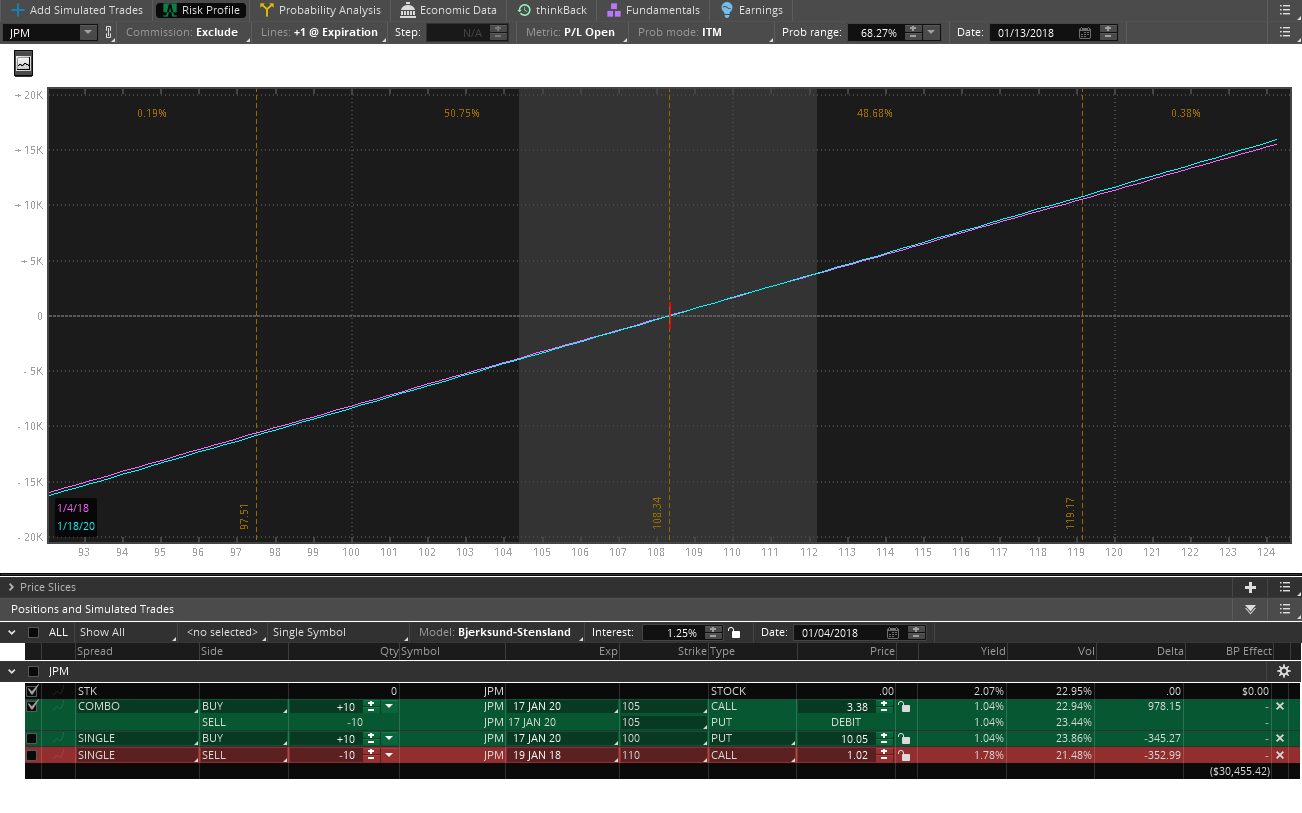

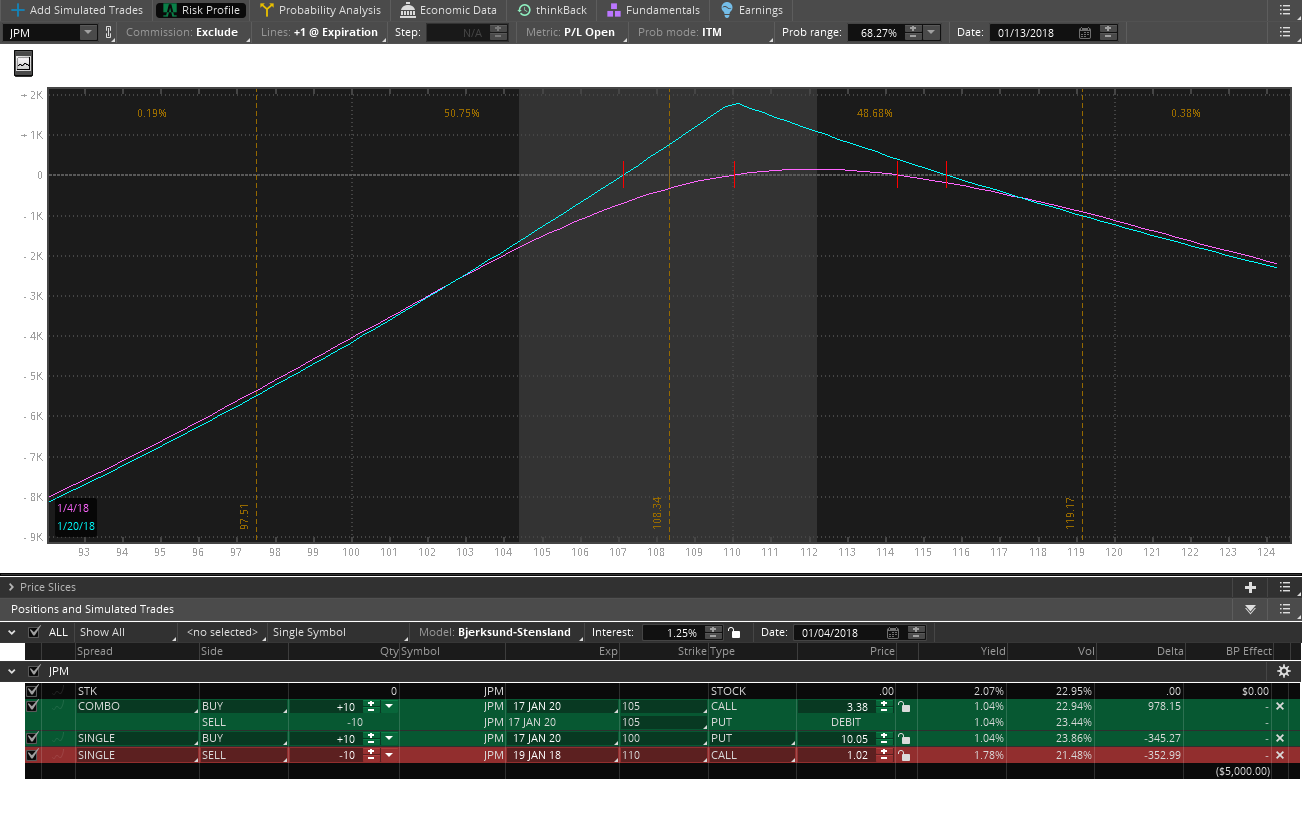

#supercharger. Works better than credit spreads for really small accounts. I have learned how to adjust from @jeffcp66 and from the options for edge book, but because of my schedule I can’t always make the adjustment in time before they go ITM or breach the short strike. By then you are already controlling losses not making money. They expire for full profit most of the time because you set then up deep ITM, if assigned on the short strike easy to exercise your long, and very easy to convert to a #fuzzy or calendar leap if they explode. Then fairly easy to work back to even or profit.

#spycraft will be rolling some of these out on the mid size accounts again but found that the ones that were farther out in time were easier to manage. So these will be 21-45 DTE in the future, mostly using spy but some qqq, iwm and maybe even dia. 3-5 points between strikes so I can manage by buying in between the strikes when needed and will not let them go to expiration, will close at 50% profit or any profit that is decent.

CC straddles or strangles if have just taken assignment on a short put and at a support area.

CC return more on a cash basis than puts so with my #pietrades will be selling puts a lot closer to the money with the hopes of getting assigned so I can immediately flip to CC.

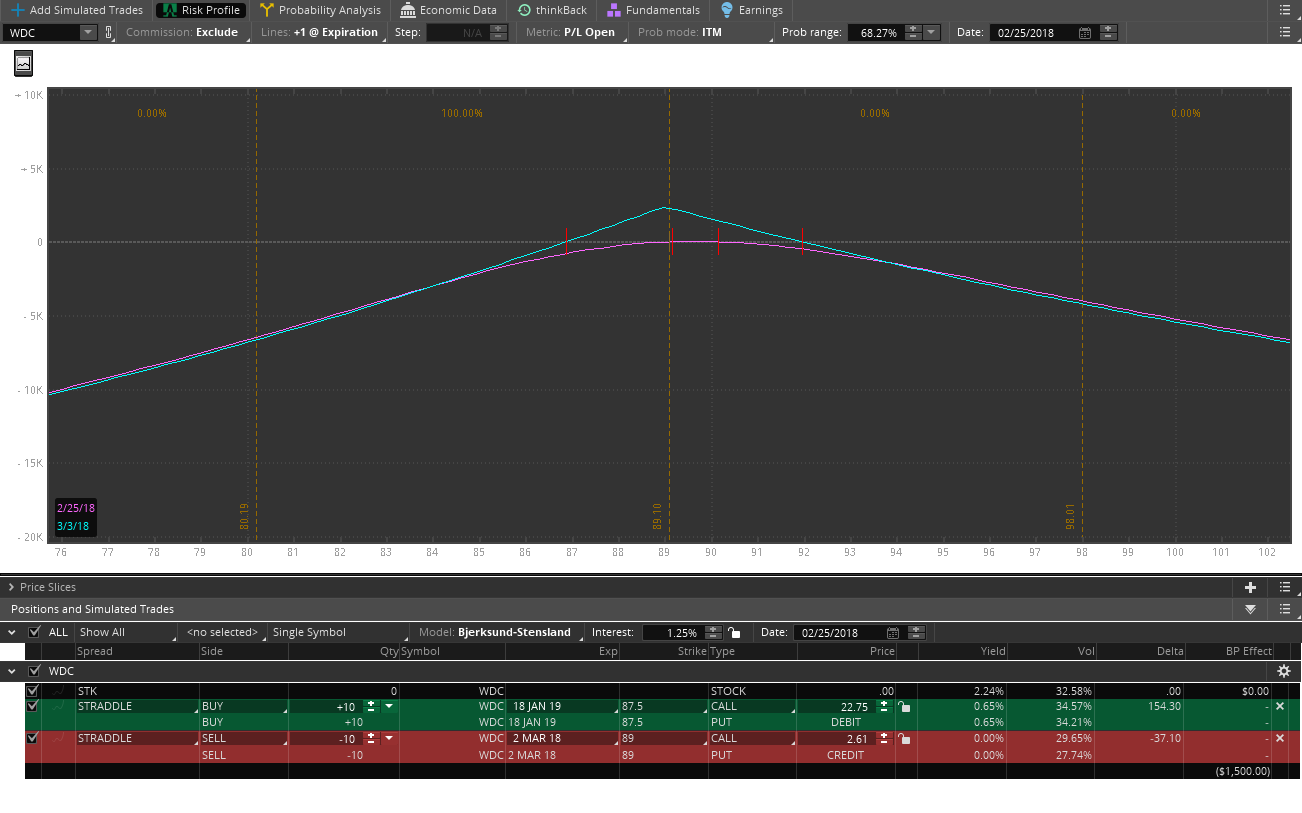

#fuzzies are a great way to convert losing trades into break even or winners.

The higher the premiums the easier it is to roll. So I am looking at the history of how often the move is exceeding the expected move. GM is a good example, expected move exceeded almost weekly but the premiums were crap so I have been rolling it for 15 weeks now. The higher premium names even when exceeded were usually back to break even in 2 weeks. Less work + more money = more free and fun time!

Never being short unhedged volatility again!!!

Sticking with those tactics and keeping it simple and profitable until the market changes and these no longer work and have to adjust again, but I think these are tactics that can work in any market condition.

With that said, bunch of rolls today and was assigned early on a few.

ERX #supercharger 20/25 assigned for full profit. Put on 21 days ago for 4.55 debit closed at 5 credit

EXPE 104 put expiring worthless :). That account will open #spycraft on Monday.

Smallest account AAPL 145/150 ITM call debit spread. 3 contracts max gain $207 for $1293 at risk. That is a 16% ROI if AAPL anywhere above 150 or 206% annualized. I will be doing a A LOT more of these going forward on the smaller accounts now that I have seen how they work for 8 weeks and even adjusted 2 to #fuzzies.

FAS 65 CC in 3 different accounts. Rolled for 1.14, 1.1, 1.15 credits and cost basis now 57.92, 55.74, 61.33 with FAS at 64.03.

Hope everyone has a good expiration and great weekend!