Since we are on experiment discussion below again, here is one I have been paper trading. A twist on #pietrades. If we need a new term we could call them #lizardpies.

So obviously with the market rout all my #pietrades went ITM and to prevent a meltdown in margin I converted them all to #fuzzy. Which is great, has controlled the volatility and still have 111 weeks to manage them. But as @fuzzballl points out below, they are expensive. Cheaper than stock but my EXPE puts are now trading at 22.40 and 19.50. Not chump change.

The #pietrade idea is sound for income generation and even some capital gains long term as long as you sell the call ATM or OTM once assigned the stock. You also are typically only selling 1 side and as Karen the supertrader (now scam artist) figured out, selling the other side is what really improves long term returns and consistency. She may have been using some creative accounting but the idea is sound and has been proven by tasty trade.

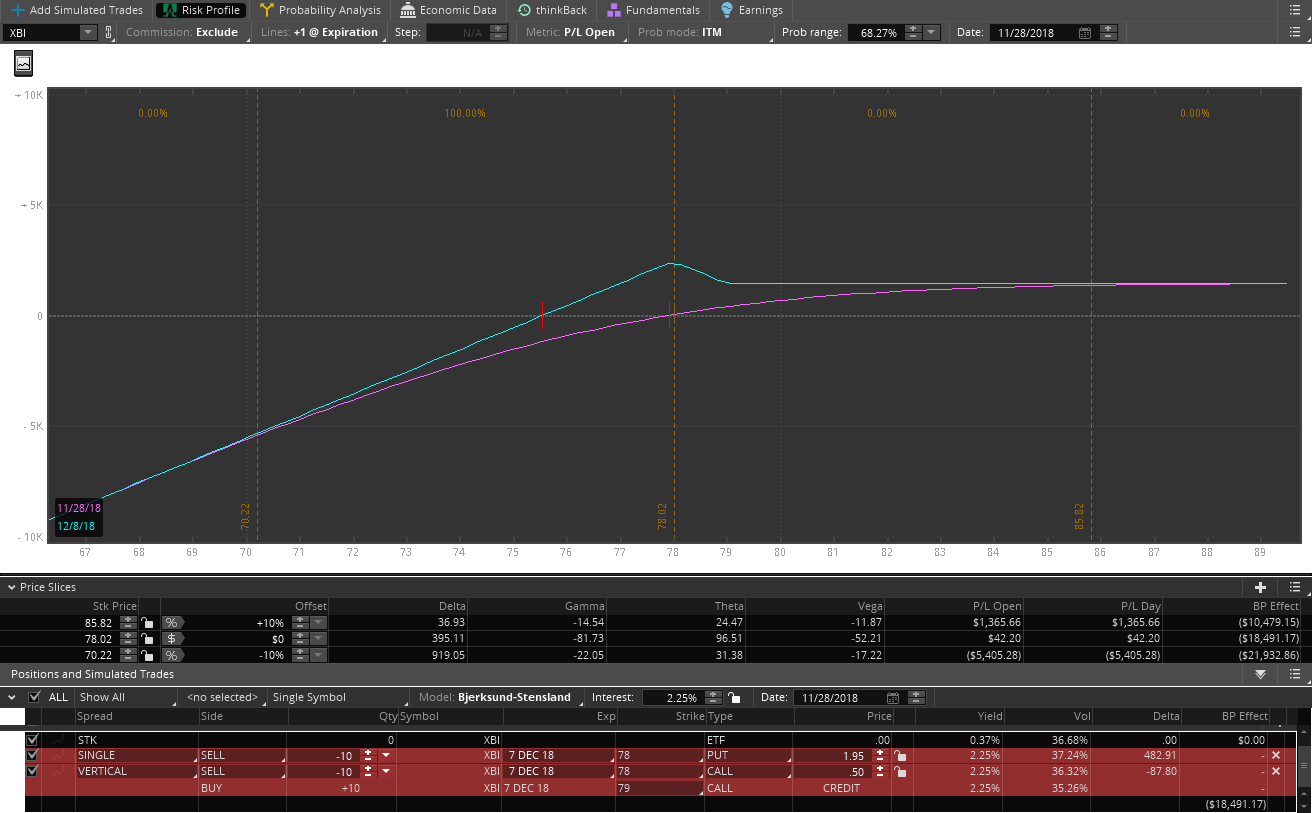

So here is the tweak I have been playing with. When you set up the trade, start it as a #jadelizard but set it up ATM. For example with XBI currently at 78.02 I would sell the 10 DTE 78 puts naked (cash secure) and then sell the 78/79 call credit spread. Total credit 2.55. No upside risk, downside break even is 75.55 which is lower than where I probably would have just sold the put.

3 possible outcomes

a: below 78 assigned shares on the put at 78 but cost basis 75.55. Can sell a next week call or call credit spread if you think rebound, then uncapped upside

b: Between the strikes max profit and you may be assigned on the call but can exercise your long call if needed.

c: above 79 everything cancels out and you keep the credit minus $1.

Here’s a graph on a 10 lot.

I have been trading it on paper and it would have had better loss control on the #pietrades than straight put sales the last 2 months.

Thoughts, holes in the strategy, other ideas to tweak it or make it better? If you wanted to be more conservative could sell strangles OTM instead or straddles ATM on the short sides but then less credit. Since my premise is income, I am trying to bring in as much credit as possible on the front end.