I really like Fuzzy’s work on this. I’ve been doing loads of collars all year, but there’s times on a run up that I don’t want to chase the calls up, so I’ll let the position go. Then I’ll use some type of premium selling as a way to re-establish a position at a discount. Or if I want to add to a position, I can’t stomach buying at highs, but this is a great way to add in.

My favorite put selling strategy is a put ratio. My go-to is 45 DTE, buy 1x 30 delta and sell 2x 25 delta. THEN (since I’m more and more risk averse every year) I’ll often set a broken wing debit fly right at the breakeven on the put ratio to get me a few more $$ of break even room.

The part I’ve been missing though is the ladder dynamic of doing this campaign style.

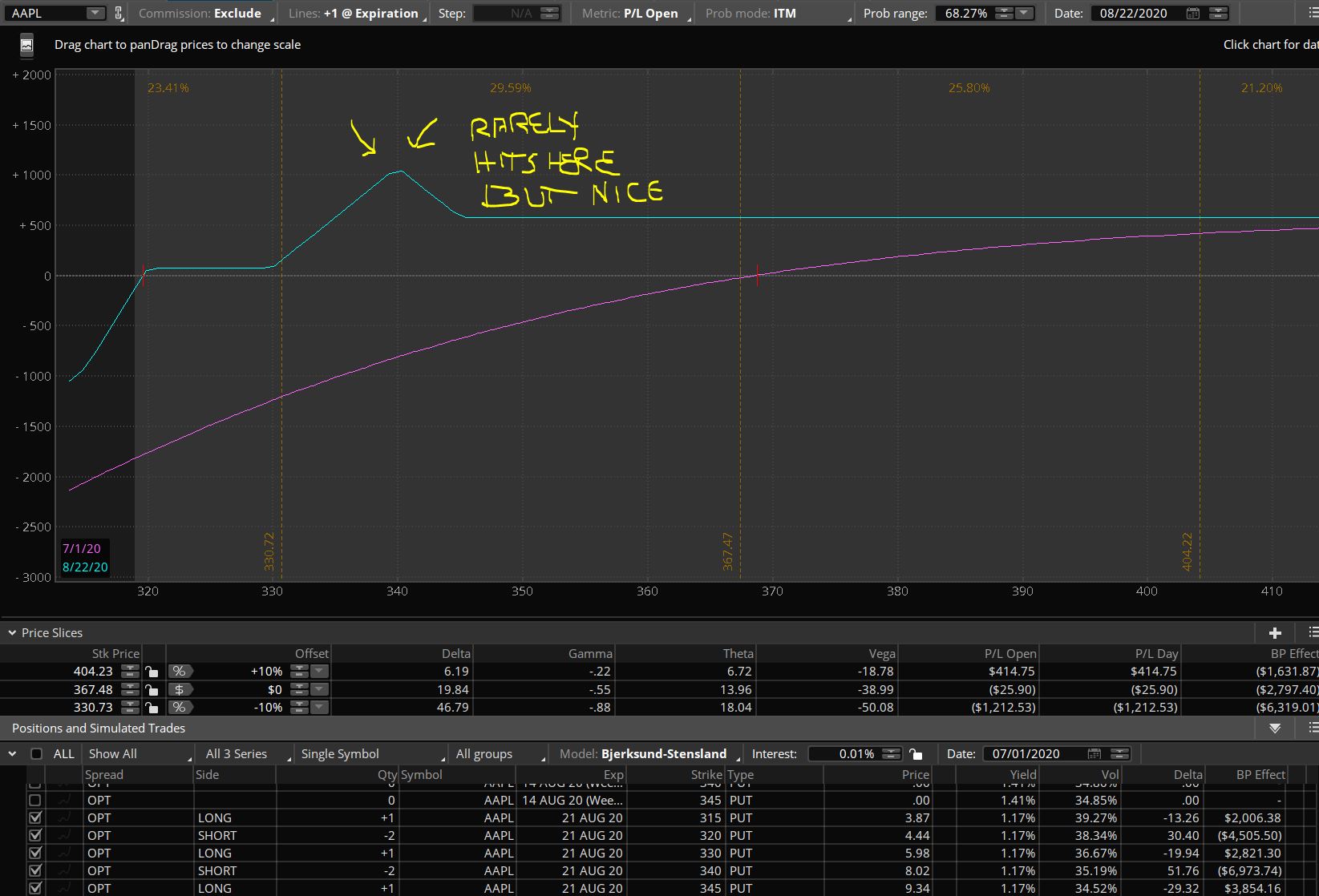

I have a small AAPL collar position right now that I’ve been wanting to add into. I’ve been doing weekly put ratios on it, but I’d like to flip to a laddering style like Fuzzy laid out in his post yesterday. Why AAPL? It’s the driving force behind both SPY and QQQ…as AAPL goes, so goes SPY/QQQ. But it has higher volatility than SPY, so more $$$ (mo’ money ties into probability).

I’ll do one of these every week, here’s today’s trade (I chose Aug 21 strike at 50 days for liquidity, had problems with fills on the Aug 14 expiry)

Bought to open qty 1 Aug 21 345 put @ 9.34

Sold to open qty 2 Aug 21 340 put @ 8.02

Ratio net credit 6.70, break even: $328.24 (roughly 18 delta)

Additional butterfly (hedge):

Aug 21 330/320/315 @ .97 debit

New breakeven: $319.69 about 13% down, 15 delta

I acknowledge the butterfly hedge eats into profits, but I’m happy w/ the trade off for the extra wide profit structure on these. Plus this is a much more complicated way of executing Fuzzy’s idea, but I really like the risk/reward on it.