#Fuzzy – BTO MU Jul20’18 52.5/52.5/50 Fuzzy for 3.80. Seems like the market is BTFD, possibly gonna cheer up soon? This synthetic position is unhedged at the moment. Dan Fitzpatrick featured this one in his free chart last night and brought it to my attention, so I will have to give him credit for the ticker.

Category Archives: Uncategorized

#earnings RH I sold an…

#earnings RH

I sold an April 20, 75 straddle for $1425, there was a good reason premiums were that high, RH ran up above break even of 90 to 95, has come back down to earth around 87, this might work out after all

Good morning

This should be fun today.

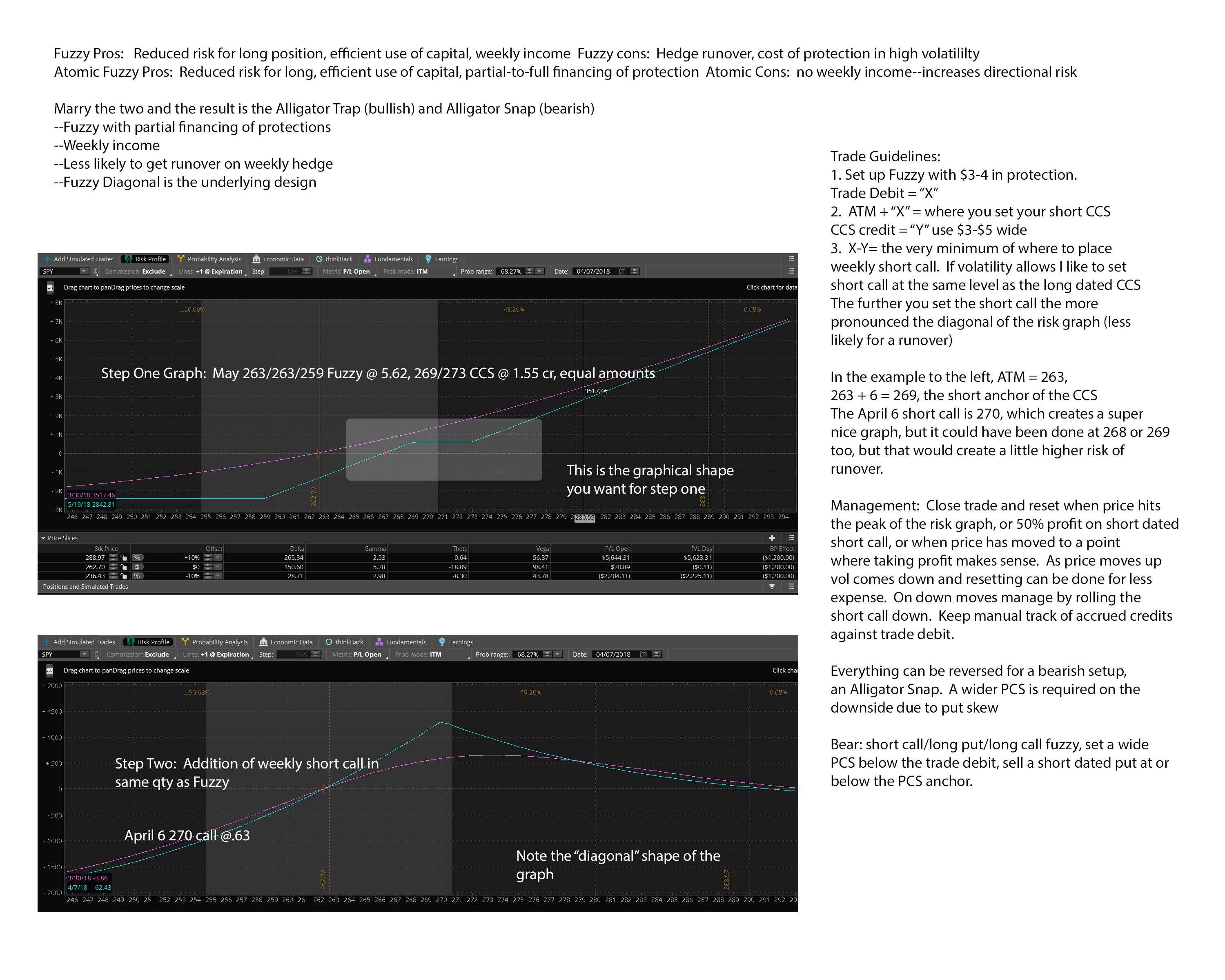

#AlligatorFuzzy Ok, here’s the latest…

#AlligatorFuzzy

Ok, here’s the latest entry into the #Fuzzy family.

Backing up a bit, there’s something every #Fuzzy has in common: A combo trade of a 2-part synthetic (long or short) coupled with protection for full risk definition. 3 legs, all the same expiration.

A Regular Fuzzy (the original one named after @fuzzballl) then uses short dated short hedges for trade debit recovery and weekly income.

An Atomic Fuzzy eschewed the short dated short hedges for a double size hedge using the same expiration as the core fuzzy–solving the problem of runover hedges.

Regular Fuzzy Pros: Efficient use of capital, risk defined, weekly income

Regular Fuzzy Cons: Protection very expensive in high vol, hedges frequently get runover

Atomic Fuzzy Pros: Efficient use of capital, risk defined, partial-to-full financing of protection (particularly useful in high vol)

Atomic Fuzzy Cons: No weekly income, which increases directional risk

Combining these two trades into a new trade solves the cons on both trades–it is essentially a Fuzzy Diagonal. There are two versions, an #AlligatorTrap is bullish, an #AlligatorSnap is bearish.

This trade uses both a long dated hedge (matching the core expiration and quantity) and short dated weekly hedges. The trade, in essence, has a triple hedge! Hedge #1: Core protection, Hedge #2: A credit spread using the core expiration, Hedge #3 A short dated short hedge. Believe it or not…perfectly legal in a 401K. I will be attaching a slide showing risk graph setups, a proper diagonal setup on the risk graph should significantly reduce the hedge runovers.

Here is the exact trade setup that I did last week for a long on SPY (captured on the attached slide)

SPY May monthly: +263c/-263p/+259p (this is the core fuzzy) @5.62 debit, then add a CCS 269/273, same qty, @1.55 cr. Then enter the weekly income hedge: Apr 6 270c @.63.

Particular setup rules: 1. The 3-leg core debit = “X” 2. Use ATM + X for the anchor short leg of the CCS. Those 5 legs should give you a “ledge” type risk graph where the ledge is solidly above 0. Finally add in the short dated short hedge–the best graphs work up with the calls at the same strike as the CCS anchor on the long dated core, or higher.

Everything can be reversed for a bear trade. Here’s an Alligator Snap (bear)trade I did on QQQ this morning:

Jun -157c/+157p/+160c @ 5.09, 152/147 PCS @ 1.34 cr ($157-$5=$152 for anchor). Then an Apr 6 152 short put @ .77. This puts the starting trade debit at $2.98. Accrued credits on rolling the short dated hedge will attack that trade debit. The bear side of this trade, due to put skew, will allow for more lucrative put rolls in an uptrending market.

So, in conclusion, this trade brings the best parts of the regular fuzzy (weekly income) and atomic fuzzy (protection financing) together. Check out the attached slide for risk graph setups, let me know your questions. I have about 8 of these trades on right now, 6 traps and 2 snaps. I’ve already rolled short hedges from last week.

Thanks to @MamaCash for the creative name…I was just going to call it a Fuzzy Diagonal….but Alligators are way more fun 🙂

2 of 3 of 5: Not yet!

Y’all know I’m keenly watching for 1-standard deviation up moves in SPX. We need 3 1SD up moves in a 5-bar window (for historical rally confirmations). We got one on Thursday. Today’s slipped through the fingers, darnit. We got a .933–the rule is it must cross 1.0. Wed and Thur still fall into the 5-bar window.

#AlligatorFuzzy anyone? I have a new #Fuzzy! I believe this is the best one yet. The love-child of regular fuzzy and atomic fuzzy. I will do a full write up on it maybe later tonight. I really think you will find it very compelling.

Sue

#ironcondor AMZN March 28, sold…

#ironcondor AMZN

March 28, sold April 20 IC for 2.00, closed today for .84. IV is still really high but I’m taking the gain.

TQQQ bearish fuzzy

STC January 2019 Bearish Fuzzy. Bought for 27.50 and STC for 29.55

STC 165 puts

BTC 165 calls

STC 170 calls

BTC April 20145 puts

#shortstrangles EWZ TastyTrade idea, sold…

#shortstrangles EWZ

TastyTrade idea, sold May 18, 42/47 strangle for 1.78

XBI

#SyntheticStock – Looks like it’s easing below the 200ma so I’m selling just above it…

Bought to Close XBI APR 6 2018 89.0 Calls @ .06 (sold for .83)

Sold XBI APR 13 2018 86.0 Calls @ 1.05

AZO

#BullCallSpreads – Letting this week’s expire so selling next week…cost basis reduction in the Jan Bull Call Spread…

Sold AZO APR 13 2018 640.0/670.0 Bear Call Spread @ 2.55

REGN

#SyntheticStock – With the weak market I’m rolling this thing back in and down. Hopefully can get it off the books a week sooner freeing up an extra sale.

Rolled REGN APR 20 2018 350.0 Calls to APR 13 2018 340.0 Calls @ .36 credit

#shortputs AMAT Sold April 20,…

#shortputs AMAT

Sold April 20, 50 put for .76

TSLA

#ShortStrangle – Had a one lot strangle where I closed the put side as the stock started imploding. Continuing to sell the call side while waiting to add the put side back in at some point.

Sold TSLA APR 13 2018 290.0 Call @ 1.45

PYPL

#SyntheticStock – Going out another week…

Bought to Close PYPL APR 6 2018 78.5 Calls @ .05 (sold for .80)

Sold PYPL APR 13 2018 76.0 Calls @ .94

LUV

#SyntheticStock – Order in to cover this week’s at a nickel. Selling next week into the tiny up move…

Sold LUV APR 13 2018 56.0 Calls @ .68

VXX

#BearPutSpreads – Selling against my Jan 2019 50/30 Bear Put Spreads….trying to gradually cover the debit.

Sold VXX APR 13 2018 46.0/41.0 Bull Put Spreads @ .63

OLED

#SyntheticStock – Selling well below the core but still bringing in enough to cover the repair of an old earnings strangle. Double sale with this week’s still running…

Sold OLED APR 13 2018 103.0 Calls @ 1.95

CRUS

#SyntheticStock #LongCalls – If I can close for a nickel on Mon or Tue and get next week’s sale going it’s well worth it to pay up I think…

Bought to Close CRUS APR 6 2018 43.5 Calls @ .05 (sold for .50)

Sold CRUS APR 13 2018 40.5 Calls @ .65

XLY

#SyntheticStock – I’m going to keep aggressively selling the rips for at least another week especially while premiums are so juicy…

Bought to Close XLY APR 6 2018 103.5 Calls @ .05 (sold for .73)

Sold XLY APR 13 2018 100.5 Calls @ .93

VXX this morning

#shortputspread AAPL Tradewise recommendation, April…

#shortputspread AAPL

Tradewise recommendation, April 27, 160/162.50. They see earnings on April 30 as supporting the price that has dropped 10%.

XBI

#Fuzzy – BTC XBI Apr06’18 91 calls for 0.04, sold for 0.46. Leaving my synthetic position unhedged for now (although waiting has not worked well lately!)

Could more pain help?

I thought this was an interesting view on the current #Market

SPX trades

#SPXcampaign Spent the morning doing mostly the reverse of yesterday… putting on call spreads and taking off put spreads.

Closed $SPX Apr 6th 2475/2450 put spreads for 1.30. Sold yesterday for 2.20.

Sold Apr 6th 2650/2675 call spreads for 3.65

Bought to Open Apr 13th 2450/2425 LONG put spreads for 2.30.

Sold May 4th 2760/2785 call spreads for 1.70.

Stopped Apr 27th 2460/2435 put spreads for 3.80. Sold Thursday for 1.75.

#ReverseRoll Sold Apr 13th 2670/2695 call spreads for 3.75.

AMZN

STO April 20, 1050/1100 bull put spread @ 1.20

Looks like I was too early on this one.

#supercharger this is the ITM…

#supercharger this is the ITM vertical debit spreads.

The adjustment to ERX yesterday is already paying off. With only a 0.24 increase in ERX, the long has gained and the short has decreased in time value so overall profit $750 on 10 contracts. Technically it is now a #fuzzy and that appears to be the way to adjust one that goes against you quickly and easily. Of course it has already moved through my short strike but will be easy to roll next week and have 41 weeks left of selling now to reduce cost basis. In 8 weeks should be a risk free trade.

Of all my positions yesterday, this one was the least underwater even though it was the biggest down percentage wise.

I will keep experimenting with these through all market conditions and see what is the best way to adjust them, what is the ideal time to put them on, and which conditions are ideal for them.

Will keep you posted as to how they work out longer term but think this may be a very viable trading idea. I may even buy the course, only $39 to see what the official recommendations are but with the trading brain power we have here I think we can figure it out! I also don’t think the course goes into adjusting, I think they just take them off at a set loss point.

#shortputs FEYE Rolled April 20,…

#shortputs FEYE

Rolled April 20, 17 put to May 4 for .40

Good Morning

Good Morning

VXX part 2

Sold $UVXY Apr 20th 26 calls for 1.45

Closed UVXY May 18th 20 call for 4.00. Sold for 2.50 on March 19th. This is my only position ITM. Closed one today and will close the other, and roll them to Sept higher strike.

Bought $VXX May 18th 30 puts for .05. I already had a couple of these; looking like a loss but why not add a handful more to make it a lottery ticket?

SPX calls closed

#SPXcampaign Closed $SPX April 13th 2745/2770 call spreads for .50. Sold in a #CondorRoll for 6.30 on 3/26… the call side was sold for 2.95.

#shortputs CRUS On March 16,…

#shortputs CRUS

On March 16, on a Motley fool recommendation(to buy the stock, not the option), I sold an April 20 40/45 put spread, just threw the 40 dollar, 40 put in for margin purposes, the short put being 1.85. My timing was impeccable as CRUS illogically is now at 38.75. I rolled the short 45 to June for a credit of 1.08, sold the April 40 long put for 2.35, staying naked on the June 45 short put. Of course, if CRUS was a buy at 45….

On the bright side…

Market Seasonality: April has closed green for the $SPX in 11 of the last 12 yrs w/ avg $SPX return coming in at 2.3%. Worth noting that Energy in April closed green in 7 of the last 10 yrs for an avg return of 3.71%.

— Stephanie Link (@Stephanie_Link) April 2, 2018

Another Downside Warning possible?

#VIXIndicator We exceeded 25% above Thursday’s close which is an additional signal. Secondary signals/warnings like this can sometimes signal a bottom, but it’s impossible to be sure. For those keeping track on this double-header correction:

1/16: First signal of trouble ahead/cancel Upside Warning

1/26: SPX high

1/29: Downside WARNING

1/30: 2nd warning

2/2: 3rd warning

2/5: six warnings in one day (a record)

2/9: SPX low

2/23: downside warning canceled

2/28: New downside WARNING

3/22: 2nd and 3rd warnings

Today: SPX lowest since 2/9

ETP

#ShortPuts

STO May18 16 puts @ 1.20

TQQQ

STO January 2019, 55 puts @4.70

Thanks to Fuzzball for the idea. I think I am going to stop selling puts or doing anything until I feel we have reached a bottom.

Who broke the market today?

#pietrades and rolling with some good premiums.

ANDV rolled 11 DTE 95 put to 25 DTE 93 put for 0.25 credit. Cost basis 90.78 if assigned.

NSC rolled 11 DTE 131 put to 25 DTE 128 put for 0.32 credit. CB 126.63 if assigned.

I will probably #jadelizard these if we get a bounce in next few days and also UTX but want better prices on a rebound.

ERX 21/26 4 DTE under water. Still some time value in the short option so will wait and roll later in the week. I will likely #fuzzy it to the Jan 19 call 20 strike, then just sell weekly options against it. With 41.5 weeks left would only need 0.19 per week to scratch the trade to zero so will probably sell OTM to give it a little room. I can roll the long option out and down for 4.15 right now and gain 41 weeks. 2-3 strikes oTM usually brings in 0.6-1 each week so this could be a good longer term trade.

Actually as I am typing this ERX going to parity, will roll it now.

New trade is a #fuzzy Jan 19 call 20 strike, rolled for 4.25 debit and the short 26 call rolled to next week 25.5 for 0.45. Total CB now 8.22 for 10 contracts. Work it down each week from here.

Trade wars should spike the price of commodities including oil so this should rebound.

SPX

BTO May 18 2770/2790 1.55 & 1 for 1.50

A Jeff trade, looking for a big run up. When I can cash out I will close 1 and let 1 run if conditions warrant

VXX gamin’

#VXXGame Sold $UVXY Apr 20th 25 call for 1.47.

BTC $UVXY Apr 20th 14 puts for .11. Sold for 1.05 on Mar 20th.

BTC $VXX Apr 13th 38.5 puts for .04. Sold for 1.10 on Mar 20th.

SPX puts sold

#SPXcampaign Sold $SPX Apr 6th 2475/2450 put spreads for 2.20. This is the spread I took profits on this morning, closing for .55. Now I’m using same strikes again for a new trade.

TQQQ

STO January 2019, 70 puts @6.90 with stock at 131

UVXY

#BearCallSpreads – Going up and out to Sep for this one…

Sold UVXY SEP 21 2018 30.0/40.0 Bear Call Spreads @ 1.20

#shortcallspreads TSLA Sold April 20…

#shortcallspreads TSLA

Sold April 20 290/300 for 1.18

SPX calls closed

#SPXcampaign

BTC $SPX Apr 19th 2820/2845 call spreads for .25. Sold for 1.95 on Mar 21st.

BTC $SPX Apr 19th 2825/2850 call spreads for .20. Sold for 1.65 on Mar 19th.

Whipsaw carries on

#SPXcampaign $SPX It was nerve-wracking selling calls on Thursday, but this approach is what’s needed with a VIX that can’t get far away from 20.00 in either direction. I closed out my Apr 6th spreads (the calls much too early), and now looking to pick the intraday low to add another put spread.

BTC Apr 6th 2725/2750 call spreads for 1.35. Sold for 3.25 on Thursday.

BTC Apr 6th 2475/2450 put spreads for .55. Sold for 2.80 on March 23rd.

STO May 4th 2400/2375 put spreads for 1.70.

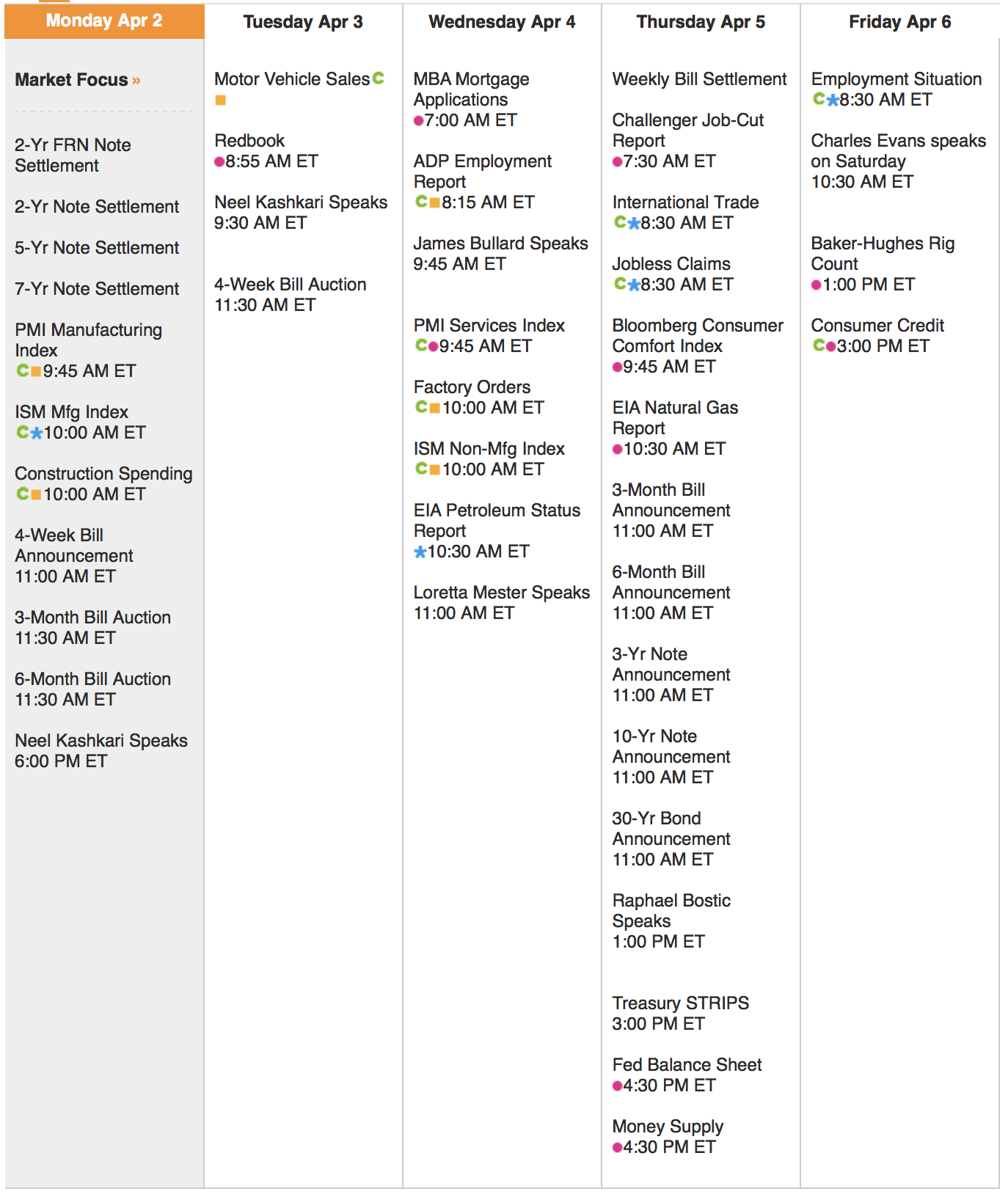

Econ Calendar for week of 4/2/18

Be sure to periodically click Home/REFRESH to keep Bistro features updated.

Jobs Report is Friday at 8:30am ET.

Good Morning

Good Morning

Taking the ITM vertical debt…

Taking the ITM vertical debt spread idea a little farther, here is an example. Best returns appear to be on the leveraged products but higher risk, obvious with the higher premiums. Here is a TQQQ example. 10 point spread, 20 DTE, 10 lot $1350 profit, max loss 8650 if you don’t manage it, and it is 33 points ITM now. Could it hit the short strike, possibly but would require more than a Feb 6 event to get there.

The more I look at these, the more I like. Easy to roll to #fuzzy if needed. Set up a ladder and would be a good income stream. Thoughts, other comments, see anything I am missing? I have an ERX one on now, it was challenged last week but never hit the break even point. I will likely roll it 3 weeks out this Thurs. or Fri. to avoid the assignment fees as long as it will close at or a few pennies shy of 5. If not will let it expire.

If it works I think we should call it a #supercharger

Wife is already asleep, daughter…

Wife is already asleep, daughter has a friend over so looking at some possible trade ideas. Taking the ITM debit spread a step further here are some numbers to consider. Based on closing prices all 22 DTE so we are comparing apples to apples. TNA as example, this is leveraged but with excellent weekly premiums. 10 contracts on all to keep the numbers consistent. These are all about 6 points ITM on the call side or 6 points OTM for the puts.

50/60 vertical debit spread cost 8.95 for a 10 point spread at expiration. Max profit $1050. Max loss $8950 but this can be converted. 11.7% ROC for a 140.4% annualized return.

60 strike CC 58.22. Max profit $1780. Max loss 58,220 for 3% ROC or 36% annualized.

60 put requires full cash secured because leveraged. 54,471 at risk for $1020 max profit, 1.87% return or 22% annualized.

All could be rolled or hedged if needed.

I am going to experiment more with these, like the idea, the returns, limited risk and can be done in a smaller account. Also could set up a ladder for an income stream. Right now have ERX going, may add FAS and TNA in small contract size in a few weeks.

Expiration

$SPX 2585/2610 What a year and it is only three months long.

Have a great Easter/Passover. Three days to enjoy on hopefully, a high note for all.

Thanks for all you help.

XBI

#Fuzzy – STO XBI Apr06’18 91 calls for 0.47.

Have a nice holiday everyone!

Have a nice long weekend

Back on Monday.

Happy Easter!

Enjoy the long weekend everyone! Resting up…16 underlyings with expirations next week. Gonna be fun!

This week in covered calls

Wednesday: BTC $BABA Apr 20 2.10 call for .35. Sold for 2.90 on Mar 15th.

Today:

BTC BABA Apr 13th 205 call for .20. Sold for 2.05 on Mar 6th.

STO BABA Apr 27th 200 call for 1.90

STO $FB Apr 27th 175 call for 1.60

STO $AAPL Apr 27th 180 call for 1.55

RH roll

#Earnings #StrangleRoll

BTC $RH Mar 29th 91.5 calls for 4.30. Sold in 65/91.5 earnings strangle for 2.53 on Tuesday.

STO $RH Apr 20th 87.5/100 strangles for 4.535.

WFC

STO September 45 puts @ 1.08

STO October 40 puts @ .61

XBI strangle

Idea from TastyTrade

Sold $XBI May 18 75/96 strangles @ 1.85

XBI currently at 88.96

SPX puts sold

#SPXcampaign Sold $SPX Apr 27th 2460/2435 puts for 1.75.

This does not fit into my approach of selling at extremes, but it is the last hour of the week and I had not sold my standard second put spread. Since VIX has not dropped too much I am not assuming the big down days are over. I will sell some additional calls if we close higher. Or puts if we sell off into the close.

FAS Fuzzy

BTO 2020,63,63,61

Sold 6April 13, 65 calls @2.53

#pietrade BTC the ANDV 108…

BTC the ANDV 108 call 15 DTE for 0.25. Sold for .95. Part of a strangle. Leaving the 95 put on still has .70 left.

When I roll the put will convert to #jadelizard. I violated my own rule of selling naked calls on individual names as a recovery for the dip(s). Strangles on ETF’s and indexes are ok because the entire ETF will not be bought out by another company. I had to pay up when Berkshire bought heinz a few years ago so learned my lesson on uncovered calls on a single company. Will unwind UTX and NSC calls as soon as they decay a little, hopefully over the long weekend.

Sold Early SPX / SPX Campaign

Sold Early

#spxcampaign

$SPX BTC 3/29 2600/2625 at 2.00 STO at 1.60. At one time this trade down A LOT. Glad to close it at a small loss even though market looks strong. I am not strong! 😉

#spxcampaign

$SPX STO 4/13 2745/2720 BECS at 3.50 Thank you @jeffcp66

XBI # fuzzy

BTO January 2020, 88,88,86

STO April 91 calls, total cost of 12.35

EWW

#SyntheticStock – Forgot to do this til now: BTO EWW Jan17’20 52/52/50 synthetic for 5.00. Max loss would be 7.00, trade runs for 94 weeks so need 0.075 cents a week to break even. STO EWW Apr06’18 52 calls for 0.30. Been needing something long term and stress-free (I hope!). Thanks to @fuzzballl!!!

VXX

#BullPutSpreads – Closing the short side of BuPS sales that I sold to finance Jan 2019 BePS. I’ll leave the long side and maybe get lucky next week.

Bought to Close VXX APR 6 2018 40.5 Puts @ .05 (sold spread for .47)

#pietrades A bunch today since…

#pietrades A bunch today since this is effectively expiration day. But it is nice out, first day can wear shorts here so going outside as soon as all the trades execute, still working 1 order.

GM Rolled 38.5 CC 22 DTE to 29 DTE for 0.17 credit. CB now 38.33. Taking forever to work this one back, will just be happy to scratch it so I can use the money somewhere else. For those following, I am taking this off the #pietrade list for a while, weekly premiums are not good enough for as much as it is moving around and to prone to steel tariff tweets.

FAS today 65 CC to next week 64 CC for 1.58 credit. CB 62.07

FAS today 64 CC to next week for 1.59 credit. CB 61.11

LNG Apr. 6 to Apr. 13 55 CC down to 54 CC for 0.52 credit. CB 53.27

ANDV 95/108 15 DTE strangle looking good, probably roll Monday to new week but #jadelizard the call side.

ERX 21/26 long debit 8 DTE should expire for full profit next week. If for some reason stays below 26 will convert to #fuzzy. I can add another 9 months to the long call for $3 and can sell $2 in premium each week, kind of a no brainer. However, this is also part of a deep ITM #syntheticcoveredcall experiment so my plan is to actually roll it next week and re-establish the position. On a percentage basis looks like a 13.7% return every month with moderate risk but very little work. Potentially a 160% annualized return so this is worth trying. I think this is what Chuck Hughes does to get some of his high returns. Buy deep ITM call with almost no time value, then sell ITM call that has a decent amount of time value left. Gives 10-20% downside protection and can still make max profit. I will keep one of these running for a while and report the results as it unfolds. Cheaper way to play a CC or #fuzzy maybe.

NSC 131/143 strangle 15 DTE. It moved around so much still at break even. Hope some theta decay will make some profits this weekend. Earnings late April so will only roll the put side.

UTX 122/132 strangle 36 DTE. Had to adjust. Same problem as NSC. Will let some of the premium suck out of it then only roll the put side. Earnings late April or I may #jadelizard both so there is no risk to the upside.

Hoppy Easter as the kids say! Hope everyone has a good long weekend.

I am still showing paper losses from the SVXY implosion. My net liq. keeps going down because of all the adjusting, only 1 positive week since Feb 6 but it was a good one. However, once these all close will have a nice bump finally and the theta decay is huge now, close to 800 per day, just need a few days of not whipsawing so it makes a difference. Once everything closes in 1-3 weeks will at least be positive for March.

Cheers, Chris

REGN

#SyntheticStock – Been selling against this all the way down. It’s in a squeeze and attempting to get off the ground but seems to get rejected right around this level each time. Rolling up and out a little for now…

Rolled REGN APR 6 2018 340.0 Calls to APR 20 2018 350.0 Calls @ .40 credit

AZO

#BullCallSpreads – Letting this week’s expire so selling next week…cost basis reduction in the Jan Bull Call Spread…

Sold AZO APR 6 2018 660.0/690.0 Bear Call Spread @ 2.50

XBI

#SyntheticStock #IRA – Thanks @1strangealien for getting this one back on my radar. I’ll take a shot out in Jan.

Bought to Open XBI JAN 18 2019 88/88/86 Synthetic Stock @ 7.69 (filled better than mid)

Max loss of 9.69 with 42 weeks to run requiring 23 cents per week to cover.

So:

Sold XBI APR 6 2018 89.0 Calls @ .83

XOM

Rolled Mar 29 76/74 BuPS to May 4 76/73 .30 Db need to add call to try to come back with this one. #Fuzzy did not work so far

BTO May 4 76 1.08

FAS

#SyntheticStock – Getting the next sale going. Going out two weeks to give it a little room with much better premium with bank earnings cranking up. JPM on the 13th and MS GS and BAC the following week so premiums should be pretty sweet that week too.

Bought to Close FAS MAR 29 2018 65.5 Calls @ .03 (sold for .85 as a bonus week 🙂 )

Sold FAS APR 13 2018 65.0 Calls @ 2.15

LUV

#SyntheticStock – Looks safe this week so selling next week on this tiny pop…

Sold LUV APR 6 2018 57.5 Calls @ .54

XOM

#SyntheticStock – Next week’s sale…still a weak looking chart but starting to form a nice squeeze. Gonna see if I can “squeeze” in one more aggressive weekly before this thing rebounds and runs to glory (or not 🙂 ). Jumped the gun on it…could do a little better now.

Sold XOM APR 6 2018 74.0 Calls @ .60

Expiration /Rolled LABU CC / AMZN IC / Close Early BIDU BECS / FB BUPS

#optionsexpiration

$SPX 2500/2525 BUPS Thank you @jeffcp66

#shortcalls

$LABU BTC 3/29 90 calls STO 4/13 87 calls for 2.14 credit

#ironcondor

$AMZN STO 1180/1190/1610/1600 IC for 1.95 Thank you @thomberg1201

#shortputs

$FB STO 4/20 135/145 BUPS at 1.85

Closed Early

$BIDU 4/20 290/280 BECS at .15 STO at 2.05

SPX Trades

STO May4th 2425/2525 BUPS at 15.10 credit….

XBI

#Fuzzy – Right before close BTO XBI Jun’18 88/88/86 synthetic stock position for 3.70. Unhedged for now. XBI printed a dragonfly doji today and Tech is due a bounce, right? Crossing fingers and toes.

XOM

#SyntheticStock – Right at the bell…no time to sell next week.

Bought to Close XOM MAR 29 2018 74.5 Calls @ .03 (sold for .48)