#ShortCalls #VXXGame – Just for good measure since I’ve got some decent size short volatility trades going…come and get this Mr. Market!

Adding one strike higher than yesterday…

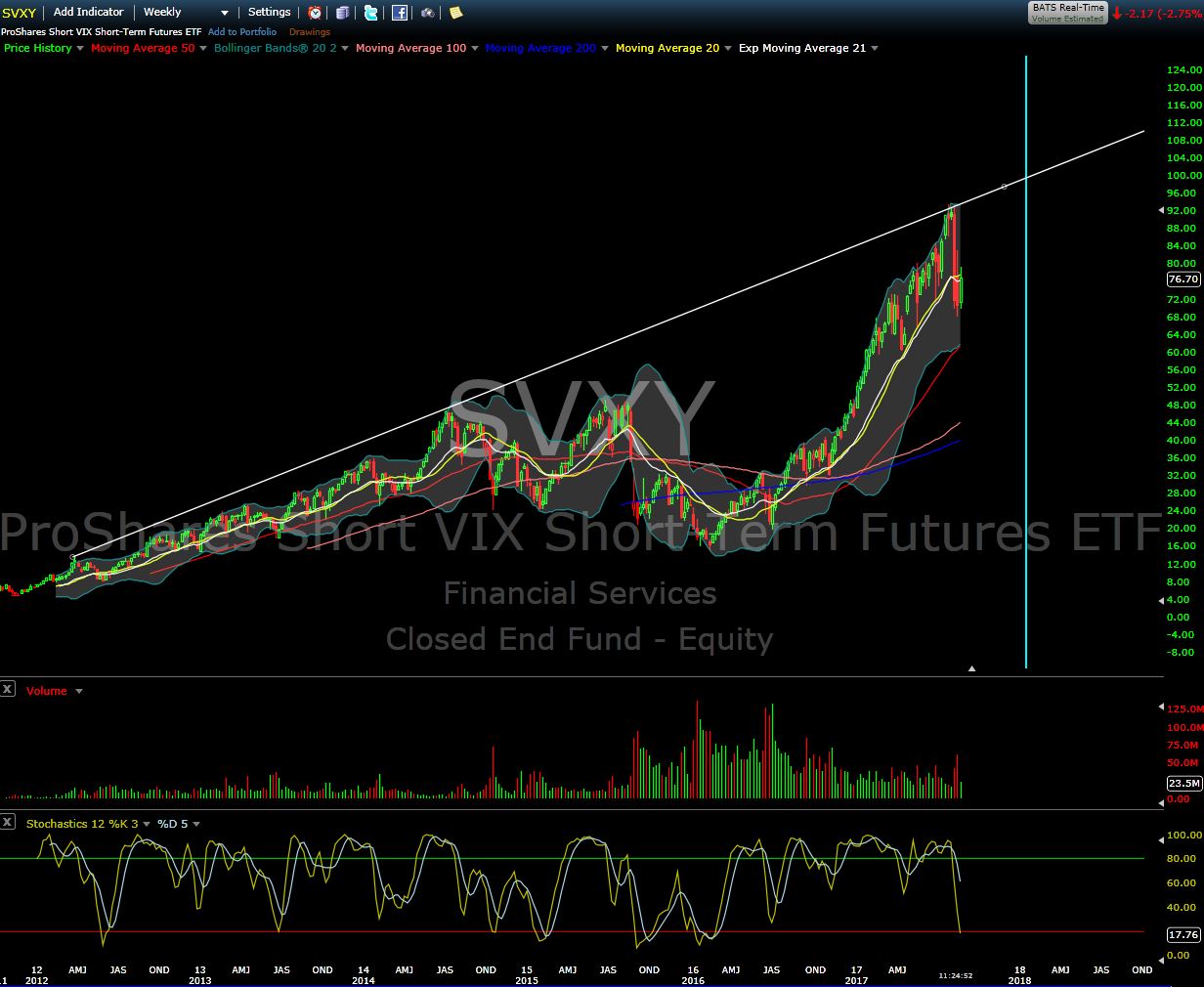

Sold SVXY DEC 15 2017 102.5 Call @ 2.00

#ShortCalls #VXXGame – Just for good measure since I’ve got some decent size short volatility trades going…come and get this Mr. Market!

Adding one strike higher than yesterday…

Sold SVXY DEC 15 2017 102.5 Call @ 2.00

#LongPutDiagonals #SyntheticShortStock – Adding a position on VXX similar to the UVXY position. I’ll let ’em race each other down and see what works the best.

—————

Synthetic short stock with disaster long calls (16.60 debit)

Sold VXX JAN 18 2019 50.0 Calls

Bought VXX JAN 18 2019 50.0 Puts

Long call for possible disasters capping potential losses:

Bought VXX JAN 18 2019 55.0 Calls

Buying the disaster calls pretty close to help with margin requirements if she spikes…

—————

Weekly put sale against synthetic short stock to really boost the profits on this trade:

Sold VXX SEP 1 2017 46.0 Puts @ .60

—————

So now what? Two extremes examined here….

VXX goes to 100 and stays there:

I lose my 16.60 debit and an additional 5 dollars to the upside capped by the disaster calls. But…selling premium at 60 cents a week until Jan 2019 brings in 43.80 points so still a net gain of 22 points for the whole ordeal. Margin requirements for now are 7 points per spread. Not a bad return even in worse case scenario.

VXX does what it usually does:

So VXX eases it’s way down to 10 again. Synthetic stock makes 40 points and weekly premium sales at just a measly 60 cents brings in another 44 points for a gain of 84 points minus the 17 debit (rounding) works out to a 67 point winner.

I expect this one to be easier to manage since the VXX drop isn’t as severe as the amount UVXY can tank. Might actually work out better in the long run due to the weekly premium sales…

#ShortStrangles – New position selling well before next earnings. Strangling near the 200ma and above all time high.

Sold TSLA SEP 29 2017 300.0/400.0 Strangle @ 4.20

#ShortCalls – January positions look pretty safe so let’s take a small shot in Dec and give it something to shoot for. Gonna take a lot of work and repair to get back to all time highs and to exceed the trend line that’s stood the test of time as a guide to my call selling. Still some nice premium in these but going with a starter for now…

Sold 1 SVXY DEC 15 2017 100.0 Call @ 2.60

Anyone know a good ETF with weeklies and decent volume? XTN no options and IYT no weeklies. Anything else?

#ShortStrangles – Back into an old favorite…filled at the open but could do better now.

Sold REGN SEP 29 2017 430.0/530.0 Strangle @ 7.00

#LongPutDiagonals – Impressive volatility collapse. Making an adjustment here.

Rolled UVXY SEP 1 2017 31.0 Puts to SEP 22 2017 29.0 Puts @ .96 credit

#ShortStrangles – Current position nicely profitable so adding one a couple weeks further out.

Sold NVDA SEP 29 2017 150.0/180.0 Strangle @ 4.65

#CoveredCalls – This roll puts the position back in the green…

Rolled ISRG SEP 1 2017 900.0 Call to SEP 22 2017 902.5 Call @ .65 credit.

Planning 2 more rolls on it. Next one will be into first or second week of October just prior to earnings. Then the final roll will be into earnings for a nice credit. I’ll keep the strike well in the money for downside protection and gather up some premium and then ship it!

#ModifiedVXXGame – Last week sold some 11/13 VXX call spreads for a buck. Sold them in a size where after the split they’ll be one tenth of a full position. Didn’t quite make it back to profitability so closed the long 13 calls on Friday and accepted the short assignment at a basis of 12.30

Then:

Sold VXX AUG 25 2017 12.0 Puts @ .13

I’ll be shorting the stock or selling aggressive call spreads to establish a short position after the split. Working towards a long term short position with protective calls to match up with a similar trade on UVXY.

#LongCallDiagonals – Lots of overhead resistance. Rolling down this week for additional credit.

Rolled AMZN AUG 25 2017 975.0 Call to AUG 25 2017 957.5 Call @ 3.60 credit.

Total credit on this one now up to 13.50

#Earnings – Lottery ticket going away today. Taking the .25 loss and moving on. No desire to take the stock of a company that might not be around on Monday!

#LongPutDiagonals – Keeping the theta rolling in…

Bought to Close UVXY AUG 25 2017 29.0 Puts @ .25 (sold for 1.25)

Sold UVXY SEP 1 2017 31.0 Puts @ 1.30

#IRA – Moving out to March…

Sold SVXY MAR 16 2018 35.0 Put @ 3.25

#IRA – First ones in this expiration…

Sold UVXY SEP 29 2017 50.0/61.0 Bear Call Spreads @ 1.42

#IRA – Adding to an existing position at higher premium…

Sold UVXY MAR 16 2018 40.0/50.0 Bear Call Spread @ 1.70

DUST has options out to 2019 but NUGT only to next March. What’s up with that?

#IRA – Adding a new position. Staying small since the only way to roll these for a credit if they end ITM is to widen or add contracts.

Sold UVXY DEC 15 2017 50.0/60.0 Bear Call Spreads @ 1.18

#ShortPuts #IRA – Adding a couple…

Sold SVXY DEC 15 2017 50.0 Put @ 4.40 (top of my ladder)

Sold SVXY JAN 19 2018 35.0 Put @ 2.45

#LongPutDiagonals #SyntheticShortStock -Adding here. Could’ve moved up to 35’s but to keep things simple I’m staying with the same strikes for now. Waiting to sell any additional puts.

Synthetic short stock with disaster long calls (17.25 debit)

Sold UVXY JAN 18 2019 30.0 Calls

Bought UVXY JAN 18 2019 30.0 Puts

Long call for possible disasters capping potential losses:

Bought UVXY JAN 18 2019 40.0 Calls

#ShortCalls #VXXGame – Sticking to strict position size limits on my naked sales of these things. Booking pretty decent quick profits from the other day and re-selling higher strikes for safety.

Bought to Close UVXY SEP 15 2017 82.0 Call @ 1.07 (sold for 3.40)

Bought to Close UVXY DEC 15 2017 82.0 Call @ 6.15 (sold for 9.60)

Sold UVXY DEC 15 2017 91.0 Call @ 6.00

Sold UVXY JAN 19 2018 91.0 Call @ 7.20

Busy week away from the market again but still adding an experimental position on UVXY. Low risk high reward playing it’s long term downtrend. Reverse Whiz style.

#LongPutDiagonals #SyntheticShortStock – I’ll be adding a similar position on VXX after the split next week. I’ll let ’em race each other down and see what works the best.

BTW…TDA portfolio margin for this trade is only 2600 increasing to 4000 if UVXY doubles overnight…

——————–

Synthetic short stock with disaster long calls (17.75 debit)

Sold UVXY JAN 18 2019 30.0 Calls

Bought UVXY JAN 18 2019 30.0 Puts

Long call for possible disasters capping potential losses:

Bought UVXY JAN 18 2019 40.0 Calls

——————–

Weekly put sale against synthetic short stock to really boost the profits on this trade:

Sold UVXY AUG 25 2017 29.0 Puts @ 1.25

——————–

The plan:

Sell weekly for the next 74 weeks and let the thing decay. Hopefully capture 10 dollars of the move from 30 to 10.

Once I get a little profit under it I’ll reduce the size or possibly eliminate the disaster calls so I’m only treating those as a temporary expense. Once I remove the disaster calls and get some of that debit back I don’t see how this thing can’t make any less than 100 points per spread with very little stress and risk.

#ShortStrangles – Caught an upgrade this morning. These analysts can be annoying sometimes.

Rolled WYNN AUG 18 2017 128.0 Puts to WYNN AUG 18 2017 133.0 Puts @ 1.00 credit

#LongCallDiagonals – Small roll until this thing proves it can get through the 50ma…

Rolled AMZN AUG 18 2017 970.0 Call to AUG 25 2017 975.0 Call @ 1.00 credit

32.80 in front month premium received in just 17 days. Trade could run as much as another 96 weeks to June 2019…

Gonna classify this under a new hashtag. The infamous #LongPutDiagonals although it will probably more than likely end up being a long term short stock position after the upcoming split. For now just messing around this week to get started…about a one-tenth position size.

Sold VXX AUG 18 2017 11.0/13.o Bear Call Spreads @ 1.00

Makes money below 12 and gets me some short stock if she spikes…I’ll add the rest after the split.

#PerpetualRollingStrangles – For safety since I’m pretty heavy on the put side…

Bought to Close GLD AUG 18 2017 121.0 Puts @ .25 (sold for 1.15)

#ShortStrangles – Sold the puts pretty conservatively the other day waiting for a bounce. Looks like we’re getting it so moving up to just under the 50ma…

Rolled NVDA SEP 15 2017 135.0 Puts to NVDA SEP 15 2017 155.0 Puts @ 3.55 credit.

Position is now 155/175 Strangles @ 7.30

Crashed all my watchlists. Guess I know how I’m spending my day. They can’t fix it either…

Just announced 3 for 1 split for September. Should be a much better trading vehicle after that. It’s another position I’ve been working awhile to get back to even. Long stock covered with a 900 call and breakeven of 903. One more roll and she’ll be green finally.

https://globenewswire.com/news-release/2017/08/11/1083856/0/en/Intuitive-Surgical-Board-of-Directors-Approves-a-Three-for-One-Stock-Split.html

#PerpetualRollingStrangles – Could Gartman be right? LOL…rolling out short calls and double selling puts until she turns around.

Rolled GLD SEP 15 2017 117.0 Calls to NOV 17 2017 118.0 Calls @ .21 credit

And:

Sold GLD SEP 1 2017 122.0 Puts @ 1.00

This was an additional sale of a full position. Still holding a full position of 121’s for next week with a stop on them at 50 percent of max gain.

#ShortPuts – Small in the #IRA replacing the ones closed earlier this week. These are right around the 200ma…

Sold NVDA JAN 19 2018 110.0 Put @ 2.50

Sold NVDA JAN 19 2018 120.0 Put @ 4.25

Closed these earlier this week hoping for some gold volatility to re-sell…

Bought to Close NUGT DEC 15 2017 58.0 Call @ 1.29 (sold for 4.30)

Bought to Close DUST DEC 15 2017 50.0 Call @ 1.50 (sold for 3.90)

#ShortStrangles – This is actually a good thing. As the puts get gradually rolled down we’re getting closer to the short 120 calls. Keep going!

Rolled WYNN AUG 11 2017 129.0 Puts to AUG 18 2017 128.0 Puts @ even

#IRA #ShortPuts – Another one I missed earlier this week. They were pretty profitable so didn’t want to hold through earnings.

Bought to Close NVDA JAN 19 2018 100.0 Put @ 1.08 (sold for 3.50)

Bought to Close NVDA JAN 19 2018 110.0 Put @ 1.80 (sold for 5.50)

#ShortPuts #VXXGame – Earlier this week:

Bought to Close SVXY SEP 15 2017 42.5 Puts @ .50 (sold for 1.15)

Bought to Close SVXY SEP 15 2017 45.0 Puts @ .57 (sold for 1.27)

Replacing with these and smaller:

Sold 1 SVXY DEC 15 2017 40.0 Put @ 2.77

Sold 1 SVXY DEC 15 2017 45.0 Put @ 3.63

#NewStrikes #VXXGame – I’ve been sticking mainly to spreads in this thing way out in time for peace of mind and to keep from getting too big. With the NVDA position out of the way I feel more comfortable dipping a toe in on the naked side. Thanks @Iceman for pointing these out. New highest strikes…

These are 200 percent above the all time lows…sometimes that’s not enough so staying small.

Sold 1 UVXY SEP 15 2017 82.0 Call @ 3.40

Sold 1 UVXY DEC 15 2017 82.0 Call @ 9.60

#LongCallDiagonals – Keeping up with a lot of the drop. I’ll be selling these aggressively and then hopefully getting out of the way on the way back up (if there is one 🙂 ).

Bought to Close AMZN AUG 11 2017 970.0 Call @ .68 (sold for 17.00)

Rolled this call down from 1000 to 990 to 980 to 970 collecting additional premium all the way down…

Then:

Sold AMZN AUG 18 2017 970.0 Call @ 8.93

Sure can feel the difference in a slightly higher VIX in all options. I’m good with 15 for awhile!

#ShortStrangles – Back in….selling at the 100ma and all time high (and much smaller than last time)

Sold NVDA SEP 15 2017 135.0/175.0 Strangles @ 3.75

#Earnings #ShortStrangles – Well, after quite a few weeks (months 🙂 ) of rolling and adjusting and collecting premium I’m out with a decent profit on a too big position.

Bought to Close NVDA AUG 11 2017 177.5/160.0 Inverted Strangles @ 20.50 (sold for 27.75)

Was hoping to keep more of it but happy to be out with a winner. Now, looking to get back in on this dip…

#ReverseSplit – In a couple weeks…

http://www.businesswire.com/news/home/20170809006219/en/Barclays-Bank-PLC-Announces-Reverse-Split-iPath%C2%AE

Maybe one to watch if missles start flying…

Busy most of the week but popping in for a second…

#IRA #ShortPuts – Freeing up a ton of margin just in case…booking these that still have nice profits. Hopefully we’ll get MUCH better entries soon!

Bought to Close SVXY SEP 15 2017 42.5 Puts @ .50 (sold for 1.15)

Bought to Close SVXY SEP 15 2017 45.0 Puts @ .57 (sold for 1.27)

Bought to Close SVXY JAN 19 2018 30.0 Puts @ 1.40 (sold for 2.00)

Bought to Close 10 UVXY1 JAN 18 2019 5.0/15 .0 Bear Call Spreads @ 1.70 (sold for 2.92)

Is it just me or does this sound slightly condescending? Seems like it could’ve been worded better. Maybe my reading comprehension sucks too…LOL

—————————————-

Scott,

It’s been 6 months since we last heard from you, and I wanted to know if you’re still interested in learning to trade profitably. If not, just shoot me back a note and I’ll close down your record.

If you are interested, let me know and I’ll send you back a free month trial to Stock Market and Option Market Mentor.

Please reply today, so I can remove you or help you.

Thanks!

Gary

—————————————-

My reply:

You can close me out…thanks Gary. By the way…the email is a little funny sounding. Makes it sound like the person you’re sending it to is not interested in trading profitably unless they come back. Sounds condescending although I’m sure it wasn’t meant to be. 🙂

Scott

—————————————-

I haven’t been posting any of the #PerpetualRollingStrangles positions but still in them and working. I was getting early exercised a couple times on some DITM TLT. Sometimes as early as 18 days out they were getting tagged. So based on some TT research and trying to maximize P/L per day I’ve been rolling the ITM positions about 3 weeks early and resetting to the 45 day mark. I’ve noticed a huge improvement in daily swings and a nice steady rise in the gains for the positions.

FWIW…

#Earnings – Here’s one that’s been a work in progress because it’s been so strong. During it’s earnings run up starting last April I’ve been rolling puts up and went inverted as she passed through my short call at about 875. Finally leveled off and I took the stock at a 904 basis. Since then been rolling the ITM call up.

So finally:

Rolled ISRG AUG 18 2017 895.0 Call to SEP 1 2017 900.0 Call @ .40 credit.

Almost back to even. As Sep approaches have to decide whether to say goodbye at even or keep rolling up to finally get some gains. It’s finally showing some weakness. What a run!

#Earnings – Stock feels kinda strong so booking this earnings trade now.

Bought to Close TSLA AUG 4 2017 350.0/345.0 Inverted Strangle @ 6.85 (sold for 9.05)

#Earnings – Managing the earnings implosion. Rolling and selling to get the deltas to a more reasonable level.

Started with a scalp:

Bought to Close AAOI AUG 4 2017 75.0 Calls @ .80 (sold for 1.10)

And got all the short puts into same expiration for simplicity:

Rolled AAOI AUG 11 2017 90.0 Put to SEP 22 2017 85.0 Put @ 1.10 debit

Rolled AAOI AUG 18 2017 85.0 Put to SEP 22 2017 85.0 Put @ 3.07 credit

Rolled AAOI AUG 25 2017 80.0 Put to SEP 22 2017 80.0 Put @ 2.54 credit

Against all of that:

Sold AAOI AUG 11 2017 75.0 Calls @ 1.75

#Earnings – They did “pre-announce” a few weeks ago with nice results. Could be a sell on the news…who knows. Might wake up in the morning and be at 40 or 140…LOL I’m still taking a small shot anyway. This might be a good one to always have a position or two going for awhile.

Sold these as a package for 11.90:

Sold AAOI AUG 11 2017 90.0 Put @ 4.34

Sold AAOI AUG 18 2017 85.0 Put @ 4.09

Sold AAOI AUG 25 2017 80.0 Put @ 3.47

Then, sold all the matching calls in the first week of the ladder:

Sold AAOI AUG 11 2017 115.0 Calls @ 2.00

So what do I want? Less movement the better but can easily mange anything from 75 to 125. Anything bigger than that will be a little more of a hassle. Market maker move for today is about 10.40…

#LongCallDiagonals – Selling next week. Feels like it’s going to be a struggle at 1000 for awhile so selling fairly aggressively.

Bought to Close AMZN AUG 4 2017 1010.0 Call @ .44 (sold for 7.20)

Sold AMZN AUG 11 2017 1000.0 Call @ 7.05

@Iceman tweeted this today. Thought it was pretty interesting so passing it along.

#ShortStrangles – With earnings out of the way it’s back to a more standard position…

Sold REGN SEP 15 2017 425.0/550.0 Strangle @ 6.80

#ShortStrangles – Was currently in a 180/155 inverted strangle. I’ve been rolling and selling and rolling and selling the crap out of this thing for weeks looking forward to next week’s earnings. Kept thinking the 180 puts were so DITM I’d get assigned early at some point. Finally happened last night.

On the opening pop I sold the stock and then on the small drop sold next week’s 177.5 puts. Also rolled the 155 calls to next week’s 160’s @ .05 credit. Ending up with exactly where I was gonna roll to anyway just had to take a detour to get there and made a little in the process.

Now the good news. Even though the position is inverted, the premium sales have been great the last few months.

Heading into earnings (should be exciting). 177.5/160 inverted with 27.75 premium received.

Anything between the strikes is a 10.25 winner. Breakeven is 149.75 to 187.75

#Earnings – Probably a little early on the management but don’t wanna risk it running away from me. It’s a toss up whether the 50 ma holds or not…

Originally sold 285/345 strangle @ 3.00. She gapped up through the 345 so I :

Sold to Open TSLA AUG 4 2017 350.0 Put @ 6.05 (actually sold 340 first then rolled to 350)

What now?

I’m 350/345 inverted @ 9.05 total credit. If we end the week in between the strikes it’s 4.05 winner. Breakeven now is 341 to 354.

#Earnings – Don’t trust this thing at all so even though the position looks extremely safe I’m bailing for a decent winner…

Bought to Close REGN AUG 4 2017 450.0/520.0 Strangle @ .40 (sold for 4.50)

#Earnings – Unfortunately working last 2 days during market hours. Threw a couple orders in ahead of time….filled on these:

TSLA Aug 4th 285/345 Strangle @ 3.00

REGN Aug 4th 450/520 Strangle @ 4.50

Good luck!

#LongCallDiagonals #IRA – Appears to be running out of steam so booking a nice winner and freeing up a sizable chunk of margin.

Sold to Close EWZ JAN 18 2019 30.0 Calls @ 9.50

Bought to Close EWZ JAN 18 2019 25.0/20.0 Bull Put Spreads @ .75

Bought to Close EWZ AUG 18 2017 37.0 Calls @ 1.07

Bought to Close EWZ SEP 15 2017 36.0 Calls @ 2.23

After front month premium factored in, a gain of 1.90 each on a good size chunk of contracts. Will definitely re-load this on a pullback.

#ShortStrangles #ShortPuts #IRA – I wanted a chance to get in. Looks like I got it…

Sold WDC JAN 19 2018 75.0 Put @ 3.95

Sold WDC JAN 19 2018 70.0 Put @ 2.70

And in regular account:

Sold WDC SEP 15 2017 80.0/95.0 Strangle @ 2.90

#FallingKnife? – Been looking to get in this one at some point.

#VXXGame – Only had to go up 8 cents above my standing offer to get filled. Making room for some more sales if we spike a little higher.

Bought to Close UVXY1 JAN 19 2018 25.0/40.0 Bear call spreads @ .38 (sold for 2.70)

#LongCallDiagonals Here we go…jumping back in. Whiz style but instead of buying a DITM call I’m going synthetic stock with a protective put and selling front months against. June 2019 now available so going out as far as possible.

Bought to Open AMZN JUN 21 2019 1000.0 strike #SyntheticStock @ 38.00

Bought to Open AMZN JUN 21 2019 700.0 Put @ 30.00

Sold AMZN AUG 4 2017 1035.0 Call @ 4.15

Net debit of 63.85 so need to average 65 (.65) dollars per week of front month sales to breakeven. May end up going monthlies if we head back up to give more room. Similar trades on AMZN GOOGL GS JPM EWZ and VRX have capped what could’ve been huge gains due to selling front month too closely.

#Earnings Bought to Close AMZN July 28th 1030/1050/1070 #IronButterfly @ 19.50 (sold for 17.90)

Don’t see it recovering today so taking what I can get and cutting max loss by .50

#PerpetualRollingStrangles – With the latest sale I was actually over sold on the put side by 3:1. Showing weakness today so booking the extras…

Bought to Close EWW AUG 11 2017 54.0 Puts @ .11 (sold for .45)

Bought to Close EWW AUG 18 2017 53.0 Puts @ .12 (sold for .91)

#Futures – Short /ES against short puts for basis improvement. I’ve been slightly over writing the puts to keep up with the rise. Taking some off to give ‘er more downside room.

Bought to Close /ES AUG 17 (Wk1) 2450 PUT @ 4.25 (sold for 12.50)

#ShortStrangles – Still aggressively selling against a DITM put.

Bought to Close CMG JUL 28 2017 365.0 Call @ .10 (sold for 10.00 after a roll down into earnings)

Sold CMG AUG 4 2017 355.0 Call @ 2.55 (yesterday)

#PerpetualRollingStrangles – Replacing some Aug 11 and Aug 18 positions that are almost worthless.

Sold EWW SEP 15 2017 55.0 Puts @ .61

#Earnings – Bought 71/74/77 Iron flies @ 1.75 (sold for 2.15)…..small winner

Almost a #PerpetualRollingStrangles position but not really. Just a great stock for premium selling…continuing to sell against ITM calls.

The power of the volatility collapse…even though the stock moved 9 or 10 dollars against my short puts was able to get out of them virtually even. Then was able to go out another week and sell into the drop at lower strikes.

Bought to Close WYNN JUL 28 2017 133.0 Put @ 3.20 (sold for 3.30)

Bought to Close WYNN JUL 28 2017 134.0 Put @ 3.80 (sold for 3.81)

Bought to Close WYNN JUL 28 2017 135.0 Put @ 4.80 (sold for 4.29)

So…lost 40 bucks on those all together. I’ll take it out of this:

Sold WYNN AUG 4 2017 130.0 Puts @ 2.45