AAL covered call in small account. Feb 2 CC at 52.5, just 2 contracts. Debit of 50.91. Making some money on @fuzzballl company.

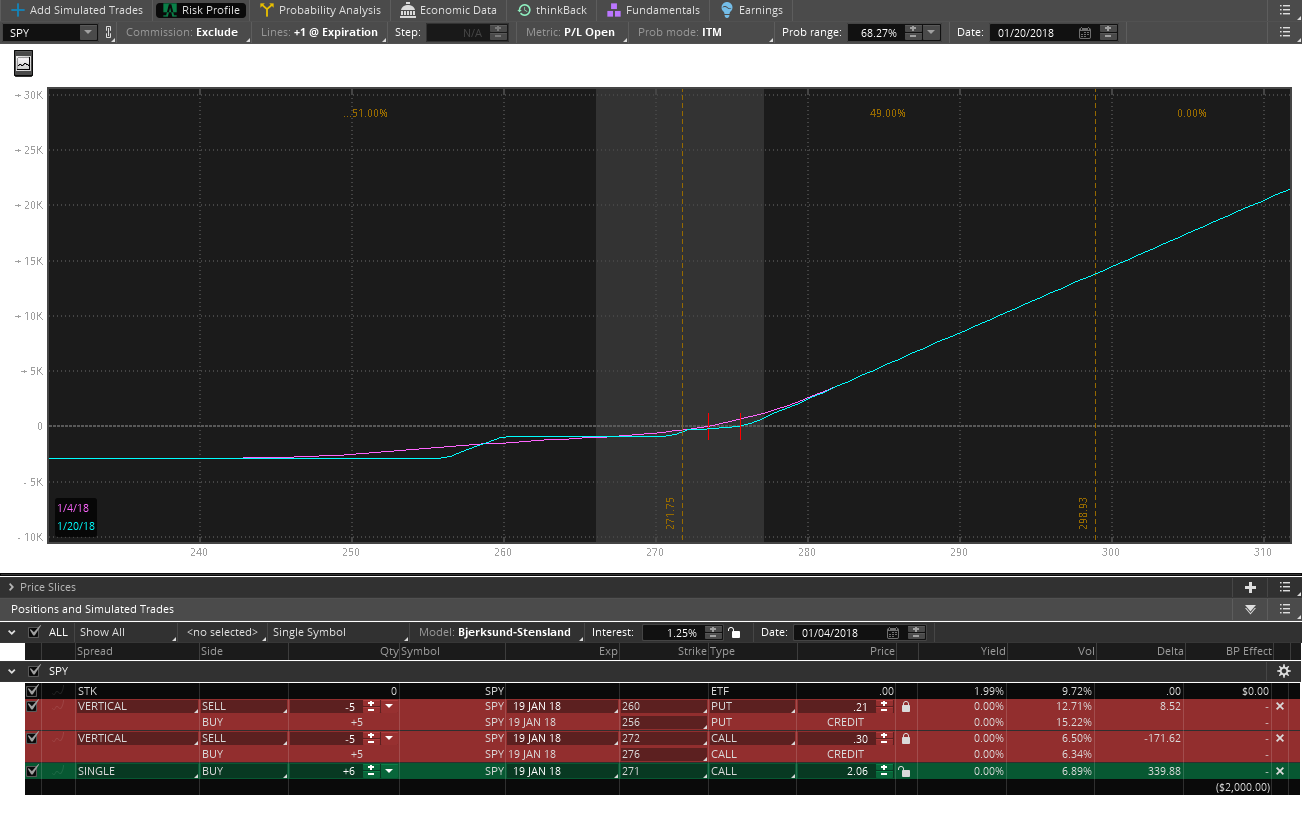

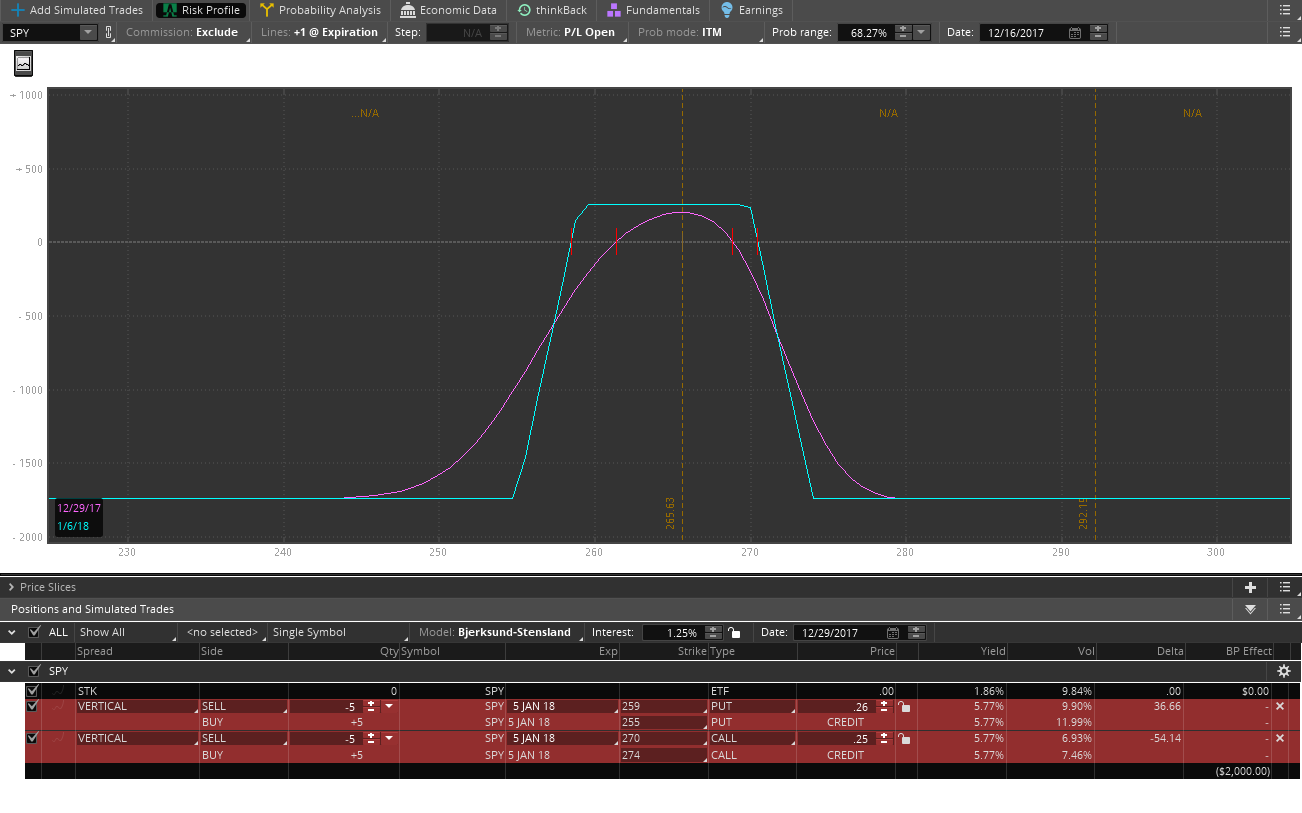

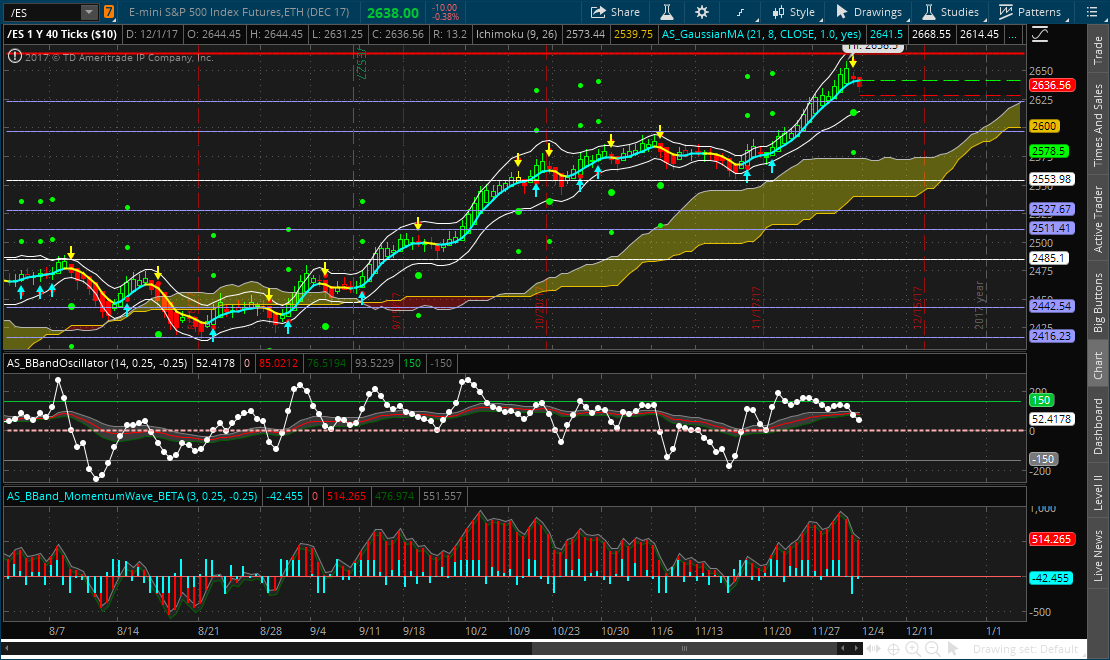

#spycraft update. For those still in the trade you should be making good $ now. I closed out yesterday at a 125 loss on 5 contracts. With the vix being so low and the parabolic market at the moment (i thought the new years goofy juice would have run out by now) I am going to hold off on additional trades at least until we have a pause, a slight pull back, some volatility or at least not a 1 sided parabolic move. I think any short strike in SPY right now is going to exceed the expected move (probably to the upside) and just require a bunch of adjustments.

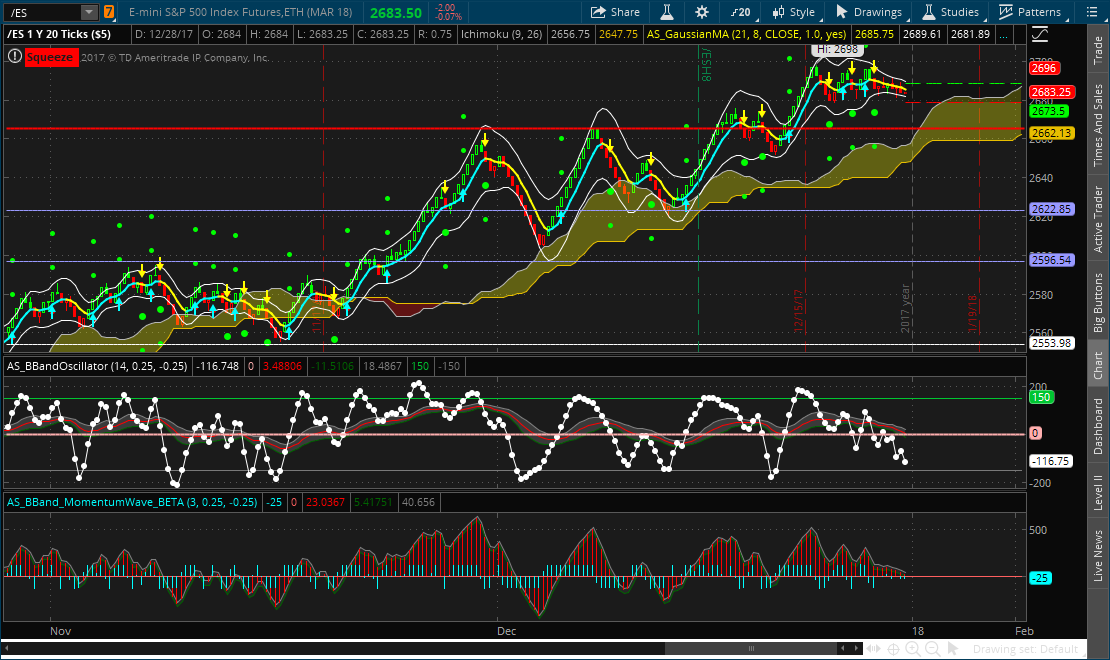

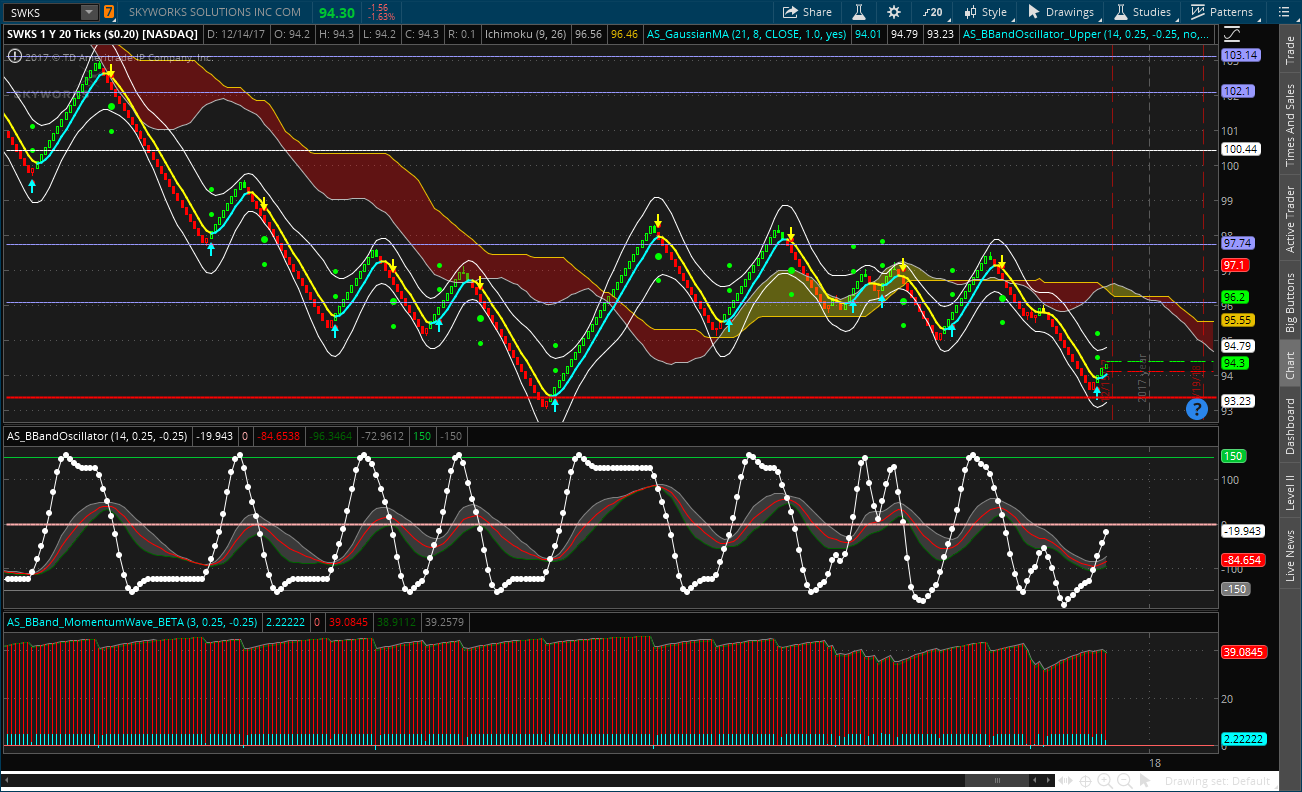

I want to make money, don’t need to be right but the risk is not worth the reward at the moment on credit spreads and IC on SPY or any of the other indexes. I will find an edge in individual names until the volatility returns and earnings will help that. Even a vix of 12 would be appreciated at the moment!! Is that asking too much?