Thanks for all the ideas below. I gave this some thought while mowing the lawn, push mower, ear plugs in, so I tend to think trading issues over while I am doing it and have about 1.25 hours to do that every week because it keeps raining and my grass keeps growing. Most years it is brown by now and I take a few weeks off mowing. Some of my best ideas have popped in my head while mowing but also some of my dumbest (no you really shouldn’t build a mini plane using a lawnmower engine, well you can but does not make it a smart idea and you would likely end up making a flaming hole in the ground).

So here are the best options I can figure out.

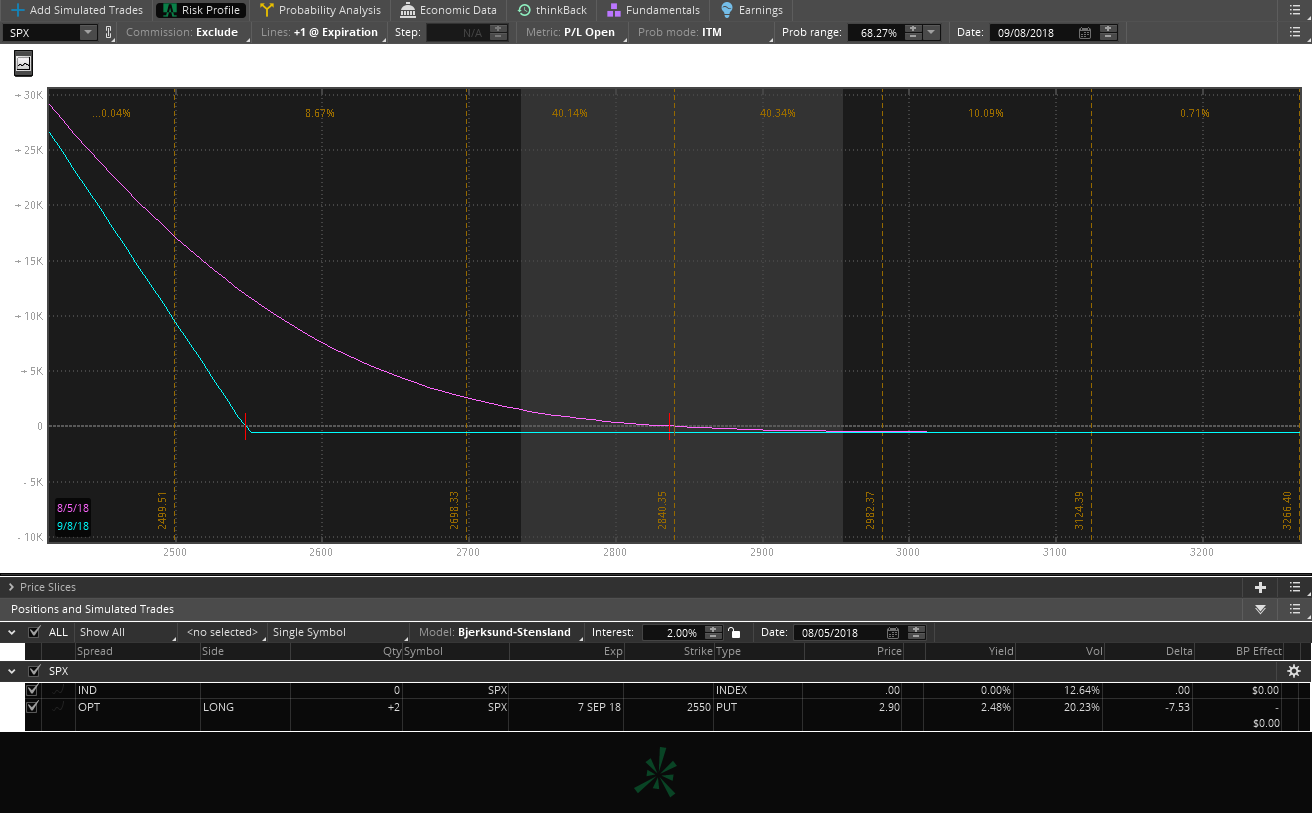

1. Straight SPX/SPY put purchase. Most months will lose almost all of it. Have to adjust as the market moves. If your hedge was set up at 2700 and the SPX is now 2800 your hedge will not cover as well as it did when you put it on. Maybe 1-2 times a year pays out decently, once every 15 months is a lottery ticket. Can sell other options to pay for it but bottom line is you are buying insurance and we all know how that usually works out. Can roll it to at least recover a little of the premium you paid. This is what I put on Friday.

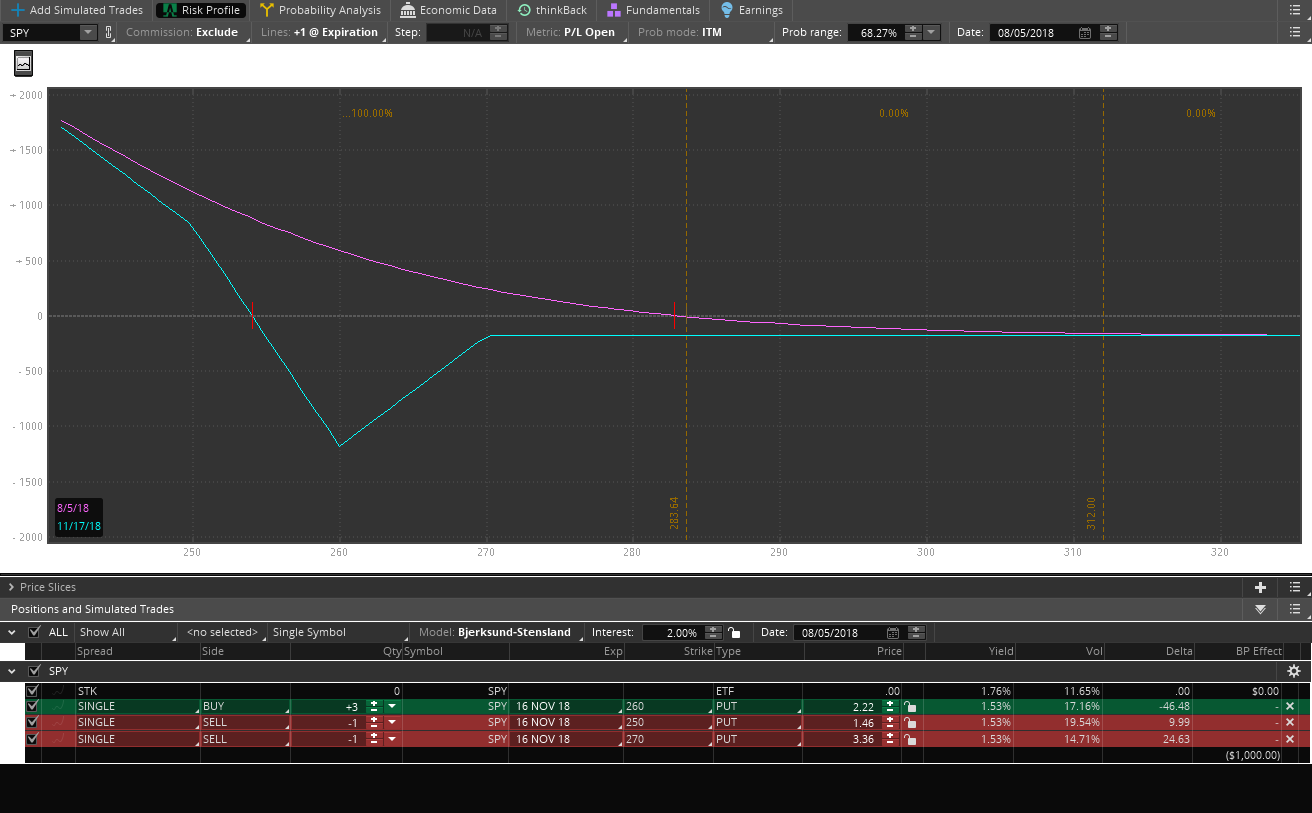

2. Risk twist. Cheaper than above good downside protection but leaves a gap at expiration where max loss can still occur. Same issue as above, needs to be adjusted as the market moves but starting 90 DTE gives you more time and less expensive even if doing 4 times a year. I suspect the payouts are about the same as straight puts since you are long puts on a ratio. Switched to SPY for example. 3 long, 2 short ratio with a 10 point spread. Similar to a back ratio or a modified butterfly.

3. Credit spread on SPY or SPX or /ES but you have to act quickly on adjusting. Say you sold the SPX delta 16 put and then bought an option 10 points below. For example sell 10 the 2600 and buy the 2590. If the delta on the short makes it to a delta 30 you would buy 3-5 of 2595 puts to effectively create a back ratio. No graph, we have discussed this as an adjustment in the #spycraft discussion. The only issue with this is you have to act quickly sometimes and occasionally the move is in the middle of the night like on 8/24/2015. The /ES was down 300 points when I woke up and any adjustment then was limiting losses, not making more $. At that point it was going to be painful no matter what I did. I suppose if you traded /ES you could adjust it in the middle of the night or even SPY and SPX now. The big advantage here is you take in a credit when you put the trade on so buying options could be taken out of the credit. On a big move buying extra options will cost more though. Likely would only have to adjust 2 times a year and you could also ladder and start 45 DTE to make the most of theta decay until the move happens. You also need to leave enough room between the strikes so that you can buy in between. The others are set and forget for a while, this one would need checking every day like any sold option. Most of us here do that anyway.

4. Front spread/back spread or back ratio depending on your vocabulary or possibly a #rocketmanhedge here?

On SPY assuming a 10% correction which I did with all of these, you sell one 265 put and buy two 260 puts for $175 debit. The debit on the risk twist above would be $219 for a similar looking graph. Also keep in the mind the straight put purchase is for 30 DTE, the risk twist and the back ratio are set up for 90 days and the credit spread at 45 DTE. So there are some timing differences and the time component would need to be managed on all of them. Front spread is buy one sell 2 so really would not help in this case, unless it was a call spread and set up for a credit. Then in a correction you would keep the credit.

So the winner is? Up to you. I suppose it depends on what you want. Lottery ticket go with straight puts but most months like a lottery ticket you will lose your money. The risk twist and the back ratio decrease the cost but still need a really big move to pay off. Advantage is you can get another 2 months out of them for a cheaper cost than the monthlies but in either case as the market moves would need to be adjusted. A 10% correction from 2800 is going to be a lot different strikes than a 10% correction from 2600 on SPX.

Finally we have the credit spread converted to a back ratio. Paid up front, theta helps you, but on those 5 standard deviation moves might not have time to pull the trigger at the right moment. But at least you are then risk defined and can probably roll until the market settles down. I was able to do that with a few of my accounts on 8/24/15 and actually broke even after about 3-4 weeks. Still there was a lot of red on the screen until then. Also the markets became really wide and it was hard to get decent fills. TS and TOS did ok with it, optionsxpress and fidelity not so much and is why I do not have accounts there anymore.

My personal vote is probably the back ratio or a credit spread adjusted to a back ratio early. Cheaper than a straight put purchase, longer acting, but still pays out the lottery ticket when needed and simpler than a risk/twist, less moving parts.

Floor open for discussion. Anyone have any other or better ideas please let me know 🙂

I am at the point in my trading career and my accounts are big enough a few of them need insurance most of the time. I plan to do these going forward and will report on what is the best cost/benefit ratio.