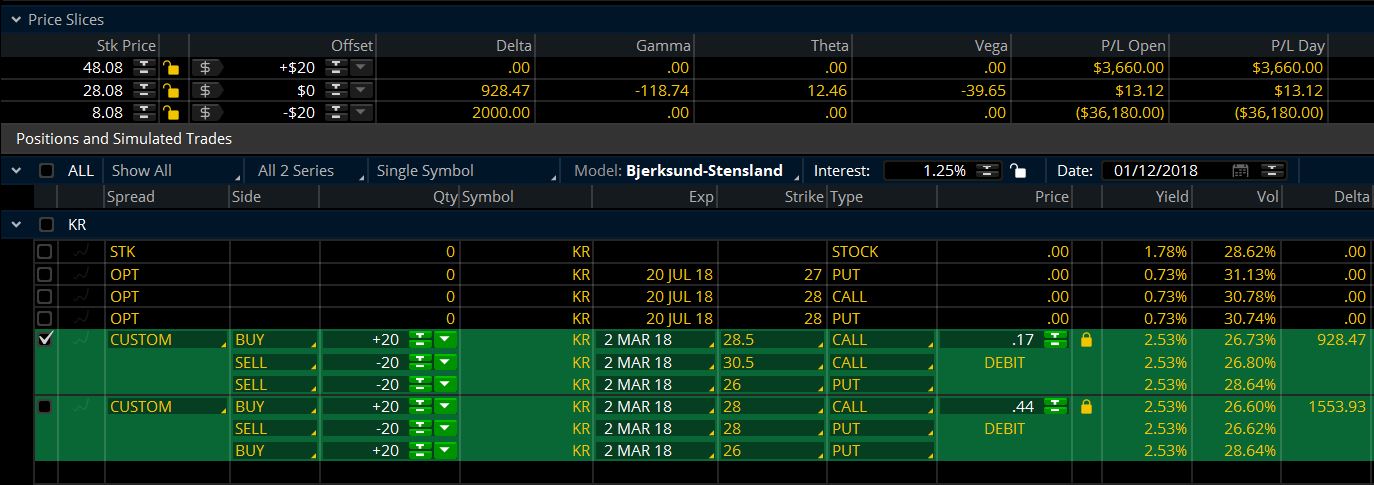

#Commissions – Doesn’t help me a whole lot but if you regularly sling more than a 10 lot it’s a big deal.

====================================================================================

Hello, tastynation!

To start off 2018 just right, we want to thank you for your show of unconditional support and irreplaceable loyalty for tastytrade and tastyworks. You are the reason we’re driving change to the financial industry. We’ve not only planned more of what you love, like more live tastytrade shows in 25 cities, more trading tools, more mind-blowing content, more new daily shows – but also stuff that will leave you thinking, “How’d they do THAT?”

tastyworks introduced zero commissions to close trades on Jan 3rd, 2017. Starting tomorrow, on Jan 2nd, 2018, tastyworks is introducing capped commissions for large option trades. This means the most commission you will pay for any single leg option trade is $10* (plus clearing fees). That’s right, just $10* per leg!

Eighteen years ago, when we built thinkorswim, 100 option contracts to open and close was $300+. At the time, we thought $1.50 per contract was cheap. Today, the industry average per contract is about $.70 plus a small ticket charge. So, 100 option contracts today is approximately $150 to open and close at most firms. With tastyworks’ new rate schedule, the same trade will cost $10 in commissions to open, zero in commissions to close and a $20 clearing fee for a total of $30. Compare that rate to any other firm on the planet and remember how good our technology and content is as well. Fees for small options trades (10 contracts or less) stay the same.

But we’re not done. As an added bonus, tastyworks will have twelve monthly drawings for funded accounts (minimum of $2,000) and each month, one customer will win free commissions for 5 years. And no, we haven’t lost our minds. We simply want to do something special and this is just the start.

On the technology side, tastyworks is releasing a new analysis tab, portfolio margin, options on futures, paper trading, an open API, a new scripting language and lots of new mobile features.

So thank you again for the incredible engagement over the past year. You have helped to make tastytrade and tastyworks one of America’s fastest growing financial innovators.

Scott / Woody & the tastyworks team

Kristi / Tom & the tastytrade team