#shortputs FEYE

Sold June 19, 12 put for .32

#shortputs FEYE

Sold June 19, 12 put for .32

BTC June 5, 50 puts at .01, that is the last of the June 5 expiration.

STO $OSTK Jun-05-2020 22.5 #CoveredCalls @0.45 credit. Basis now 19.40.

#shortputs

$OLLI BTC 6/19 80 puts at .60. STO 5/22 for 3.70

$TQQQ BTC 6/19 35 puts at .05. STO 4/15 for 2.35 Thank you @jsd501

$WORK BTC 6/19 80 puts at .50. STO 5/11 for 2.78

$AXSM BTC 6/19 92.50 puts at 19.11. STO 5/11 for 8.00. Ouch!

$TQQQ STO 9/18 35 put at 1.50 Thank you @jsd501

#coveredcalls

$RAD STO 6/5 14 calls at .28

BTC June 5, 45 puts at .01, Now waiting to get filled on the $50 puts.

#shortputs

$MRVL BTC 6/19 25 put for .05. STO at 1.30 on 5/8

#coveredcalls

$ROKU STO 6/5 113 calla at 2.40

#coveredcalls VSTO

Bought 100 shares @ 10.75, sold June 19, 10 call for 1.65, 9.10 debit

#SPX7dteLong Bought to Open $SPX June 8th 3030/3050-3060/3080 condors for 17.50, w/SPX at 3058.

Expiring: June 1st 3010/3030 call spreads for 20.00. Condors bought for 16.65 last Tuesday.

#SPX1dte Expiring: June 1st 2910/2930-3110/3130 condors, sold Friday for 1.10.

No trades today but after a 12 week wait and 2 hours at the DMV I’ve finally got them and I can’t quit laughing!

🙂 🙂 🙂 🙂 🙂

Rolled $WORK Jun-05-2020 33.50 #CoveredCalls // Jun-12-2020 #CoveredCalls @0.05 Debit. Still ITM, but $0.50 better strike.

#shortputs #closing FEYE GPRO CAR

GPRO bought June 19 3.5 put for .04 sold May 18 for .18

FEYE bought June 19, 11 put .11 originally sold April 30 for .39, rolled May 5 for .72

CAR bought June 19, 20 put for .12, bought May 22 for 1.11

Original trade was a diagonal call spread, long 8/21 10 calls and short 6/19 20 calls. With the stock at 17.95 and 19 days to expiration, I rolled the 6/19 20 calls out to 7/17 20 calls @ 1.05 credit. Debit on original trade was 6.00, so cost basis now reduced to 4.95.

Rolled $TSLA 6/19 650/630 bull put spread up to 780/760 for 2.80 credit (short puts 17∆). Paired as an iron condor with 950/970 bear call spread. Stock at 884.00. Total premium for position now 7.50.

Bought to close 1 SPY 06/01/2020 298.00 Call / Sold 1 SPY 06/08/2020 300.00 Call @ 0.30 Credit plus 2.0 points higher on the short strike.

(Avoiding assignment for the call due to expire today)

#SPYLadder

Sold to open $LULU 6/19 320/330 bear call spread @ 3.05.

BTC a partial fill on the 40 puts for June 5 at .01, sold at .63

The all filled at .01 so, I am working on my 45 puts and 50 puts.

#coveredcalls WFC

Sold June 5, 27 call for .59

The FAAMGs Are Up 15% In 2020; The Remaining 495 S&P Stocks Are Down 8%

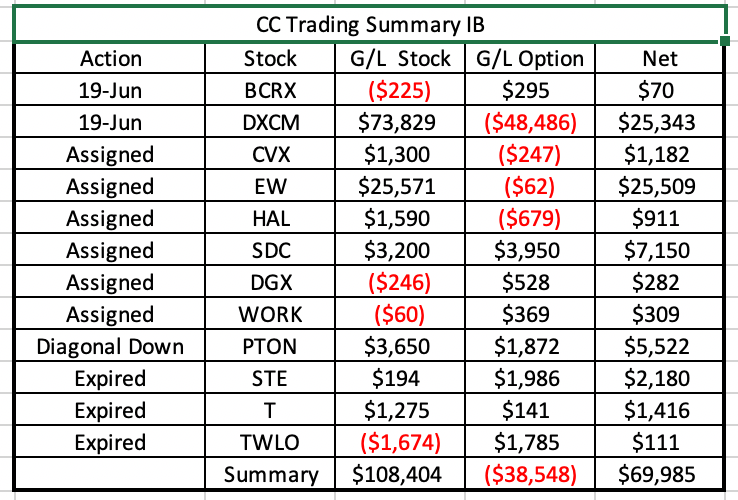

Overall net profits would be higher with just owning the stock (driven by DXCM and EW). Removing DXCM and EW from the calculation we have $19,000 in profit ($9,004 from stocks, $10,000 from short options).

6 positions assigned. 3 positions expired. 1 Diagonal down.

Moved to the cottage in Canada on Thursday. Issues with internet and couldn’t get trades done to roll positions and avoid assignment/expiration. Managed to get Schwab trades done but ran out of time with IB :(. Love the cottage…..hate the service.

WFC 28 covered call

VFC 52.50 put

TLRY 9.5 put

DXCM has been on a wild ride since early March with a low of $182.07 and a high of $428.59. The increase has made it a significant percent of my account. Interesting challenge to manage. Protect on the downside after such a run up and leave some upside. Getting called away will trigger a capital gain that I would prefer to manage over time (make it long term).

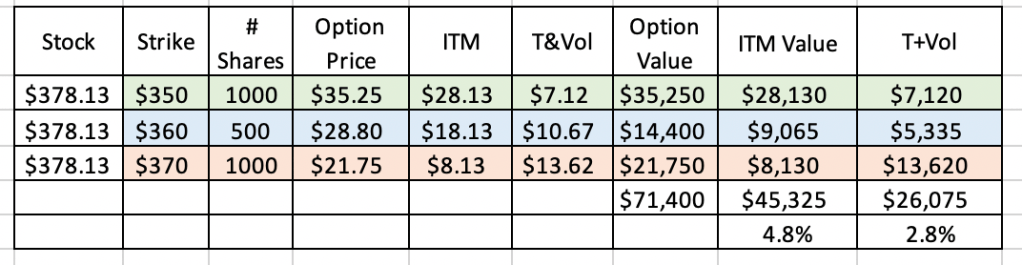

In mid May I switched to a “ladder” of strike prices under the stock price to increase the protection. I was not able to protect all of the gain. The stock has dropped $90,775 in value. Options have increased in value by $59,625 for a net loss of $31,510. The position has a profit of $90,305 in 44 days.

The current position is below. 4.8% protection and 2.8% upside. Options are all Jun 19 expiry (monthly only).

Not sure if I have done the right management. If I had known the stock would go on such a run I wouldn’t have sold the calls to start with! Hope this might help someone manage a similar position. Comments/suggestions are welcome.

New diagonal

Bought to open VXX Jan 21 2022 6.0 Puts / Sold VXX Jun 03 2020 31.0 Puts @ 0.09 Credit.

The short is 7 dte and the long is 602 dte, and I can write a new option every week.

Just a couple.

OX $LULU May-29-2020 250/260 #BuPS

OX $OXY May-29-2020 14.5 #CoveredCall

#optionsexpiration

$RAD 13.5 call

$ROKU 114 call

$ROKU 112 call

$AMD 57 call

$TQQQ 50 put Thank you @jsd501

$PFE 37 put

$DKNG 28 put Thank you @honkhonk81

$ZS 70/75 BUPS Earnings trade STO yesterday at 1.77

Expirations – everything else was rolled out a week

OXY 05/29/2020 17.00 Covered Calls

SLB 05/29/2020 19.00 Diagonal Calls

VXX 05/29/2020 30.00 Diagonal Puts

VXX 05/29/2020 30.50 Diagonal Puts

Assignments – no good roll was available for additional cash flow so I’m letting these go..

AA 05/29/2020 8.00 Covered Calls

WBA 05/29/2020 37.50 Covered Call (I got the initial time premium plus the $0.4575 Div)

AAL 11.0 CALLS STO @.66

AAL 10.0 PUTS STO @.58

ACB 11.0 & 13.0 PUTS STO @.39 & .55

ACB 18.0, 19.0,21.0 CALLS STO @1.18 & .73 & .88

DKNG 28.0, 32.0 PUT STO @1.10 & 1.30

DKNG 32.0 CALL STO @1.10 Stock will be called

OSTK 18.0 CALLS STO @1.00 MAYBE BTC for .15

OSTK 19.0 CALLS STO @.75

Bought to close VXX 05/29/2020 31.0 Diagonal Puts @ 0.01.

Sold VXX 06/05/2020 30.0 Puts @ 0.23.

#DoubleDip or #TripleDip against the long side positions

#shortputs

$AMD STO 6/5 50 puts at .78

#SPX1dte Sold to Open $SPX June 1st 2910/2930-3110/3130 condors for 1.10. IV: 17.3%, SPX 3040, deltas: -.05, +.05.

Expiring: May 29th 2920/2940-3090/3110 condors, sold yesterday for 1.10.

Today I STO the September 18, 35 puts at 1.63 and the 30 puts at 1.12

#SPX7dteLong Bought to Open $SPX June 5th 3030/3040-3050/3070 condors for 17.35, with SPX at 3043.

I realized today that I mistakenly SOLD my June 3rd 2990/3010-3020/3040 7dteLong condor instead of buying it (sold for 17.25 on Wednesday). So today I BTC the call spread for 11.00, and am now looking to close the put spread for 4.40 before the close.

Regarding today’s expiration, the sale of the 2940/2920 put side of my 1-dte condors yesterday effectively closed my long put spread of the same strikes I sold last Friday. So at the open today, I sold the May 29th 2960/2940 put spread for .85. That should expire with full profit.

BTO Debit IC Jun 5 234.5/236.5 227.5/225.5 $1.20

Bought to close SLB 05/29/2020 19.50 Covered Calls / Sold SLB 06/05/2020 19.50 Covered Calls @ 0.14 Credit

Bought to close VXX 05/29/2020 40.0 Diagonal Calls @ 0.01

Bought to close VXX 05/29/2020 32.0 Diagonal Puts @ 0.01.

Replaced these with VXX 06/05/2020 40.0 Calls @ 0.43 and VXX 06/05/2020 30.50 Puts @ 0.29.

#DoubleDip or #TripleDip against the long side positions

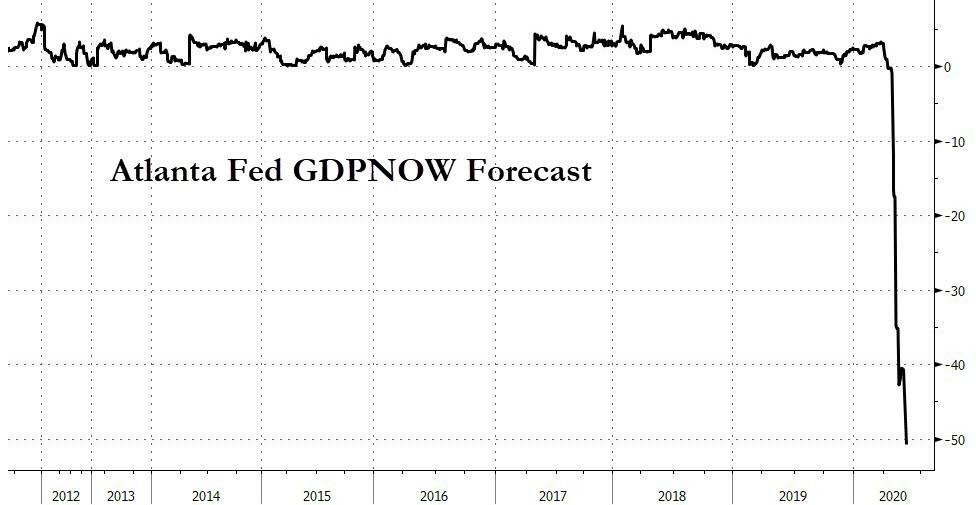

https://www.zerohedge.com/markets/atlanta-fed-now-sees-q2-gdp-collapsing-staggering-51

Nothing to see here

#JOBS report for May is Friday morning

Link to calendar: https://research.investors.com/economic-calendar/

#ShortPuts #CoveredCalls – Slow week but nice theta throughout the accounts.

NTAP: Old earnings trade still trying to work out of.

Bought to Close NTAP MAY 29 2020 45.0 Calls @ .01 (sold for 1.60)

Sold NTAP JUN 5 2020 44.0 Calls @ 1.09

SPY: Staying involved. Not nearly as heavy as I’ve been last 8 weeks.

Sold SPY JUN 19 2020 280.0 Put @ 2.50

UVXY: Feels like we’ll have some volatility though the election so trying to grab some put premium here.

UVXY MAY 29 2020 33.0 Puts expiring (sold for .86)

Sold UVXY JUN 5 2020 32.5 Puts @ 1.15

AAL BTO STOCK @10.45 A little add. Just a matter of time, and timing. ;>)

STNE STO 6/5/20 29.0 PUTS @.75

ACB STO 6/5/20 15.0 CALLS @.63

AAL STO 6/5/20 10.5 PUTS @.56

PLAY STO 6/5/20 PUTS @.65

PLAY STO 6/5/20 CALLS @.50

OSTK STO 6/5/20 CALLS @.60

$BIDU @ $103.80

Original trade:

Sold to open 1 BIDU May 29 108 short straddle @ $3.78

Bought to open 1 BIDU Jul 02 100 put / 115 call strangle @ $5.29

Net debit trade of $1.51

With BIDU moving down, need to roll the put side of the 108 short straddle

Rolled to the Jun 05, 105 short put for a debit of $0.92 – however, improving $3 in position.

Will let the May 29, 108 short call expire worthless and willing to take the risk by already opening the new short call leg to complete the $105 short straddle:

STO BIDU Jun 05, $105 call @ $2.20

The original Diagonal Butterfly was put on for a debit of $1.51, so the overall position now is in credit for $0.69.

STO $AMD Jun-05-2020 50 #shortputs @0.70.

7th week in a row. Small trade & would accept the stock if it gets assigned.

Bought to close CCL 05/29/2020 16.00 Covered Call / Sold CCL 06/05/2020 16.50 Call @ 0.30 Credit plus an extra half point higher on the strike for one more week.

BTC May 29, 60 puts at .01 and that is the last for that expiration.

Bought to close VIAC 05/29/2020 21.00 Diagonal Calls / Sold VIAC 06/05/2020 22.0 Calls @ 0.07 Credit plus an extra point higher on the strike for one more week.

Bought to close SLB 05/29/2020 18.00 Calls / Sold SLB 06/05/2020 18.00 Calls @ 0.22 Credit

Bought to close SLB 05/29/2020 18.50 Calls / Sold SLB 06/05/2020 19.00 Calls @ 0.02 Credit but a 0.50 higher strike for next week.

Still cash flow positive.

#SPX1dte Sold to Open $SPX May 29th 2920/2940-3090/3110 condors for 1.10. IV 22%, SPX 3026, deltas -.06, +.06.

Selling that actually closed the put side of my long condor. I want to sell it again to officially take the profit on my long and leave me short as intended.

Sold $BA 7/17 130/120 bull put spread @ 2.06, with the stock between 152 and 153. Short puts at 21 delta.

#rolling VIAC #shortputs CCL

VIAC Rolled June 19, 25 put to July 17 for .37

CCL sold June 5, 11 put for .40

Bought to close WFC 05/29/2020 27.50 Calls / Sold WFC 06/05/2020 28.00 Calls @ 0.24 Credit plus a 0.50 higher strike

Rolled short $MMM 9/18 115 puts up to 130 puts @ 1.50 credit with the stock at 159.17, new delta 16. This is the second rollup (from 100 to 115 to 130). Total premium collected now 5.12.

BTC May 29, 55 puts at .01 and waiting for my 60 puts order to fill at .01

Sold another lot of my SPY @ 306.12. Bought this on 3/16 @ 240.00

I honestly didn’t think it would get back here.

My last remaining lot was bought @ 230.00 and I will enter a sell order now another 2.50 higher.

ps. you’d think the VIX would be collapsing today as we hit new highs, but it is flat

$EWZ @ $27.26

Sold to open 1 EWZ June 05: 27 short straddle @ $1.62

Bought to open 1 EWZ Sep 18: 24 put / 30 call strangle @ $2.93

Net debit trade of $1.32

#coveredcalls WFC

Sold May 29, 28 call for 22, cost basis is 27.

BTC May 29, 50 puts at .01

Rolled $Work May-29-2020 33 #CoveredCall // Jun-05-2020 33.5 at @1.20 Credit.

#SPX7dte In pre-market, GTC order filled: Sold to close $SPX May 29th 2950/2970 call spreads for 19.00.

Condors bought for 17.35 on Friday. Will look to sell the put side for around 1.00.

Early assignment by the holder of the 05/29 13.00 covered calls I had sold (to get the 0.12 monthly dividend payment I guess).

At least one I won’t have to roll.

#CoveredCalls – Not much today. Just sitting and enjoying the rally (EWZ especially!). For risk reduction letting some stock go…

SPY stock called away @ 295.0 (basis 291.90)

Assigned these on a 300 put that I sold at the beginning of the implosion. Happy to be out of it…

Bought to close AAL 05/29/2020 11.50 Covered Calls / Sold AAL 06/05/2020 12.00 Covered Calls @ 0.12 Credit Plus a 0.50 higher strike

Bought to close WBA 05/29/2020 40.50 Covered Call / Sold WBA 06/05/2020 41.00 Covered Call @ 0.12 Credit Plus a 0.50 higher strike. (This gets the strike above my entry cost on the stock)

Sold off a little more of my SPY @ $303.62 in after hours trading.

Bought this lot @ $250 on 3/12.

The average cost on my remaining SPY is @ $233.33/sh.

#SPX7dteLong Bought to Open $SPX June 3rd 2990/3010-3020/3040 condors for 17.25, with SPX at 3019.

I did not close the put side of today’s condor. It went as high as 7.00 but I decided to hold it to see if I could get more. I had made 1.60 on the trade so it was a conscious decision.

#SPX1dte expiring: May 27th 2905/2925-30503070 condors, sold yesterday for 1.00.

#shortputs APPN

Sold June 19, 50 put for 1.00

#Earnings $NTAP reports tonight. Options trades need to be placed today to capture any earnings move. Below are details on earnings one-day moves over the last 12 quarters.

Feb. 12, 2020 AC -9.27%

Nov. 13, 2019 AC +3.17%

Aug. 14, 2019 AC +3.93%

May 22, 2019 AC -8.10%

Feb. 13, 2019 AC -5.47%

Nov. 14, 2018 AC -11.72% Biggest DOWN

Aug. 15, 2018 AC -3.58%

May 23, 2018 AC +1.93%

Feb. 14, 2018 AC -4.89%

Nov. 15, 2017 AC +15.91% Biggest UP

Aug. 16, 2017 AC -6.72%

May 24, 2017 AC +3.53%

Avg (+ or -) 6.52%

Bias -1.77%, negative bias on earnings.

With stock at 45.40 the data suggests these ranges:

Based on current IV (expected move into Friday per TOS): 42.28 to 48.52 (+/- 6.9%)

Based on AVERAGE one-day move over last 12 quarters: 42.44 to 48.36

Based on MAXIMUM one-day move over last 12 Q’s (15.9%): 38.18 to 52.62

Based on DOWN max only (-11.7%): 40.08

Open to requests for other symbols.

#closing FB BABA QQQ COF

FB Bought 242.50/245 #shortcallspreads for .48, sold May 22 for .83

BABA bought 170/175/230/235 #ironcondor for 1.10, sold May 22 for 1.37

QQQ bought 185/195/235/246 #ironcondor for 1.97, sold May 13 for 2.68

COF bought June 19, 50 put for .41, sold May 21 for 1.04 #shortputs

STO September 18, 45 put at 3.71

STO September 18, 50 put at 4.80

STO September 40 puts at 2.75

#closing #shortcallspreads DRIP

Bought 12 post split 14.59/51.42 June 19 call spreads for .01, sold as a 175/185 call spread on Feb. 25 for 2.08. I’ve been trying to close this for a few weeks. Thanks to you DRIP traders!

#SPX7dteLong In pre-market, GTC order filled: Bought to close $SPX May 27th 2980/3000 call spreads for 18.60. Condors sold last Wednesday for 17.00. Will sell put side early in the day.

#coveredcalls

$ROKU BTC 5/29 121 call and STO 5/29 114 call at 2.68 added credit

$CODX BTC 6/17 19 call and STO 7/17 22 call at .20 added credit

$NVTA BTC 6/17 17.5 call and STO 7/17 20 call at .30 debit.

$AMD STO 5/29 57 call at .65

$ROKU STO 5/29 112 call at 2.23

#shortputs

$DDOG STO 6/19 65 put at 1.70

#shortcalls

$SDGR BTC 6/19 70 call and STO 7/17 80 call at added cost of .80

BTO Jun 5 320/317.5 Puts $1.25

#in-out

Rolled profitable short puts out to July:

6/19 100 puts to 7/17 100 puts @ 1.08 credit

6/19 101 puts to 7/17 105 puts @ 1.73 credit

Stock at 125.55