#earnings #longputspread #hedge DIS

Bought a 105/100 May 15 put spread for 1.99 against a rolled June 19, 100/110 short put spread, DIS is around 104.

Thanks for the data Jeff.

#earnings #longputspread #hedge DIS

Bought a 105/100 May 15 put spread for 1.99 against a rolled June 19, 100/110 short put spread, DIS is around 104.

Thanks for the data Jeff.

/ES/SPX/SPY #hedge

Closed out the /ES 2690/2700 back ratio for 300 or a $3025 loss. Just means the market did not crash.

So I have been trying to figure out a cheaper way to do these but still get the 10% coverage for a 10% down move. I came up with a modified risk twist/unbalanced butterfly. Cost about half as much as the back ratio.

BTO the Mar 2020 /ES 2790/2780/2770 butterfly. Ratio is one 2790 sold, bought three 2780 and sold one 2770 for $1690. About half the cost of the back ratio. Still good coverage and could always tweak the ratio if the market really starts to move. So this will only cost about $6800 per year instead of 12k but the deductible stays about the same.

Here is the graph and just put his on 10 minutes ago so can probably do the same. For every 100k in the account I would do 1.

#Hedge I’m calling it a hedge, but I’m not net long or short so it’s really just a trade.

Bought to open $VIX Jan 21st 17/20 call spread for .80

#butterfly #hedge ROKU

I have a long suffering, inverted, Oct. 18, 85/105 strangle that is approaching break even with ROKU dropping below 105 after rocketing to the moon. I sold a 97/99/99/100 put butterfly for .34 for a little upside protection.

#optionsexpiration and actually these are for next week, I rolled everything today.

Sorry I have not had time to post for anyone that was following trades. I will do a better job of at least a weekly update. That is how I trade. 95% of my trades are on Thurs. so a weekly update should keep things up to date.

Lots of trading last few weeks but equity curve flat. Need the trade tariff BS to end. Not good for business 😦

Most of my trades have been converted to #fuzzy or #lizardpies for recovery.

#hedge

/ES 62 DTE 2610/2605 back ratio has made a few $. It’s real purpose is to guard against a 2/6/18 or 8/24/15 event. Hope I don’t need it but would get a lot of cash then. However like an insurance policy I expect to lose on this.

#pietrades

LABU 45 cc at 44.25 cb and 40 cc at 37.13 and another batch of 40 cc at 38.42

TNA 60 cc at 59.69

TQQQ 63 cc at 62.15

AMAT 22 DTE 42 CC at 41.04. Assigned off a 43 put but had some credits as a cushion

#fuzzy

EOG 92.5/90 rolled down to 87.5/87.5 for a little debit. Cost basis 15.44 but because I had made some on the longs it put some cash back in the account.

GILD 65/65 rolled next week for 0.29 credit. Cost basis 5.91. Should not be too much longer for a free trade.

LNG 67.5/67.5 rolled for 0.34 credit. Cost basis 9.99 down from 15.57 at onset only 4 weeks ago.

XBI 80/80/85 rolled for 0.70 and cb 5.57

XBI 80/85 cb 12.50. This is a new batch we are doing live as an experiment. Avg. about 4% cost reduction per week. With monthlies it is larger about 6-8% but the theta decay is slower. 6% per month is 96% per year.

GILD 65/65 rolled for 0.28 for cb of 3.78. Freebie soon I hope 🙂 but this is also an experiment that will be taken all the way to expiration in 2021.

GILD 65/65 rolled for 0.28 at 6.45. Same as above but this is tracking the compounded addition of contracts as the rolls spit off cash.

#lizardpies

IBB 103.5 rolled down to 102/102/102.5 for total credit of 0.84. This has been recovered all the way from 107/109 strikes. Shows the flexibility of the #jadelizard as a tactic for adjustments.

IWM rolled down from 150 to 149/149/149.5. Reduced debit from 2.11 to 1.63 as I have recovered this from 155/157 strikes. I gave back a little credit to reduce margin.

SQ 63.5/63.5/64 rolled for total credit of 2.19. Looks like it found a bottom.

XBI 81.5 rolled down to 81/81/81.5 for total credit of 2.35.

LNG 64/64/64.5 rolled down from 66 for 1.68 total credit.

Once I can close a few of these, hopefully next week, will start some 21 DTE #lizardpies and create ladders. Some of them will be skewed to downside to just have steady income with every expiration and let them expire each week. Add new ones every Monday or Thurs.

Stay nimble, I suspect there is more volatility ahead but take advantage of the increased premiums 🙂

Here is an example of a 22 DTE #lizardpies I am looking at.

7 points of downside protection. No risk to upside. Income over 3 weeks, can probably close early for 50% or more profit.

#hedge LULU

In addition to the May strangle I sold today, I have had an April 18, 130/135 short ratio put spread (2 short 130s, 1 long 135) trade put on March 1. LULU has been up and down, trade hasn’t been profitable. I bought a March 29, 120/130 put spread for 1.33. If LULU drops big I have some insurance, will be OK on a big rise, the short 130s will cover the hedge.

BTO Apr 15 284/282 Bear Put spread .78 #hedge From TastyTrade

BTO Mar 22 154/152 Puts $.75 #hedge

Wish I had kept my SPX hedges on. A $3 put that I had on at 2550 is now trading for $21.40-22.

Most months you never need it. Last few weeks it is almost a mega millions or power ball ticket.

Once we settle down I will always keep one of these on. Either long puts, ratio, or risk twist for times like this. Then you have a pile of cash you can deploy when the market tanks.

#Hedge – I didn’t think this would pay until the election. It may do better but I’m booking it while it’s nice and green.

Sold 10 VIX Nov 11/13/17/21 double verticals @ .56 (bought for .10)

Actually left the long 11’s on for maybe a drop…

#Hedge – Added the second half of this today. First half filled at .05 debit and second half filled at .10 credit. Also added long 11 puts underneath the short 13’s. Basically a bullish (on VIX) double vertical…sold 13/11 put spreads to finance the purchase of 17/21 call spreads. This will also be a nice hedge for shorting UVXY after the upcoming reverse split.

Here’s the original post:

=======================================================================

Theo Trade VIX hedge

#Hedge – From a free webinar last night….Don was going out to Nov and selling 13 strike puts. Using that cash to finance the purchase of 17/21 Bull Call Spreads. He was getting it at even. I’m showing a nickel debit right now. No fill yet.

=======================================================================

#Hedge – From a free webinar last night….Don was going out to Nov and selling 13 strike puts. Using that cash to finance the purchase of 17/21 Bull Call Spreads. He was getting it at even. I’m showing a nickel debit right now. No fill yet.

On vacation this week but home so still doing some trading.

Let’s get the crap out of the way first. Sorry to anyone who followed AMAT. Loss on the last earnings 12 weeks ago. Almost worked it back to even but they beat last week but still punished so break even or near break even is now a loss again. I mostly had these in small accounts so am closing so I can use the money on something more effective. BTC all the 47 call options for pennies, 0.03. Sold the stock at 43.06 and 43.09. Total losses (not per contract) of $588 on lot 1 and $558 on lot 2. Not bad considering it was down over $2000 initially. Rolling helps but the reason I am closing it is this: as it dropped below $50 the premiums dried up. ATM 1 week out is only 0.4-0.5. Not enough for #pietrades. Second reason is after 14 weeks of not being able to break even, time to move on. Like GM this is off the #pietrade list for a while. If you can’t bring in more than 0.5-1% per week, not worth #pietrade.

STC the SPX 2550 calendar hedge for 0.55. So a 1 month hedge only cost 0.65. I will continue playing with these but doubt I will always have a hedge. Maybe easier to just short some /ES futures when needed.

Rest are updates, rolls, new trades.

#fuzzies

MU LEAP 55/50 8 DTE cb at 11.26. At least MU found a base.

WDC LEAP 60/ 65 29 DTE cb at 17.78. Looks like finding new range in the 60-70 area.

EOG LEAP 115/115 29 DTE cb at 11.2.

XBI LEAP 87/95 and 95/95 rolled out to 22 DTE for 0.72 credit. cb now 6.8 and 3.32. Should be free trades soon.

#pietrades

LABU 8 DTE 85 put for 1.9, cb 83.10 if assigned. Good support at 85.

TQQQ lot 1 65 cc rolled to next week 65.5 cc for 0.20 credit. Cb 62.78

TQQQ lot 2 65 CC cb 63.23, new trade, small account only 1-2 contracts

TQQQ lot 3 65 cc rolled to next week 65.5 for 0.25 credit. Cb now 62.98

TQQQ lot 4 66 CC cb 65.02 new trade.

TQQQ lot 5 65 cc cb 63.90

Looks like a lot of TQQQ but each account only 1-2 contracts, I am diversified elsewhere. However I have noticed that my more concentrated accounts are doing much better. Better to be a specialist than a general practitioner like me, at least for trading. Also have noticed the more you get direction right, the better the non directional trades do better. Will keep working on being better at directional bias.

A few other changes. No more #pietrades on earnings. Last 5 out of 8 went bad and basically flattened my equity curve for the last 4 months. Would have done much better without those. If I do them will use spreads in advance. Without those 5 losing earnings trades I could have paid off my wife’s car.

Converting deep ITM #pietrades into #fuzzy is a very effective risk reduction tool. Allows you to limit margin but also keep selling premium weekly and looking at 100% returns over 6 months if I keep them going. Probably best tactic for small accounts.

I will be moving most of the #pietrades over to ETFs and leveraged products to avoid the single ticker risk. The ladder idea works well for this 45 DTE and closing/rolling after 3 weeks.

#pietrades and #optionsexpiration

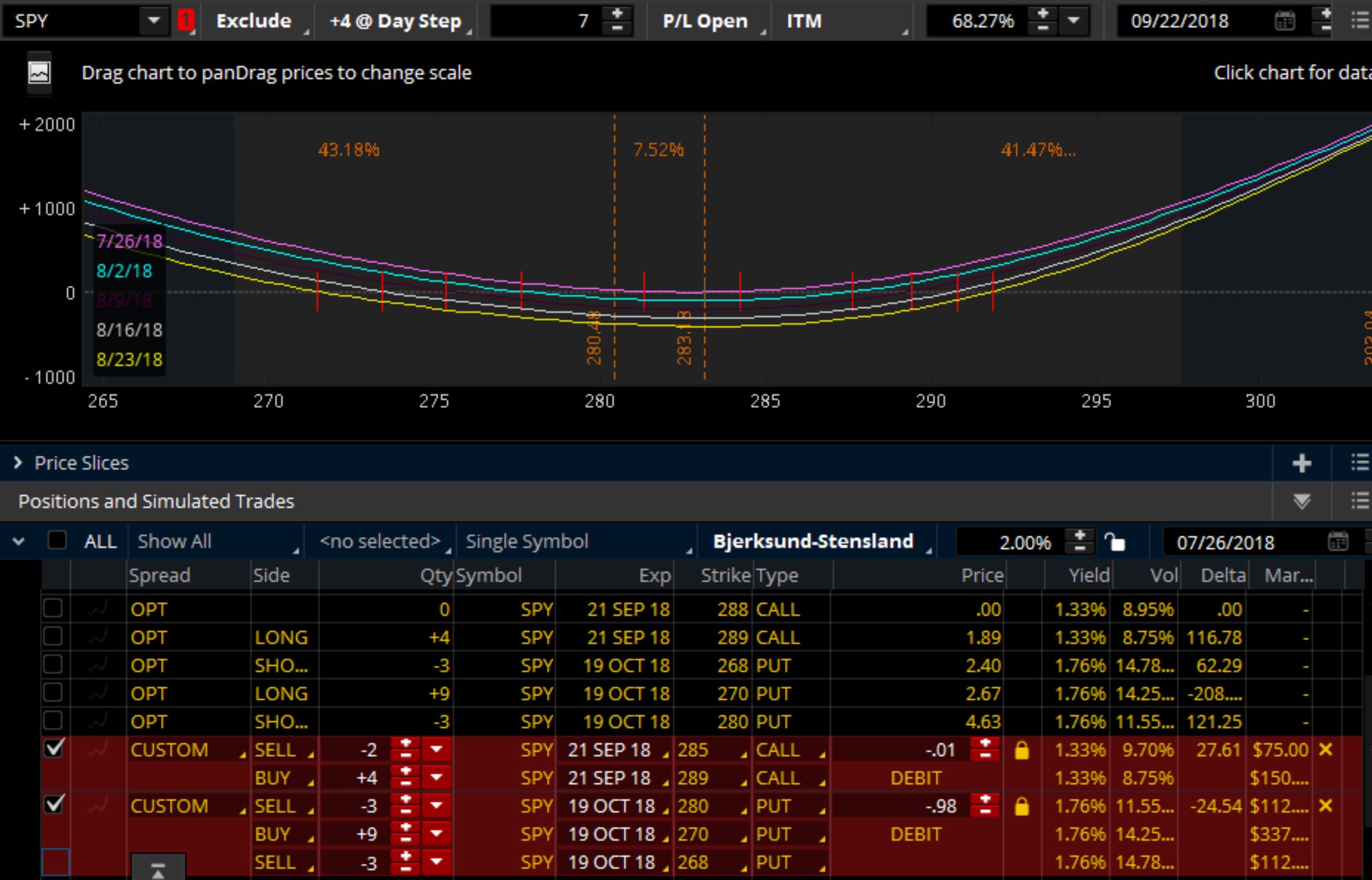

Fragmented trading day here. They were working on lines near our house and internet kept going in and out which will explain my weird WDC trade.

WDC, keeps going down. Converted to LEAP #fuzzy earlier in week. Was trying to roll to next week at 70 but because of the internet issues it somehow rolled to 66. Ok so took in a lot of cash but then the internet went down for a few hours. Of course during that time WDC reversed so was losing $ on the new trade and deltas were already flat. So rolled out to 43 DTE and up to 70. Took in 1.32 on the 66 call but had to buy them back and roll for 1.02 debit. So anyway after all that, now have the 60 LEAP 70 43 DTE call spread for cost basis of 19.03. If we rebound will buy back 2-3 of the short calls to let it run. Break below 65 will collar it to prevent further losses. As long as it stays 65-70 should break even in about 6-8 weeks.

MU 55/54 diagonal looking ok. Cb 12.43.

EOG 43 DTE 115 put cost basis at 113.20.

TQQQ batch 1 will assign tomorrow at 60 for a 2.21 gain on each contract. Reset Monday, hopefully after at least a little pull back.

TQQQ batch 2 will assign at 59 for 1.75 gain per each contract. Both these are nice 2 week pay checks! Reset Monday.

AMAT batch 1. Rolled 47 cc out a week for 0.52 credit. Cb now 49.24. A few more weeks of rolling then will reset as #pietrade again.

AMAT batch 2 rolled 47 cc out a week for 0.5 credit. This is showing a profit of 0.81 per contract but may keep rolling if it stays in range.

XBI 87/96.5 and 95/96 #fuzzy. Waiting for more decay and will roll next week. Cost basis of 8.62 on first batch and 5.1 on second.

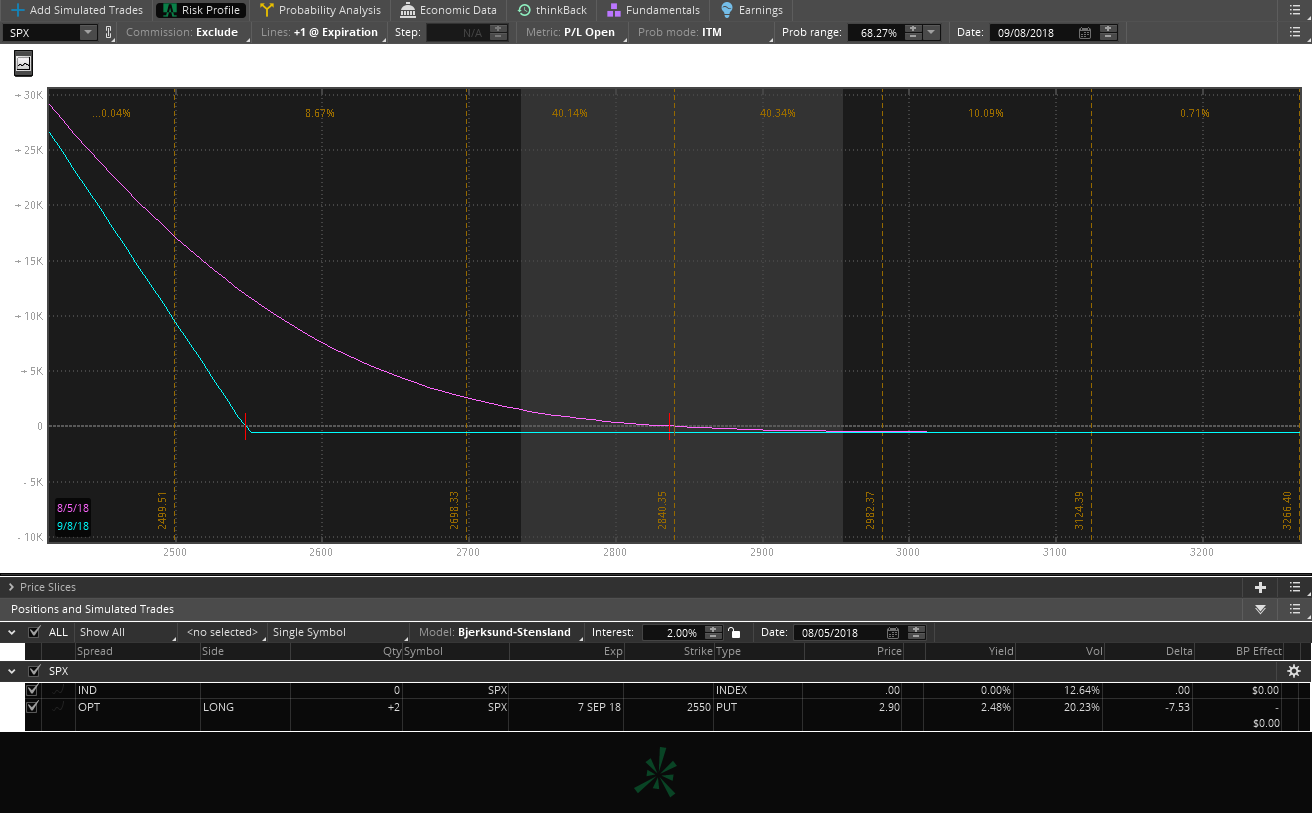

SPX #hedge 2550 put has lost a lot already but gained 0.15 late in the day. Currently 1.75, bought for 2.9. Hope I don’t need it but will roll it at least a week before it expires and change it to a back ratio or risk twist to limit costs. That will be a more efficient hedge.

Hope everyone is having a good week and expiration. Some new trades will be added Monday.

Thanks for all the ideas below. I gave this some thought while mowing the lawn, push mower, ear plugs in, so I tend to think trading issues over while I am doing it and have about 1.25 hours to do that every week because it keeps raining and my grass keeps growing. Most years it is brown by now and I take a few weeks off mowing. Some of my best ideas have popped in my head while mowing but also some of my dumbest (no you really shouldn’t build a mini plane using a lawnmower engine, well you can but does not make it a smart idea and you would likely end up making a flaming hole in the ground).

So here are the best options I can figure out.

1. Straight SPX/SPY put purchase. Most months will lose almost all of it. Have to adjust as the market moves. If your hedge was set up at 2700 and the SPX is now 2800 your hedge will not cover as well as it did when you put it on. Maybe 1-2 times a year pays out decently, once every 15 months is a lottery ticket. Can sell other options to pay for it but bottom line is you are buying insurance and we all know how that usually works out. Can roll it to at least recover a little of the premium you paid. This is what I put on Friday.

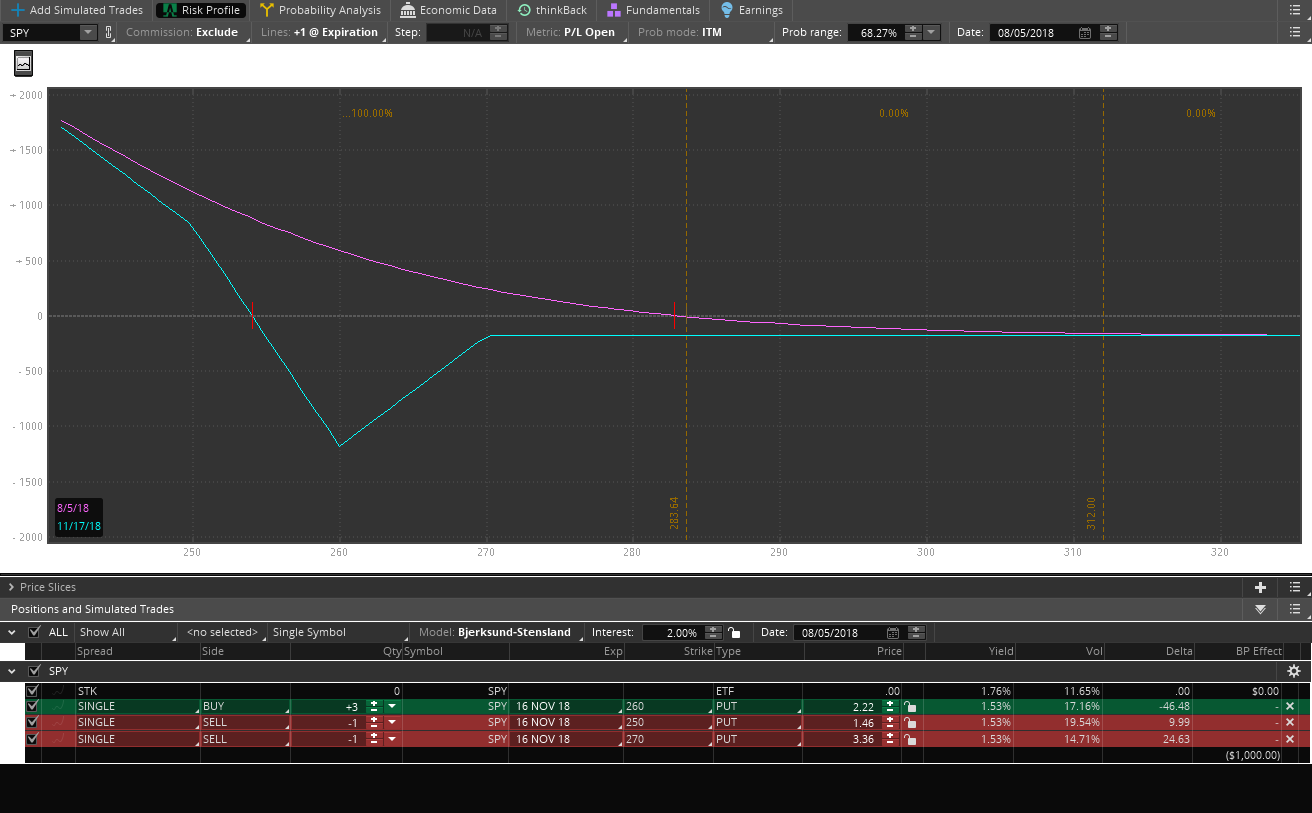

2. Risk twist. Cheaper than above good downside protection but leaves a gap at expiration where max loss can still occur. Same issue as above, needs to be adjusted as the market moves but starting 90 DTE gives you more time and less expensive even if doing 4 times a year. I suspect the payouts are about the same as straight puts since you are long puts on a ratio. Switched to SPY for example. 3 long, 2 short ratio with a 10 point spread. Similar to a back ratio or a modified butterfly.

3. Credit spread on SPY or SPX or /ES but you have to act quickly on adjusting. Say you sold the SPX delta 16 put and then bought an option 10 points below. For example sell 10 the 2600 and buy the 2590. If the delta on the short makes it to a delta 30 you would buy 3-5 of 2595 puts to effectively create a back ratio. No graph, we have discussed this as an adjustment in the #spycraft discussion. The only issue with this is you have to act quickly sometimes and occasionally the move is in the middle of the night like on 8/24/2015. The /ES was down 300 points when I woke up and any adjustment then was limiting losses, not making more $. At that point it was going to be painful no matter what I did. I suppose if you traded /ES you could adjust it in the middle of the night or even SPY and SPX now. The big advantage here is you take in a credit when you put the trade on so buying options could be taken out of the credit. On a big move buying extra options will cost more though. Likely would only have to adjust 2 times a year and you could also ladder and start 45 DTE to make the most of theta decay until the move happens. You also need to leave enough room between the strikes so that you can buy in between. The others are set and forget for a while, this one would need checking every day like any sold option. Most of us here do that anyway.

4. Front spread/back spread or back ratio depending on your vocabulary or possibly a #rocketmanhedge here?

On SPY assuming a 10% correction which I did with all of these, you sell one 265 put and buy two 260 puts for $175 debit. The debit on the risk twist above would be $219 for a similar looking graph. Also keep in the mind the straight put purchase is for 30 DTE, the risk twist and the back ratio are set up for 90 days and the credit spread at 45 DTE. So there are some timing differences and the time component would need to be managed on all of them. Front spread is buy one sell 2 so really would not help in this case, unless it was a call spread and set up for a credit. Then in a correction you would keep the credit.

So the winner is? Up to you. I suppose it depends on what you want. Lottery ticket go with straight puts but most months like a lottery ticket you will lose your money. The risk twist and the back ratio decrease the cost but still need a really big move to pay off. Advantage is you can get another 2 months out of them for a cheaper cost than the monthlies but in either case as the market moves would need to be adjusted. A 10% correction from 2800 is going to be a lot different strikes than a 10% correction from 2600 on SPX.

Finally we have the credit spread converted to a back ratio. Paid up front, theta helps you, but on those 5 standard deviation moves might not have time to pull the trigger at the right moment. But at least you are then risk defined and can probably roll until the market settles down. I was able to do that with a few of my accounts on 8/24/15 and actually broke even after about 3-4 weeks. Still there was a lot of red on the screen until then. Also the markets became really wide and it was hard to get decent fills. TS and TOS did ok with it, optionsxpress and fidelity not so much and is why I do not have accounts there anymore.

My personal vote is probably the back ratio or a credit spread adjusted to a back ratio early. Cheaper than a straight put purchase, longer acting, but still pays out the lottery ticket when needed and simpler than a risk/twist, less moving parts.

Floor open for discussion. Anyone have any other or better ideas please let me know 🙂

I am at the point in my trading career and my accounts are big enough a few of them need insurance most of the time. I plan to do these going forward and will report on what is the best cost/benefit ratio.

Still raining here and the VIX is down to 11.82. Cheapest time to put on a portfolio hedge. I fully expect these to expire and lose all my $ but 1-2 times a year it may be a lottery ticket! This is based on the recommendation from option income masters (a subset of OIB). They hedge the entire portfolio almost monthly, after a big drop they cash out and put the money back in at the bottom. They finance the hedges by selling other options.

I am only hedging my core account, everything else already spreads or cash hedged so BTO 2 SPX 2550 puts 35 DTE. In a 10% correction these should be worth 11-12k which would offset the losses on the account in a 10% correction and then could close for cash to redeploy.

Hope I don’t need it but will see how it works.

#Hedge – With the hedge subject being discussed here’s what I did based on last nights Theo Trade free update video. Playing SPY both ways for minimal cost but still very nice protection. He says max risk is what you paid for the position but it looks like there are small pockets of slightly greater risk if held all the way to expiration. I’m not 100 percent sure I’ve got the risk graph configured properly. I also moved the strikes up a little from the video.

#Hedge

BTO Aug 22 15/19 BuCS & 13/10 BuPS cost .09

This is a DK trade

STO Jul 18 13/11 & BTO Jul 18 18/23 calls 13 Cr

#Hedge DK Trade

#SyntheticStock – Core is out in Jan 2020…

Bought to Close XOM MAR 9 2018 76.0 Calls @ .03 (sold for .54)

Sold XOM MAR 16 2018 75.5 Calls @ .36

rolled my march 9 48 call #hedge into march 23 50 call for 3 cent credit

#syntheticstock

BTO 21 SEP 18 46/46/44 CALL/PUT/PUT 5.97 with stock at 45.98. Need 0.28 per week to cover so STO 9 MAR 48 CALL 0.67 #syntheticstock

Rolled #Hedge Mar 2 77 to Mar 9 81 1.01 Debit More room to move

Rolled Feb 23 79 Call to Mar 2 77 .25 #Hedge

STO CC #Hedge Mar 2 97.5 Call .15

STO UPS Mar 29 111/113 Calls .32 2x #atomicfuzzy #Hedge

Rolled UPS Feb 23 111 Call to Mar 2 109 .48

Rolled XLV Feb 23 87.5 Call to mar 2 87 .25

#Hedge for additional credits

Rolled Feb 16 45.5 to Feb 23 .23 #Hedge

Rolled Feb 16 274 Calls to Feb 23 276.5 .24 Cr #Hedge

SPY Rolled #Hedge Feb 14 274 to Feb 16 274 .13

SPY STO Feb 14 274 Call @ .18 #Hedge

Rolled Feb 16 167.5 Call to Feb 23 @ .63 #Hedge Roll

BTC Feb 9 63 .03 Close #Hedge Sold 1-24 $ .46

STO DFeb 9 63 .15 #Hedge

STO #Hedge Feb 9 64 .15

Rolled Feb 2 45 to Feb 9 .30 #Hedge

#Fuzzy – BTC MU Jan26’18 45 calls for 0.02, sold last week for 0.30. My core position is MU Apr’18 45/45/40, paid 0.87. So far have booked 0.85 in premium since opened on 1/02/18. Earnings are March 20. I’m going to leave this unhedged for now, seems like it’s been headed down the runway a bit, hopefully takeoff will be soon??

STO Feb 2 61 .42 #hedge

STO Feb 16 43.50 .46 #hedge Net Debit .20

Thx

Smasty

STO IP Feb 2 67 .30 #Hedge

STO MYGN Feb 45 .70 #Hedge

Rolled IWM #Hedge Jan 29 160 Call to Feb 2 .31 reduced cost debit

Pretty quiet trading day for me, thanks again for everyone’s good ideas:

1. Took the HD BePS profit I was expecting this morning (Bought 1.09, sold 1.59)

2. Bought PIR long calls for Earnings run up (closes 1 day before earnings), target 40%

3. SHAK BePS for retracement from extreme up move, .84 debit, target 50%, trade is green

4. BA BePS for retracement from extreme up move, 1.21 debit, 50% target, trade is red

5. ADSK #ShortPuts for Mar, thank you for the idea @jsd501

6. I’m keeping 2 short /ES contracts hedged with short puts, rolled short puts to next week for additional credit. This “Z” contract will run out pretty soon.

7. CVX closed BuCS for 50% loss (I’m testing using “probability of touch” as a stop on debit trades)

8. RCII There was an almost 10,000 contract opening call sale today for Jan 13 calls, so I bought a BePS Jan 13/11 for 1.14 (paid less than intrinsic). Following the “smart money” fund flow on this (I realize this may be Trader setting a hedge vs a spec trade, but it’s limited risk)

9. New NDX #Bitty Dec 29 6125/6120 for .85 cr, 50% target

Active Greens: ADSK, AFL, AMC, BBY, ETFC,FB, LRCX, MNST, MSFT,NDX,NTNX,ORCL, SHAK, TTWO,

Active Reds: AAPL, ALGN, DLTR, JPM, LMT, NUE, PIR, QQQ, SPY, ULTA, /ES, BA (net green)

3% return on capital today

I’m not much of a regular old butterfly guy (other than iron butterflies for earnings) so maybe I did something wrong. The SVXY put butterfly that @vxxkelly and I were discussing as a #Hedge didn’t do much during the selloff Friday. I monitored it as SVXY dropped all the way down and then all the way back up and the thing was never profitable at all. Was it because it was out in Jan? Do these types of trades only work on much shorter time frames? Did I (quite possibly) screw something up?

Here was the trade:

SVXY JAN 19 2018 110.0/105.0/97.5 Put Butterfly @ .22 credit

Bought 5 110 puts

Sold 10 105 puts

Bought 5 97.5 puts

#SyntheticShort #Hedge #RocketManHedge – A little hedge out through the beginning of the year…

Synthetic short stock with a protective call. 45.00 debit with max loss of 50.00:

Sold SPX JAN 19 2018 2570.0 Call @ 41.50

Bought SPX JAN 19 2018 2570.0 Put @ 48.00

Bought SPX JAN 19 2018 2575.0 Call @ 38.50

Need to collect 4.15 per week to cover the max loss so:

Sold SPX NOV 3 2017 2530.0 Put @ 5.90

This gives 40 to 50 points of downside protection for minimal (or no) cost…

FB #Hedge

I often hedge earnings trades by going out further which sometimes defeats the purpose but in the event the real job gets in the way I have time to make yet another bad decision. Instead I bought a Nov. 4 123/137 straddle for 1.67. It may offer some protection along with a roll in case of a blow out either direction.