Happy Friday Everyone!

I didn’t have a ton going, ‘cept for one big thing. That later.

IWM: #Saf-T 1000 shares called, net profit $1200. Reset 1500 @ 167.66, 14x jul 27 166 puts @ 2.10, Jun 22 168.5 calls x13 @ .70

I was squirming bad this morning with a ton of SPY shares on and no short calls against them. Luckily the market rebounded, I got some short calls for next Wednesday in the book. I can sleep at night when I know my short calls are on. I’m not kidding when I say it felt really uncomfortable not having them. I will change this strategy next quarter so that calls are always on regardless of dividends.

BA…ugly, but I’m not too concerned. Got lots of hedges on, got a put diagonal kicker, so far it’s looking like a retracement. Maybe even the handle of a cup forming.

Ok…beware when @kathycon MamaCash and I open the lab. We can stay up all night online battering trade designs about and running backtests. We are ALWAYS taking established designs, or other people’s ideas, and reworking them for the best success rates, highest profits, lowest risk.

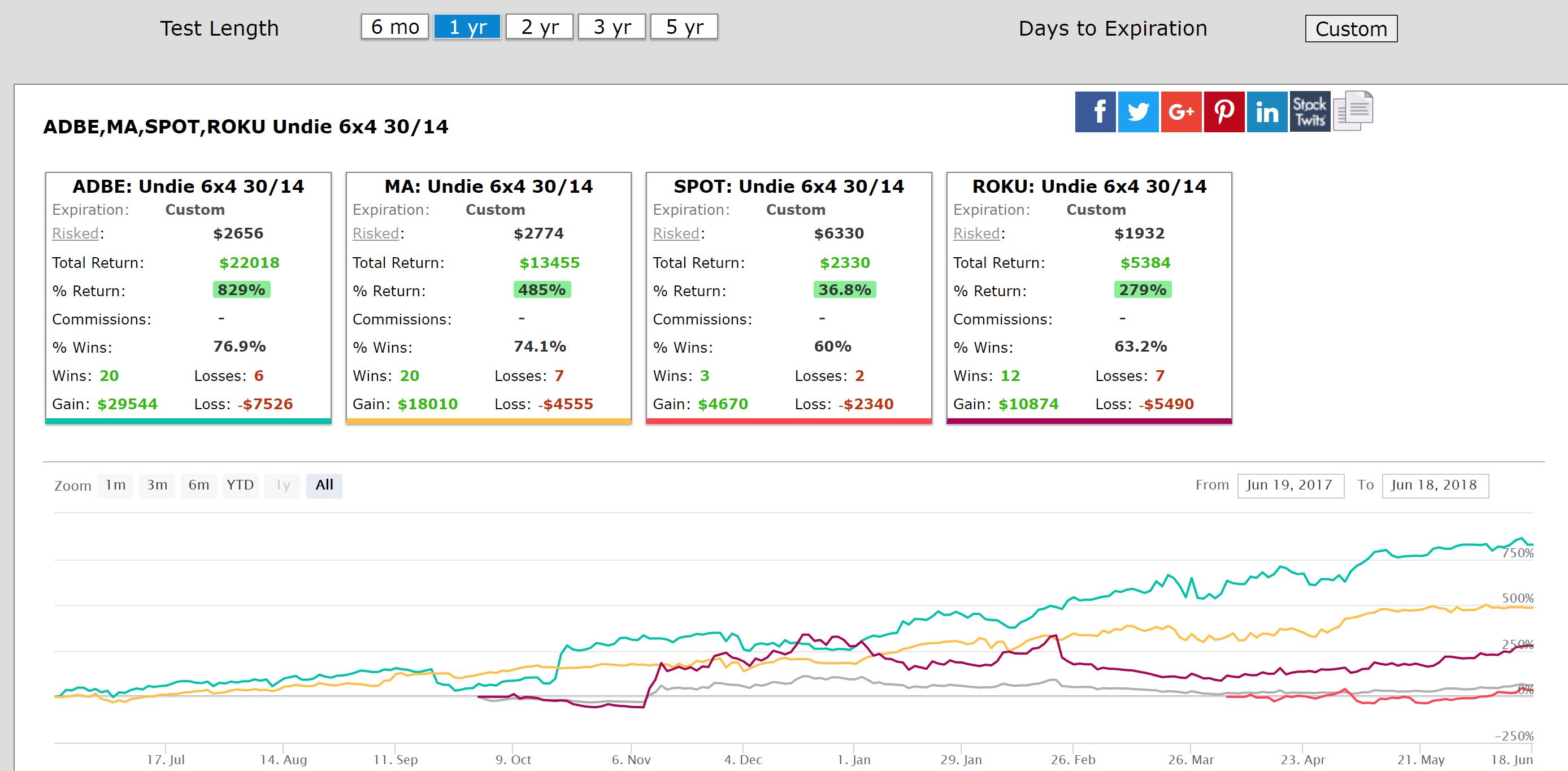

We reworked the dates and ratios on #Undies last night. I think you should let us test these out a bit. But what we discovered by backtesting is that a 30day long with a 14 day short in a .66 ratio (3×2, 6×4, 20×13) yields a much higher return on margin than using the longer dates. Because the 30-day longs are cheaper, there is less risk, which directly affects the return. These trades go on with a slight positive gamma, slight negative theta, positive vega…so kind of nice greeks on these. All of the 1-year returns we are looking at are really high, like 300% to 1200% (return on margin risk).

Consider these “petri dish” trades right now…we’ll run ’em down and report on effectiveness.

Between the two of us we have a lot of 3×2 tests on now in NVDA, ADBE, BABA, NFLX…and some others. We will report on the effectiveness of this.

Here is an example of one I have on BABA: Jul 13 202.5 call 3x @ 9.20/Jun 29 210 call 2x @ 3.40.

Everyone have a safe weekend!

Sue

p.s. premium collection this week was $14,811, 90% of what I sold. Good week!

#fundie