Sold $EXAS Jan 12 49 puts @ .80 with the stock at 50.99. Thanks for the idea @thomberg1201.

Recent Updates Page 355

GILD rolled the 4 DTE…

GILD rolled the 4 DTE 72 call to 46 DTE for 1.65 credit. Profitable now so if anywhere in that area at expiration will let it assign to free up some margin.

#Fuzzy Biotechs Big move in…

#Fuzzy Biotechs

Big move in Biotechs this morning after talking about some positions over the weekend–definite pain in EXAS/EXEL/GWPH/CELG. I’ve got two fuzzies in EXAS, one was hedged and DITM, one was unhedged. Luckily my vow to really try to not overtrade these paid off today since I didn’t jump the gun on managing the DITM hedge on EXAS. So I was able to BTC the Jan 12 55 calls for 50% gain (.70 vs 1.35). EXAS pre-announced quarterly earnings, they are presenting this week at the JPM conf, so continued volatility this week is expected.

CELG: I used the AS-BB osc. to cover my hedge for $2300 profit and eventually reset the hedge. BTC Jan 12 107 c for .40 (sold for 2.70), STO Jan12 105c for .76. CELG is now my oldest fuzzy with a total collected hedge now of $4100.00 (yesterday’s report was wrong-cell ranges were missing on my spreadsheet formulas). The synthetic line is $110…so hedging has absolutely saved this position (though it still has net loss). I have collected 1.72 OVER the initial trade debit. Earnings coming up.

QQQ: I shut it down for net $1171 profit. My rolls have been sloppy, I’d like to reset with the tighter put that I’m using now on indexes. In my weekend work, I show QQQ with lagging strength over SPY.

SPY Unhedged Fuzzy: Added Feb 273/273/269 for 2.51 x 15

DIA Unhedged Fuzzy: Added Feb 252/252/248 for 2.17 x 15

SPX closures

#SPXcampaign These closed this morning on GTC orders:

$SPX Jan 12th 2690/2665 put spreads for .25. Sold for 3.20 one Jan 3rd.

$SPX Jan 18th 2620/2595 put spreads for .20. Sold for 1.60 on Dec 22nd.

Upside Warning working… this morning’s minor drop another entry opportunity.

NVDA

#SyntheticStock – Booking this one before it gets away…another one straight up. Maybe an earnings pullback to re-enter. We can hope!

Sold to Close 190/190/185 synthetic @ 67.80

Bought to Close 202.5 short call @ 21.60

Net credit to close of 46.20 plus weekly premium of 2.35 for total credit of 48.55

Entered the trade for 41.00 so a nice little 7.55 gain. Could’ve been better but just went up too fast…

BIDU

#SyntheticStock – Same as BABA but more extreme….giving back a little of the weekly premium I’ve sold but picking up some more upside.

Rolled BIDU JAN 12 2018 237.5 Calls to FEB 23 2018 250.0 Calls @ 2.34 debit.

BABA

#SyntheticStock – I don’t mind things going up but does it always have to be STRAIGHT UP? 🙂 Rolling front month short calls up and out.

Rolled BABA JAN 19 2018 180.0 Calls to BABA FEB 9 2018 185.0 Calls @ .37 debit

#SPXcampain STO SPX 28 FEB…

#SPXcampain STO SPX 28 FEB 18 2620/2520 BuPS @5.10

STO SPY Jan 19 270/268…

STO SPY Jan 19 270/268 Puts .16 BTO SPY Jan 19 273 call total cost 1.47

#shortputs EXAS Sold Jan. 12…

#shortputs EXAS

Sold Jan. 12 49 put for .80

TLT

#PerpetualRollingStrangles – Filled Friday but missed it. This entire position sat inverted for all of 2017 with rarely either side getting taken out. Still made 2.5 times margin required. I’ll keep it going…nice steady theta day after day with little P/L change due to the inversion. 6 contracts each for 4- 5k margin…

Rolled TLT JAN 19 2018 127.0 Puts to TLT FEB 16 2018 127.0 Puts @ .75 credit.

Everything now in Feb monthly. 121/123 calls and 127/130 puts. Showing $40 theta per day for 4500 margin with a delta of +12. How did I decide on the position size? Stress tested it through TOS Analyze tab using TLT at 87 and/or 143. Using it’s most extreme values over the last 10 years the risk was satisfactory considering the annual returns.

ISRG

#ShortStrangles – Earnings not for 2 more weeks but IV still hanging in there this week for some reason. Squeezing the strangle in a little for additional premium. Expires Friday…

Rolled 350 put to 370 for 2.75 credit.

Now sitting at 370/400 @ 8.75

SPX

#RocketManHedge – Core position in March…selling against it.

Bought to Close SPX JAN 10 2018 2700.0 Put @ .35 (sold for 11.70 net after a roll up)

Sold SPX JAN 17 2018 2725.0 Put @ 5.00

SPX more puts sold

#SPXcampaign Earlier sold my standard, 5-week-out, campaign trade (Feb 9th expiry). Here I’m selling an aggressive, ATM, shorter timeframe as it looks like the morning weakness is ending. This one will be on a shorter leash, and if we haven’t moved higher by this Friday I will likely roll it.

Sold $SPX Jan 19th (Friday PM expiration) 2740/2715 put spreads for 6.95.

EXAS

Adding to positions.

STO April 40 puts @1.95

STO July 35 puts @1.90

EXAS

STO April 45 puts @ 3.10

$GPRO

Getting slammed

Announcement…

I’m changing the name of my site to Options Blockchain Bistro-Coin. I’m selling only 100 shares, opening ask is $1.6 million each.

SPX puts sold

#SPXcampaign Sold $SPX Feb 9th 2650/2625 put spreads for 1.60.

Econ Calendar for week of 1/8/18

Be sure to periodically click “Home/REFRESH” to keep Bistro features updated.

#spycraft We are showing a…

We are showing a whopping $9 profit on the adjusted call side of the Jan 12 271 long call 6, 272 short call and 276 call 5 of those. I am going to close mine this morning. This could be the start of a 3 point or 30 point reversal but with only 11 DTE there is not much more time to adjust and now we have a slight profit, if we wait until expiration it will be a $410 loss. The hedge worked, time to take it off and will establish new range tomorrow.

Of course you can stay in if you think we are going higher. I personally will close. We made $255 credit on the IC initially. With the adjustment we are now up $9. Not being greedy, just want to keep most of the initial credit and move on and we have the opportunity at the open to do that.

Earnings Season kicks off on…

Earnings Season kicks off on Friday, 12 Jan with JPM, BLK and WFC.

NOTE: There may be errors and omissions in this list. Please perform your own due diligence and confirm the earnings date BEFORE entering a trade.

+++++++++++++++++++++++++++

Notable Earnings AMC Fri (Last Week)/BMO Mon:

HELE

Notable Earnings AMC Mon/BMO Tues:

AYI, SCHN, SHLM

Notable Earnings AMC Tues/BMO Wed:

LEN, MSM, SNX, SVU, VOXX

Notable Earnings AMC Wed/BMO Thurs:

DAL, FCEL, KBH, PRGS, SJR

Notable Earnings AMC Thurs/BMO Fri:

BLK, JPM, PNC, WFC

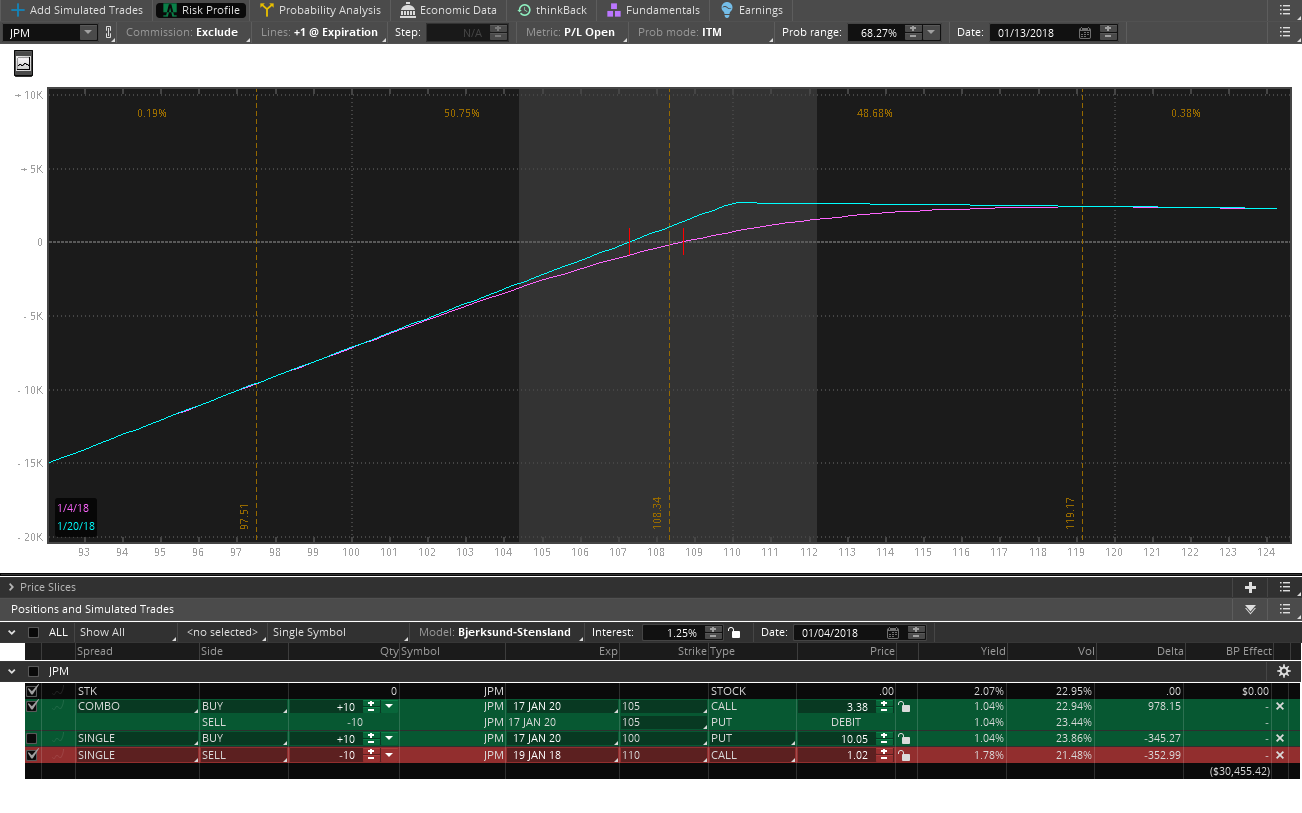

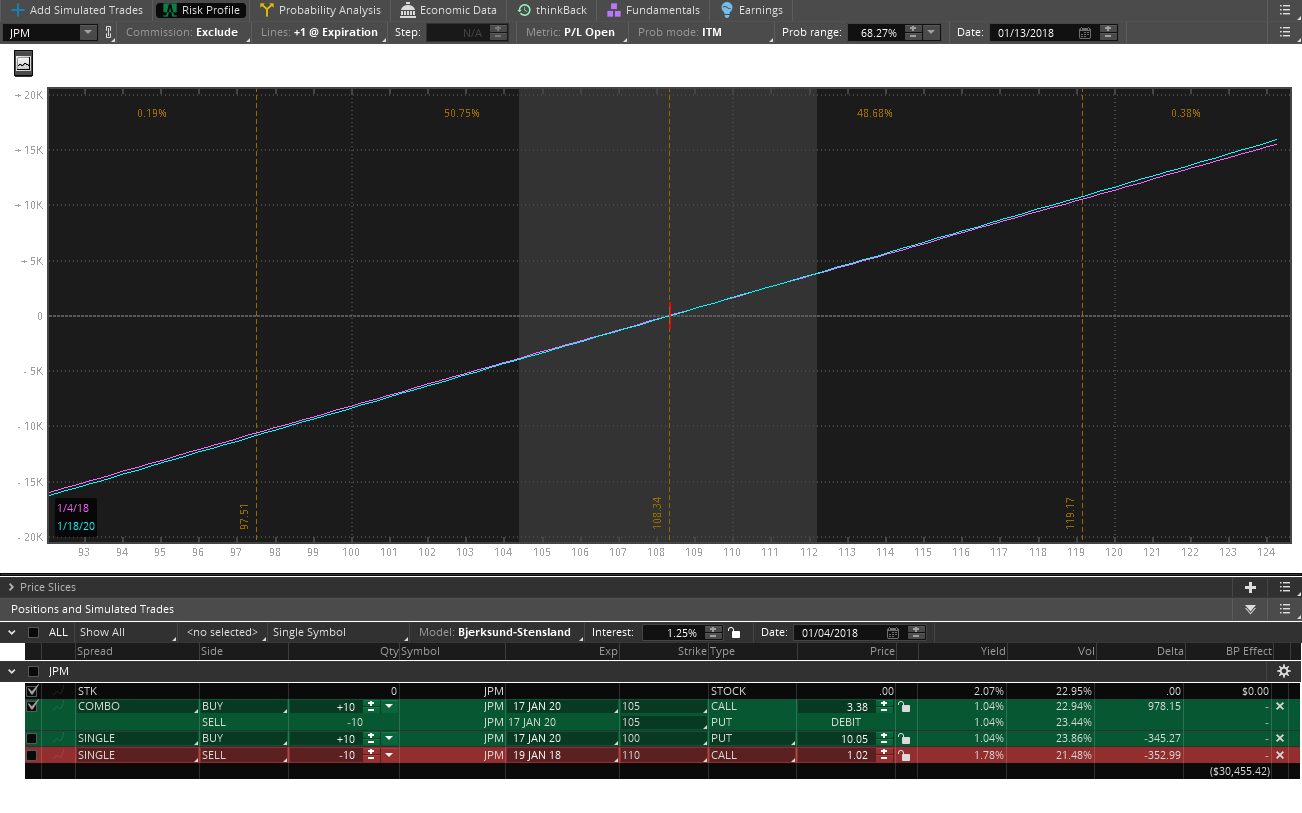

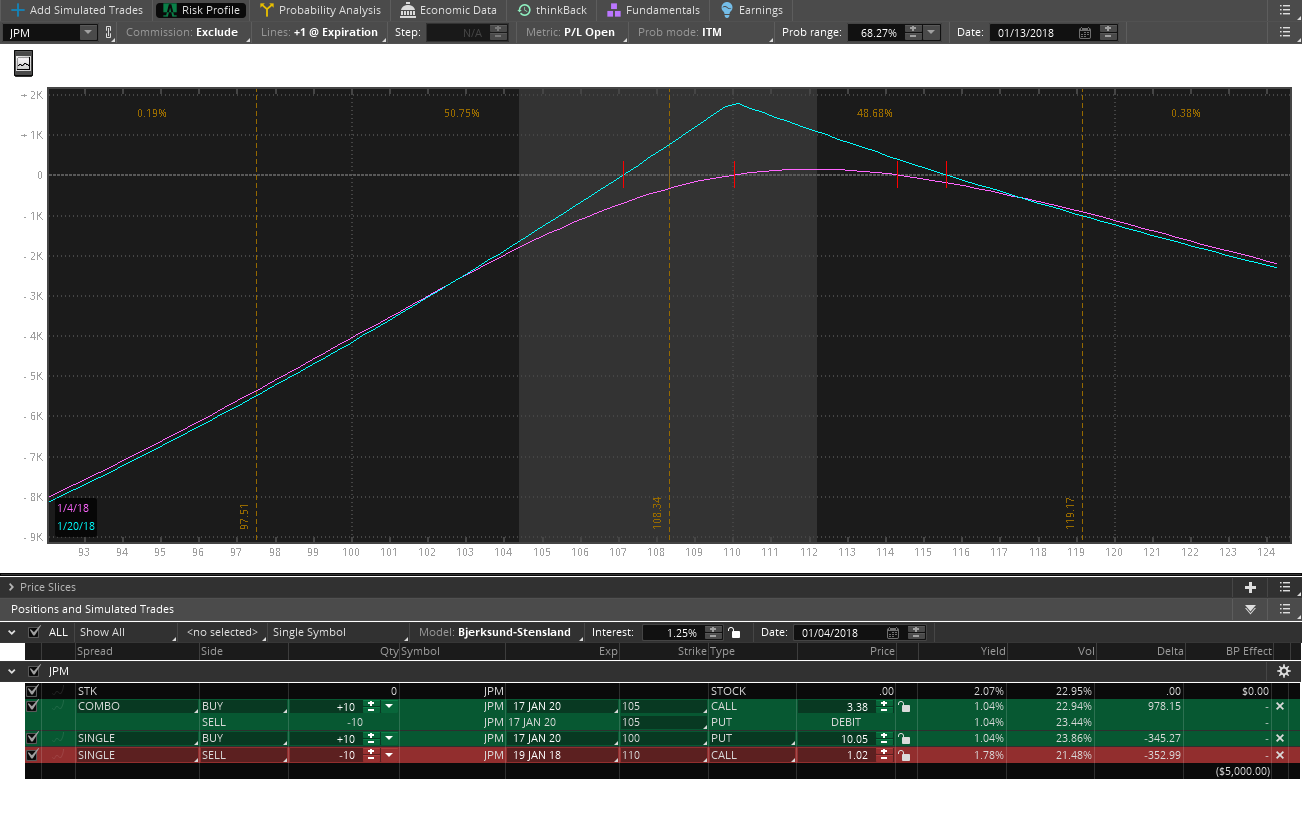

Short post, promise but a…

Short post, promise but a few graphs that will take up some space. JPM as example. First graph is a synthetic long selling a 1 week 110 call without the downside protection. Looks like a regular covered call and it should, it is a synthetic covered call (this is what motley fool does a lot of). Second graph uncapped, looks like buying stock but there is no downside protection so would have to have the cash or margin to buy at the put strike. Third graph is a #fuzzy with 5 point disaster protection put. Looks more like a long calendar spread because of the extra cost of the put protection. That is why you would want to sell weekly or monthly calls against it, to lower the cost basis on the debit of the leap spread and the put protection. I personally would probably go 10 points wide but this shows you could do it in a recently funded IRA for 5000 max risk if JPM is not too big to fail.

I am not recommending this trade but I think @smasty160 has a similar trade running.

Hope that helps for people trying to wrap their head around #fuzzies and learn visually, I know I learn better with a visual.

Sunday nite Open

A nice open on the Futures, as ES and YM both open up nicely…a nice trade start for monday…

#Fuzzy Weekly Report Open Fuzzies…

#Fuzzy Weekly Report

Open Fuzzies (Oldest first)

“Revised Debits” are dropping very slowly due to rollups on hedges.

1. CELG (Mar 110/110/100) Core Debit: 2.38 Net Collected: 1.04 Revised Debit: 1.34 Hedged Jan12

2. RCL (Mar 125/125/115) Core Debit: 3.59 Net collected: 2.36 Revised Debit: 1.23 Hedged Jan12

3. FAS-1 (Apr 70/70/60) Core Debit: 2.08 Net Collected: 1.58 Revised Debit: .50 Hedged Jan12 ITM

4. FAS-2 (Apr 70/70/60) Core Debit: 2.12 Net Collected: 1.57 Revised Debit: .55 Hedged Jan12 ITM

5. LMT-1 (Mar 320/320/310) Core Debit: 6.20 Net Collected: 2.81 Revised Debit: 3.39 Hedged Jan19 ITM

6. LMT-2 (Mar 320/320/310) Core Debit: 6.20 Net Collected: 2.88 Revised Debit: 3.32 Hedged Jan19 ITM

7. QQQ (Apr 158/158/148) Core Debit: 2.73 Net Collected: .96 Revised Debit: 1.77 Hedged Jan19

8. IWM (Mar 151/151/141) Core Debit: 2.25 Net Collected: .57 Revised Debit: 1.68 Hedged Jan12

9. MCD (Mar 170/170/160) Core Debit: 3.12 Net Collected: .79 Revised Debit: 2.33 Hedged Jan19

10. CMCSA (lazy river) (Apr 40/40/35) Core Debit: 1.38 Net Collected: .94 Revised Debit: .44 Hedged Jan 12

11. AAPL (Apr 170/170/160) Core Debit: 5.27 Net Collected: 1.25 Revised Debit: 4.02 Hedged Jan19

12. CVX (Jun 125/125/115) Core Debit: 2.33 Net Collected: .94 Revised Debit: 1.39 Hedged Jan12

13. EXAS (Apr 50/50/45) Core Debit: 6.15 Net Collected: 1.35 Revised Debit: 4.80 Hedged Jan12 ITM

14. MNST (Lazy River) (Jun 60/60/55) Core Debit: 5.13 Net Collected: .50 Revised Debit: 4.63 Hedged Jan12

15. SPY x 4 (4 accts) (Jun 272/272/268) Core Debit: 6.98 Net Collected .58 Revised Debit: 6.40 Hedged Jan17

The total amount of hedges on above, included debit rolls and open hedges is $20,950.00. Almost everything I do is 10-lots.

Unhedged Fuzzies:

EXAS: Apr 50/50/45 @ 6.15 x10

EXEL: May 31/31/27 @ 2.55 x10

GWPH: May 135/135/125 @ 9.65 x 5

SPY: Feb 273/273/269 @2.31 x10

Closed Fuzzies:

LMT: $773 Net

TWTR: $440

NUE: (340)

DWDP: $1500

CSX: $1300

JPM: $3230

BABA: $1560

Synthetic Stock…Repair of Weekly Sales

Scroll to the very bottom for the Cliff’s notes if you’d like… 🙂 🙂

#SyntheticStock #Fuzzy – While criss crossing the country this week I’ve had plenty of time to think about things (besides the mountains around Eagle CO and the cyclone in NYC…LOL)

I’ve got a couple synthetic long positions where the weekly call sale has gone ITM. Not surprising in this market but still annoying. Most of the trades are still profitable but it’s more fun when they are REALLY profitable. So…what can I do once they’re so DITM that rolling up and out becomes nearly impossible?

I’m going to use my most extreme example here…

Currently holding AMZN Jun 2019 synthetic short at 1050. It started out as 1000 synthetic but I rolled up a couple months ago to bring a little cash back in. For quite awhile I was selling weekly calls around the 950 to 1000 level while AMZN chopped around down there. They then had an earnings surprise and stock took off and hasn’t stopped since.

My current short call is Jan 2018 monthly at 1010. Obviously DITM so what can I do?

When looking at the overall position and imagining this at expiration, my profit is capped at the level of the short call so the goal is to get that as high as possible.

My plan is to roll the synthetic up to a level I’m comfortable with as far as AMZN support goes. Then…take the credit and use it to roll the ITM short call up. This accomplishes two things. First, the call can be rolled for around even and up a slightly greater distance than the synthetic moves up. Secondly, the short call becomes less DITM so it becomes more rollable in the future (that’s the most important thing I think).

So…what’s the risk? An AMZN implosion is the risk…LOL. For now I’m not rolling up the disaster put since the DITM short call actually provides a nice hedge of it’s own on pullbacks. If the short call were to become out of the money then that might be a signal to ease the disaster put up. Until then, I’m not wasting cash on it.

Hopefully I’ve explained this ok. Other than the free fall of the stock, are there other risks I’m not seeing or considering? It seems to be a reasonable shot at capturing further upside with limited risk increase. I haven’t run the numbers yet on cheaper stocks but looking at VRX now…

Long story short…roll up the synthetic and use the credit to roll up the DITM call IF and only IF you’re confident in the stock holding it’s upside move.

TQQQ

If we ever get a correction I want to put on this trade.

buy 2020 80 call

sell 2020 80 put

buy 2020 75 put

sell the weekly or monthly call. I figure that I would need .89 cents a week to pay for the trade.

Unhedged #Fuzzy (this is really…

Unhedged #Fuzzy (this is really long!!)

My good friend @MamaCash calls these “Unhinged Fuzzies” and that always makes me smile. Over the past couple of weeks, the power of these revealed itself to me. So that’s why I called Mr @fuzzballl an onion last night 🙂 These fuzzies are revealing very important layers of opportunity to apply in different circumstances.

Yesterday morning I woke up remembering one of John Carter’s classes from a few years ago where he talked about “HPTM” High Probability Moments in Time. Couple that with Jeff’s upside VIX warning and Eureka! HPTM is here. My immediate thought was “put down all the toys.” No more 2-lot 3-lot 5-lots on various tickers. Time for BIG laser focus on SPY/SPX RIGHT NOW. However long this window lasts this is when fortunes are made.

Before I talk more about yesterday though, let me give a couple-paragraph primer on unhedged fuzzies, because I know some people are following this carefully. And when the check-out girl at the grocery store this weekend asks you “why not just buy calls instead of a fuzzy,” here’s your answer:

100 shares of stock = 100 Delta (P/L moves 1:1 with stock, it is stock)

1 At-the-Money call = 100 shares of stock = 50 Delta (only moves 1/2 with stock)

(1 ATM Call) + (- 1 ATM Put) = 100 Delta—this is a synthetic long stock position with 100 delta

A synthetic stock position is a very cheap way to approximate ownership of stock, but there’s not a huge advantage in it. In a 401K you still are required to hold the full buying power risk of the naked puts, in margin accounts there is some buying power reduction on the naked puts. But note that you have a large naked put position with synthetic stock.

SPY 1000 Shares: $273,000

SPY 10-lot synthetic naked put risk: $273,000 (indulge me in being less than precise)

Buying Power required: $273,000

Enter the 3rd leg of the Unhedged Fuzzy: The Protective Put

This is done in the same expiration cycle as the synthetic, in fact on the same order (hold your control key to add the leg). Currently I’m using $4.00 spread-risk on SPY. Here’s what my orders look like:

BTO 273 Call

STO 273 Put

BTO 269 Put

What just happened? All of this is on a 10-lot:

Risk: $4,000 (+ trade cost) vs $273,000

Income: UNLIMITED 700 delta ($700 for every $1.00 move in SPY (vs $500 for ATM calls))

Buying Power: FREE for portfolio margin, $4,000 for IRA vs $273,000

Let me give you a real example of how I recently used this trade that I’ve not yet reported. I really like the Gorilla Trades service. I’ve been a subscriber for probably 10 years. If I’d been a faithful follower I’d probably have $25 Million by now, but I’ve not been a faithful follower. Last weekend they came out with their top 3 picks for 2018, all 3 biotechs, all 3 are take out candidates for 2018: EXAS, EXEL, GWPH. All 3 look awesome to me! Do I want to buy 1000 shares of each and just sit on them for 6 months waiting for a buyout that may or may not come? Some of these have very high vol, meaning the market thinks they are either zoom or doom stocks. Do I want to risk 1000 shares on doom? Enter the unhedged fuzzy. Here were my Tue trades:

EXAS July 55/55/45 for 3.56 x 10 (this position is up $2,740)

EXEL May 31/31/27 for 2.55 x10 (this position is up $150.00)

GWPH May 135/135/125 for 9.65 x 5 (this position is down $1175.00 but only because of weekend b/a spread, it’s been up and down )

Point is….I have nice positions tucked away on 3 biotechs using very small risk and buying power….any one of these 3 could bring in a $40K windfall (or more), but if it doesn’t, what is my risk? I’m not sitting on thousands of shares of speculative stock. EXAS I’m most comfortable with, their product is amazing, so I took bigger risk there with a $10 wide protective put (they present at the big health conf this next week). EXEL I’m less familiar with, less risk. GWPH, less risk with less size.

Alright, back to yesterday morning. Woke up, big opportunity still in the markets. But its Friday, we’ve breached key expected move targets (not just for 1 week but 2 weeks). Still I removed hedges from 40 SPY fuzzies that I had, I added 30 Feb SPY Fuzzies for about 2.30. That gave me 70 SPY Fuzzies. 70x $272 x 100 = $1,904,000. Buying power used, next to nothing. Risk: $28,000 + trade cost. I still have a hard time believing the power of this myself. I rode this to the sign of resistance around 2 hours before the close, it was pretty quiet for most of the day. Grabbed about .50 of SPY move = $3500. Then I closed the extra 30 fuzzies and put fresh hedges on the other 40. When resistance broke and we had strength into the close I added another 10 unhedged fuzzies on for Monday morning. So I’m currently sitting on 40 hedged, 10 unhedged. My intent was to keep these trades open longer, but I tend to be a nervous nelly on Fridays. However, this is a tool I plan to use over and over; shorter duration expiries on limited trend trades, longer duration (hedged) on income trades.

This is really long, I know, thank you if you’ve made it this far. These trades, with their limited risk and effective use of buying power, are showing great versatility for trending/contraction/income/momo/long/short/hedge/speculation opportunities. Hope this was helpful for those of you still getting the #fuzzy concepts.

Sue

Jan 5, 2018

Fractured Focus Today

I heard this is the best trading week since sometime in 2006? This is also the week 5 sheriff deputies were shot in my (almost) backyard. Fractured focus today as I left trading behind to try to honor the victim just a little. I’m happy to live in a community of many people who felt the same way.

I’ll post more tomorrow….especially about the power of unhedged Fuzzies. This morning, I found myself with $1.9M in SPY power, with only $63K at risk. Oh @fuzzballl You are like an onion of opportunity!

Sue

(

Late Fill Roll SVXY Calls

#rolling

$SVXY BTC 1/19 75 call @ 60.96 STO 3/16 80 call @ 58.20 Might be delaying the inevitable. Duh

OptionsExpiration

Might be my smallest expiration in years

$C $72 puts

$RCL $124 #coveredcalls

No $SVXY, $UVXY or $VXX expirations this week

Running pretty low on short option positions.

Expiration

$SPX 2500/2525 BUPS STO 12/5 for 1.45 Thank you @jeffcp66

$NFLX 205 call (Twas covered – what’s five points among friends) Still profit was made on stock as well

Have a great weekend. Those of us needing warmth – layer up.

Expirations

Only 4 today but I have a big one on the 19th.

SVXY 60 puts

SVXY 65 puts

SVXY 70 puts

SVXY 75 puts

Short Puts OLED EXAS

#shortputs

$OLED STO 2/16 169/170 BUPS @ 2.55

$EXAS STO 1/19 55 Put @ 1.95

BTC SPX 16 FEB 18…

BTC SPX 16 FEB 18 2605/2505 BuPS @3.25 Sold on 2 JAN 2018 for $5.00

BOT SPX 16 FEB 18…

BTC SPX 16 FEB 18 2595/2495 BuPS @2.90 Sold on 1 JAN 2018 for $5.70

JCI, STZ

STO JCI, July 33 puts @.85

STO STZ, April 200 put On 1 contract @ 3.20

MYL

Roll MYL Jan05’18 43 calls to MYL Jan19’18 43.5 calls for 0.07 credit. I had a hard time getting this order in, Interactive Brokers is having some sort of an issue with their site. Earnings for MYL coming up supposedly on 02/05/18.

SVXY roll

#VXXGame Doing a @fuzzballl style #ReverseRoll on this one. My naked call was bound for #EarlyAssignment any day now so I finally closed it. Getting some of that premium back with an ITM put spread. If we have a significant drop before June, I can sell the long put and take assignment of the stock at a decent cost basis.

Closed $SVXY Jan 16th 97.5 call for 38.35. Sold as the 195 call for 6.25 on 1/6/17, exactly a year ago…. cost basis 3.125, so not a great trade!

Sold SVXY June 150/110 put spread for 18.40. So for instance if SVXY dips to 80 at June expiration, I would get the stock at 101.60 cost basis. I’ll be looking for another roll on the next pullback.

SPX Campaign / Long Calls WUBA / Short Puts BA

#spxcampaign

$SPX STO 1/17 2705/2730 BUPS @ 6.25 Thank you @jeffcp66

$SPX STO 2/2 2635/2660 BUPS @ 1.55 Ditto

#longcalls

$WUBA BTO 2/16 75/85 BUCS @ 5.00

#shortputs

$BA STO 2/16 280/290 BUPS @ 2.15

AMZN covered call roll

Rolled $AMZN Feb 16 1220 call up and out to Apr 20 1260 call for 1.19 credit. Getting another 40 points of room to the upside.

Bespoke’s List of the Most Volatile Stocks on Earnings

#Earnings https://www.bespokepremium.com/think-big-blog/bespokes-list-of-the-most-volatile-stocks-on-earnings-2/

SPX trades

#SPXcampaign Here are the $SPX trades I made on the Great Market Dip of 2018 (the 3-point drop between 9:30 and 9:55 PT)

Sold Feb 2nd 2660/2635 put spreads for 1.55

Sold Jan 17th 2730/2705 put spreads for 6.50

BOUGHT Jan 16th 2750/2770 call spreads for 2.80

COST

BTC January 19, 125 puts @ .01two weeks early. Sold @1.15

BTC 3x EXPR 118/116 Jan…

BTC 3x EXPR 118/116 Jan 12 .05 profit after comm 63.00 4 days, still have 1 expiring today

$UVXY

#VXXGame

OK, I got bored. Entered this defined risk trade based on upside warning and potential continued decline in $UVXY

STO Jan 12 $UVXY $8/$9.50 call spreads @ $0.74

Doesn’t take much of a drop for this to be profitable

Closed Early

$COST BTC 1/19 203/195 BECS @ .40 STO @ 1.11 62% of available profit

AVGO call added

#ShortStrangles Sold another $AVGO Feb 16th 290 call for 3.75. Why do I get the feeling I will have to roll it?

STZ

STO July 190 put @ 3.30

$SVXY

Morning Before I get drug off the the other gig I sold some Jan 19th and Jan 26th 120 Puts yesterday and today. Hope everyone is safe and warm.

SPX trade

#SPXcampaign I was futzing around with taking some risk off yesterday, but was not filled. Then I forgot to take the order off, so this closed overnight, regretfully now that it’s trading at .60.

Closed $SPX Jan 8th 2710/2685 put spreads for 1.40. Sold for 6.20 on Wednesday.

December Jobs Report

+148,000 non-farm payroll jobs, vs 180K expected

Unemployment holds steady at 4.1%

U6 unemployment up one tenth to 8.1%

Wages up 0.3%, totaling +2.5% for the year

Labor force participation holds at 62.7%

Upside Warning in effect

#VIXIndicator #Market An Upside Warning went into effect, meaning the risk is to upside: higher prices on the indices. I was hoping for some relaxation or minor pullback to start us off, but we are over 8 points higher again on $SPX. No use fighting it.

Jobs report in 20 minutes.

Long Calls XLU CRM

#longcalls

$XLU BTO 3/16/2018 52/54 BUCS @ .74

$CRM BTO 2/16 105/115 BUCS @ 3.50

#shortputs AXDX Sold Jan. 19,…

#shortputs AXDX

Sold Jan. 19, 30 put for 1.90, stock is at 29, plan to own it.

#spycraft Closing out the put…

Closing out the put side of the Jan 19 IC at 260/256. Currently going for 0.03. Removes a lot of the downside risk and if we get above 275 will have decent profit on the call side now. Max risk to downside with the puts closed is now $1110 on 5 contracts plus the 6 longs from this morning. If we start pulling back will close the long while it is still worth something then handle the short call spread like a regular credit spread.

Going out to play in our 11 inches of snow now!

Jan 4 #Fuzzy All Fuzzies…

Jan 4 #Fuzzy

All Fuzzies are managed for the week and new ones added, including a new category I call “Lazy River Fuzzies.” I mentioned a couple weeks ago that I was scanning stocks with a weekly ATR of less than 2 in an effort to avoid a lot of the debit roll/chasing drama. My single test, CMCSA, has worked great, so added a second one today, MNST. The Lazy Rivers are cheaper to put on, have less hedge premium (lower volatility), but hopefully are more “set and forget.” I did a successful round of SPY naked put #Bitty this week….but you know…..I think fuzzies are better than bitties, so instead of setting new SPY Bitties, I have set SPY Fuzzies in all my accounts.

1. CSX Closed Down for net $1300…lots of debit rolls on this and earnings next week. It was a great #fallingknife suggestion

2. LMT-1 Debit Roll BTC Jan 5 322.5 for 2.15 STO Jan 18 325 c for 2.51

3. LMT-2 ditto

4. JPM Closed Down for net $3230.00. This was my very first Fuzzy! Earnings next week. Will reset after earnings release.

5. IWM BTC Jan 5 154 c for .96, STO Jan 12 155 c for .89

6. CMCSA (Lazy River) BTC Jan 5 41 c for .07, STO Jan 12 40.5c for .45

7. MCD BTC Jan 5 172.5 c for 1.50, STO Jan 19 175 c for 1.22

New Fuzzies:

1. EXAS (earlier this week) Apr 50/50/45 for 6.15 Jan 12 55 c -1.35 (ITM now)

2. SPY 1, 2, 3, 4 Jun 272/272/268 7.00 Jan 12 273 -.61 (going tighter on these puts)

3. MNST (Lazy River) Jun 60/60/55 5.13 Jan 12 64c -.50

I’ll do a stats recap tomorrow. A huge amount of fuzzies this week were debit rolls, so basis reduction is moving down ever so slowly, but unrealized profits with the purchase of upside allowance had added up nicely.

DGX GIS NVDA

#IRA #ShortPuts – Freeing up some margin in the IRA. With earnings season cranking up hopefully get a chance for some more #FallingKnife trades…

Bought to Close DGX May 18 2018 80.0 Put .52 (sold for 2.20)

Bought to Close GIS Apr 20 2018 47.5 Puts @ .25 (sold for 1.62)

Bought to Close NVDA MAR 16 2018 150.0 Put @ .41 (sold for 3.69)

WDC

#ShortPuts #IRA – Going back into this one…

Sold WDC APR 20 2018 75.0 Put @ 2.80

Sold WDC APR 20 2018 72.5 Put @ 2.10

Sold WDC APR 20 2018 70.0 Put @ 1.55

$RCL

#Coveredcall

Stock looking weak today, likely because of the big storm on the east coast, probably stay weak into next week.

STO $RCL Jan 19 $124 call @ $1.35, early replacement of $124 call expiring tomorrow.

Blizzard of trades

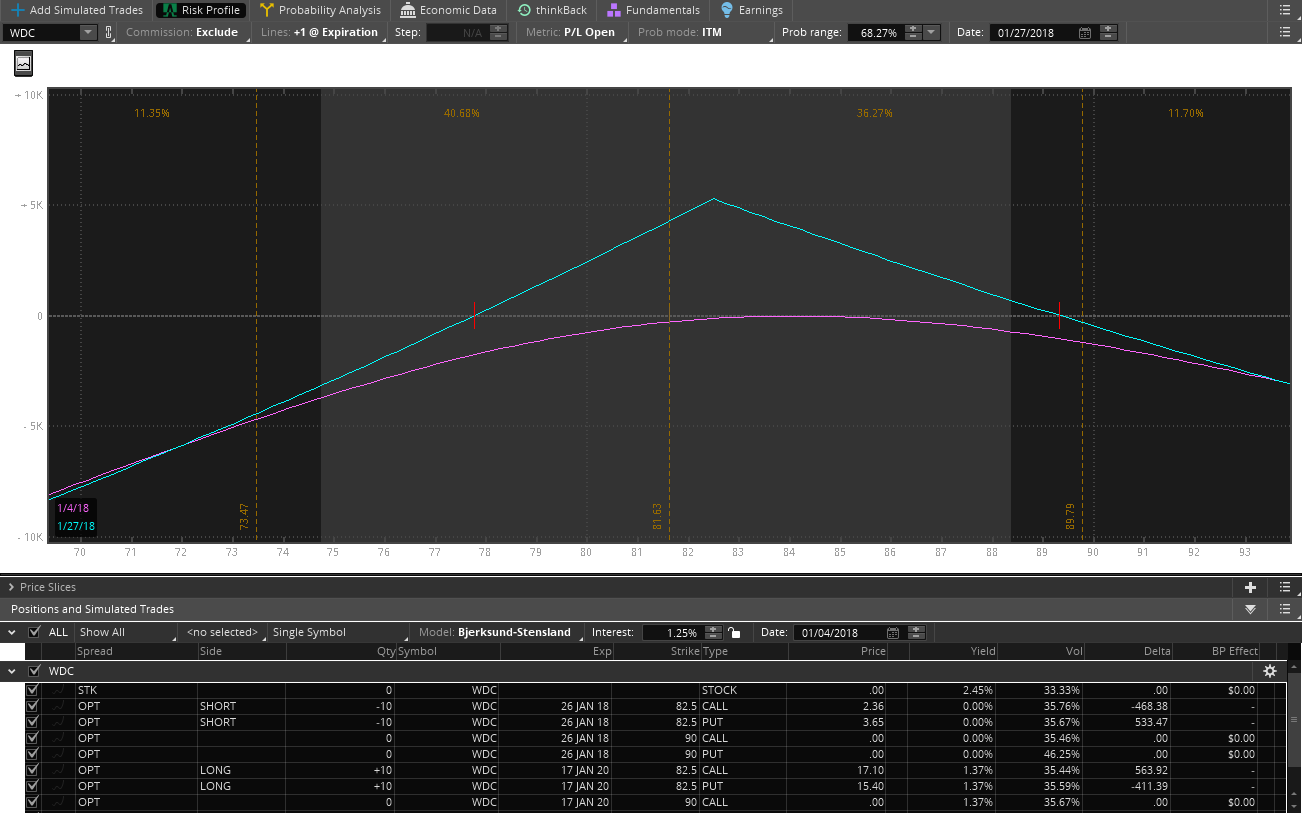

WDC has been in a new range. This is still an earnings trade I have been adjusting since last earnings drop. I am up overall on the trade, but the hedging/theta was not keeping up with the drop so went old school calendar adjustment. Rolled the long 743 DTE 90 straddle down to 82.5 for overall credit of 1.5.

Then rolled the short straddle 22 DTE 90 down to 82.5. This is a roll into earnings so good premium. Debit of 4.24 but still against my accumulated rolls of 18.27 credits. Just keeping the cash machine alive for a little longer. Here is the new profit graph as long as we stay in the new trading range of 77-85 or so. Still have 106 weeks to sell against it and no margin requirements now, that is the main reason I tweaked it and to get extra theta burn.

$C

STO Jan 19 $72.5 puts @ $0.35

Short Puts INTC / Closed Early ADBE

#shortputs

$INTC STO 2/16 40/44 BUPS @ 1.13

Closed Early

$ADBE BTC 1/19 150/165 BUPS @ .10 STO @ 1.00

$SMG

OK, file this under better lucky than good. I wanted to buy some $SMG stock on a pull back so had a GTC order sitting there at $103.25. Down draft this morning took it to $103 and bounced, back above $107 now.

#fallingknife KHC Oct 5, sold…

#fallingknife KHC

Oct 5, sold a Jan.19 72.50 put for 1.13, closed today for .05 (autotrade) thanks Iceman

SPX

#RocketManHedge – This was the first one I tried as an experiment. Went synthetic short for this one using Jan monthly. Never moved in my favor from the very first day. Just closed the synthetic short position at max loss of 50 points. But…weekly put sales brought in a surprising 56.3 points.

Completely out of it now with a 6.30 winner. Similar trade in March that will hopefully turn out ok. It hasn’t exactly been moving in my favor either…LOL

DWDP

I just closed an unhedged #Fuzzy in DWDP that I followed @smasty160 on on 12/27/17, made $1.69! Thanks Sue! Thought about just selling half and letting the rest ride, but since we have the jobs number tomorrow and also because the market has been having a love affair with the sky this week I decided to close it all down.

Still in SPX 2750/2775 Jan…

Still in SPX 2750/2775 Jan 12, Thx Jeff

#dividends T Research showing better…

#dividends T

Research showing better to buy T after dividends than ahead of dividends to capture the dividend.

https://seekingalpha.com/article/4135036-t-can-earn-income-forfeiting-next-dividend?ifp=0&utoken=411b0cb2f22d708fa1ffa7378685662d

NUGT

#SyntheticShort – Out most of yesterday afternoon and late into the night. Managed to beat the cyclone into JFK. Get me back to Florida please! Just a beautiful day here. Had a fill yesterday adding to NUGT short and closed front month short puts this morning.

Added Jan 2019 32/32/34 synthetic short/disaster calls @ 9.40 (previously 10.08 at same strikes)

Bought to Close NUGT JAN 5 2018 29.5 Puts @ .03 (sold for .36)

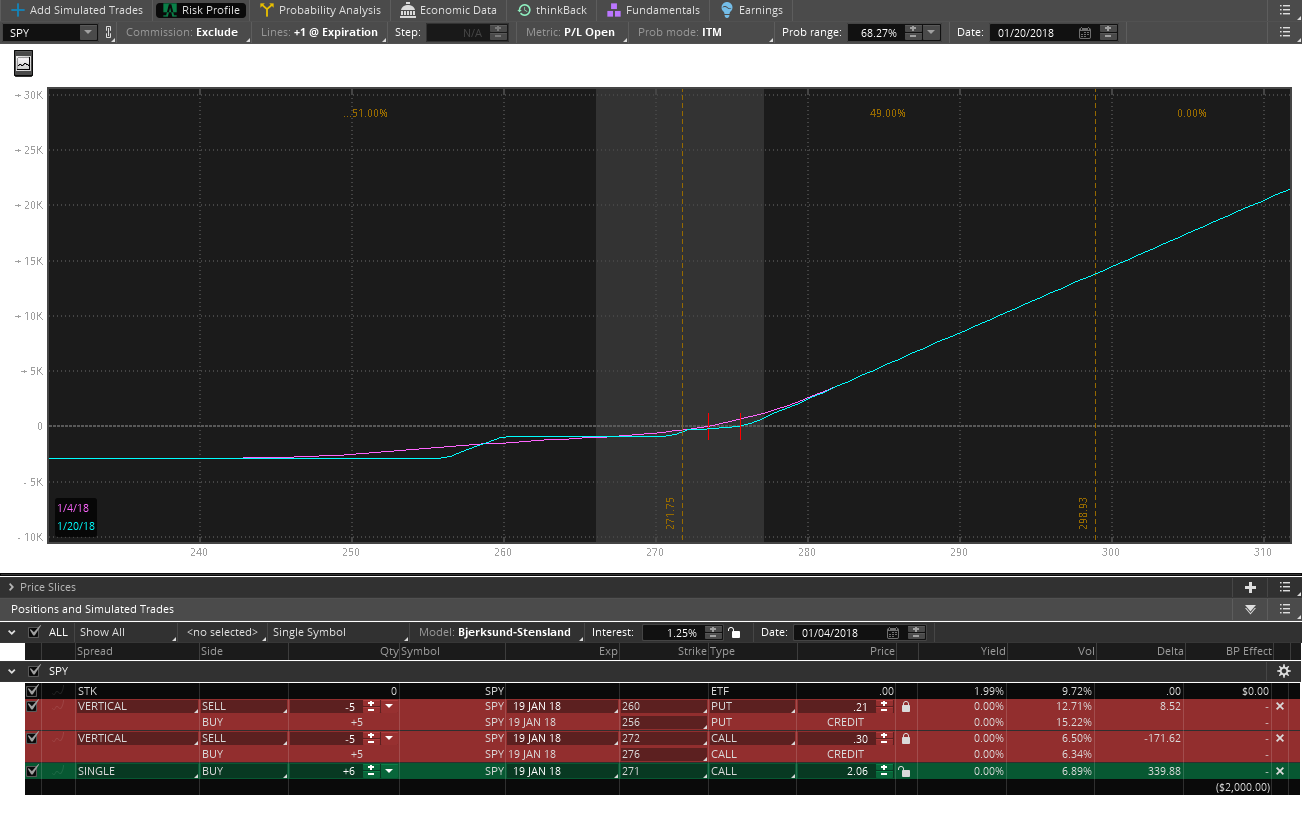

#spycraft Taking @jeffcp66 recommendation. Just…

Taking @jeffcp66 recommendation. Just bought 6 Jan 19 271 calls. Original position was 5 IC at 272/276 on the call side. With the market going into booster phase again makes sense to go directional.

If we get above 273 will start making a little money as long as we close before expiration. If we wait too long and it does not get above 275 then we will lose about the same as we made and would be a scratch. Original position made $255, will lose 275 to 170 between 273 and 275. Above that a nice gain.

STZ earnings

#Earnings Bullish trend, stellar earnings performance.

Sold $STZ Jan 19th 220 put for 2.20. Will add another.

One day moves: Biggest UP move: 6.4%, Biggest DOWN move: -7.1%, Average move: 3.8%. +2.6% upside bias. This trade is -3.9% OTM.

Over last 12 reports, -7.1% was its only move down the day after, and that improved to only -2.7% thirteen days later (which is roughly expiration).

#spxstrategy btc on gtc SPY…

btc on gtc SPY put 26 JAN 18 265/260 PUT @.24 had sold for .59

50% return sto on 12.29.17

SPX calls closed

#SPXcampaign Closed $SPX Jan 18th (monthlys) 2750/2775 call spreads for 2.15. Sold for 1.60.

That puts me 100% long SPX.

strangling AVGO

#ShortStrangles Sold $AVGO Feb 16th 290 call for 3.25.

Sold (2) 250 puts for 5.85 last week… now making this a strangle. Will add another 290 at a higher price to balance the quantity.