#Earnings Expiring: $SPLK Nov 30th 102/107/109 #BrokenWingButterfly, for a 3.00 credit at Exercise. Bought for 1.60 yesterday. I was trying to close for 3.05 or more, but wasn’t possible after stock moved above 110 and didn’t come back. My broker charges little to none for exercising ITM spreads.

Monthly Archives: November 2018

Good night

Have a nice weekend to everyone. I can’t wait until Monday.

SVXY-still chipping away at these

My 51 covered calls will expire today. They were sold at a net of .475 cents. If we get a big rally on Monday, I can sell them again.

SPX 1-dte

#SPXcampaign My condor for today, Nov 30th 2690/2710/2810/2830, is expiring (sold for .90). I wasn’t planning on doing one for Monday due to the chance for a huge gap on the China talks. However, IV is so high, that I was able to sell a very wide condor. My short strikes have been around 100 points apart in this last week. For Monday’s condor, they are 210 apart.

Sold $SPX Dec 3rd 2620/2640-2850/2870 condors for .95.

Short strikes are 115 points away on downside, 95 points on upside. We have exceeded those moves only once this year: to the downside on Feb 5th.

UVXY

#LongPuts #LEAPS #ShortCalls – Let’s give Mr. Market some incentive…

Sold UVXY DEC 28 2018 60.0 Call @ 3.35

UVXY

#LongPuts #LEAPS #ShortCalls – Rolling…

Rolled UVXY NOV 30 2018 54.0 Puts to DEC 7 2018 51.0 Puts @ .90 credit

IC for Monday

Entry:

Sell ES 12/3 2810×2820 Call Binary/Spread 1.00+ Credit

Sell ES 12/3 2675×2665 Put Binary/Spread 1.00+ Credit

Exit Stop Limit Loss: 3x credit per side

#spxcampaign Sell iron condor Nov…

#spxcampaign

Sell iron condor Nov 30 2760/2770 calls and 2740/1730 puts for $1 and 1 hour till expiration. Many missteps today, hope to get this one right.

Back home again after almost…

Back home again after almost 5 weeks of Hospital & Rehab with wife.

Hopefully all is well.

Econ Calendar for week of 12/3/18

Jobs Report is Friday morning

Link to Calendar: https://us.econoday.com/byweek.asp?day=3&month=12&year=2018&cust=us&lid=0

#shortcallspreads #shortstrangles TSLA AAL TSLA…

#shortcallspreads #shortstrangles TSLA AAL

TSLA sold Dec. 21, 380/385 for 1.05

AAL sold Jan. 18, 35/44 for 1.40

AMBA Earnings

#Earnings – Gave it shot. I’m great at getting stocks to make moves way outside expected. LOL Paying the extra penny to avoid the exercise fees.

Bought to Close AMBA NOV 30 2018 32/34/36 Iron Flies @ 2.01 (sold for 1.73)

TNA

#CoveredCalls – Keeping it pretty tight betting no major agreement over the weekend. Now we wake up Monday morning with TNA at 75…LOL

Bought to Close TNA NOV 30 2018 65.0 Calls @ .05 (sold for 1.55)

Sold TNA DEC 14 2018 65.0 Calls @ 2.36

TQQQ roll

BTC January 4, 49.5 calls @ 4.14

STO January 11, 50 calls @ 4.26

#earnings #closing #ironcondor NVDA Nov….

#earnings #closing #ironcondor NVDA

Nov. 15, sold 125/135/255/265 for 1.02. NVDA went as low as 133, now back to 160. Closed today for .62.

#earnings #closing #shortstrangles SPLK Bought…

#earnings #closing #shortstrangles SPLK

Bought strangle for 1.33, sold yesterday for 2.30

VixCentral.com is down

They’re aware and working on it but just wanted to let you all know in case you were checking and wondering what happened.

UPRO

#ShortPuts #IRA – Late fill…

Bought to Close UPRO DEC 21 2018 30.0 Put @.10 (sold for 1.05)

OLED

#ShortCalls – Just for safety taking these extras off…

Bought to Close OLED NOV 30 2018 94.0 Calls @ .37 (sold for .85)

Bought to Close OLED NOV 30 2018 95.0 Calls @ .17 (sold for 1.15)

AMBA Earnings

#Earnings #IronFlies – Let’s try it again…risk .27 to make 1.72. Two wide on a 3.90 expected move. Low risk, low probability, high reward.

Sold AMBA NOV 30 2018 32/34/36 Iron Flies @ 1.73

SPX 1-dte

#SPXcampaign Sold to Open $SPX Nov 30th 2690/2710/2810/2830 condors for .90. Expires tomorrow.

SPLK speculative trade

#Earnings Bought to Open $SPLK Nov 30th 102/107/109 #BrokenWingButterfly for 1.60.

This is a bullish trade. Breakeven at 103.60. No upside risk.

Max loss 1.60.

Max gain (if pin at 107) 3.40.

If it explodes above 109 gain will be 1.40.

TNA

#ShortPuts #IRA – With enough risk in Dec and Jan I’m looking out to Feb now. 21.5% annualized or a pretty good price to buy some stock if it gets there.

Sold TNA FEB 15 2019 50.0 Put @ 2.20

TNA

#ShortPuts #IRA – Just for risk reduction. Now hoping my 65 strike covered calls expire tomorrow. Threading the needle again. 🙂 🙂

Bought to Close TNA NOV 30 2018 60.0 Puts @ .10 (sold for 2.25)

#shortputs SLB Bottom feeding, sold…

#shortputs SLB

Bottom feeding, sold Dec. 7, 44 put for .44, stock at 46.14 ex-div next week.

Closing some SOXL

For greater than 50% of the profit.

Bought to close $SOXL Dec 21 85 put @ 2.60. Sold for 5.60 on 10/10.

#earnings #shortstrangles SPLK Sold Dec….

#earnings #shortstrangles SPLK

Sold Dec. 21, 80/120 strangle for 2.30, outside past max moves

Trump Xi meeting

From what I can find, it looks like their dinner is Saturday, which means markets may not be affected much tomorrow by the G-20 (unless other big news is generated). But it could mean a gap up or down on Monday. I’m guessing more likely up, as Trump will likely report that the meeting went well. But if his advisors are more bearish, as they usually have been on trade agreements, it could go anywhere.

SPLK earnings analysis

#Earnings I’m considering a bullish trade on SPLK… it has positive bias on earnings. Possible broken-wing BF with no upside risk.

$SPLK reports tonight. Below are details on earnings 1-day moves over the last 12 quarters.

Aug. 23, 2018 AC 14.81%

May 24, 2018 AC -5.20%

March 1, 2018 AC 9.26%

Nov. 16, 2017 AC 17.89% Biggest UP

Aug. 24, 2017 AC 8.47%

May 25, 2017 AC -6.97%

Feb. 23, 2017 AC -3.23%

Nov. 29, 2016 AC 0.41%

Aug. 25, 2016 AC -10.10% Biggest DOWN

May 26, 2016 AC 2.56%

Feb. 25, 2016 AC 7.73%

Nov. 19, 2015 AC -3.53%

Avg (+ or -) 7.51%

Bias 2.68%, positive bias on earnings.

With stock at 100.00 the data suggests these ranges.

Based on current IV (expected move per TOS): 89.71 to 110.29

Based on AVERAGE move over last 12 quarters: 92.49 to 107. 51

Based on MAXIMUM move over last 12 Q’s (17.9%): 82.11 to 117.89

Open for requests on other symbols.

Rolls and adjustments

#pietrades

TQQQ 63 cc rolled out to Jan 19 60 for 0.70 credit. CB now 58.4

TQQQ lot 2 65 cc rolled out and down to Jan 19 60 for 0.70 credit. Cb now 58.75

Just sit on these until rebound. If not will convert to #fuzzy later.

LNG 65 CC rolled down 8 DTE to 62 for 0.96 credit. CB 60.03 so will let assign next week. My plan with this account is to then start a live #lizardpies.

LNG lot 2 expires in 3 weeks at the 61 CC for cb 59.27. Same as above but will change ticker.

My #pietrades for the next few weeks will be LNG, GILD, EXPE, EOG, XBI, SMH. A few others I am watching but these will be the core trades for a while. Want to see chips and a few other names stabilize before adding.

#fuzzy

LNG 50/65 rolled out 43 DTE for 1.03 credit. Cb now 15.31 and 110 weeks left.

I have not taken a LEAP all the way to expiration in several years but I may do that with some of these smaller accounts to see what kind of annualized returns I can achieve. Hopefully 50-100% or more.

Have a ton of contracts expiring in 15 and 21 DTE so sitting on hands until then. At that point will add a few more live #lizardpies as I roll the #fuzzy and free up some cash.

4 things I noticed with the latest correction. If you own the stock can sit on it long term but the losses are much larger on paper than with spreads and takes a lot longer to get back to even.

The spreads help navigate the corrections and are easier to adjust, but everyone here probably already knew that.

Using longer options with the #pietrades 21-43 DTE prevents a lot of assignments and easier to roll. Also helps handle the volatility easier.

Once VIX settles down (under 15) will always leave on an SPX or /ES hedge lottery ticket to cover about 10% correction for the account. Probably finance it by selling a LEAP on something I want to own long term.

Finally a slight bump in my equity curve after being down/flat for the last 8 weeks 🙂

BOIL

#BearCallSpreads – Surprised I got filled on this one. Better than yesterday even with the stock down a little.

Sold BOIL MAR 15 2019 50.0/60.0 Bear Call Spread @ 3.25

#jeff SPX call spread Are…

SPX call spread

Are you still holding $SPX Dec 7th 2720/2745 call spreads?

#earnings #shortstraddle GME Sold Dec….

#earnings #shortstraddle GME

Sold Dec. 21 15 straddle for 2.20, thanks Jeff

UNG

DLTR Earnings

#Earnings #IronFlies – Not looking like it’s gonna come back so taking a tiny loss instead of small loss…LOL Now I can try again in something else. On the bright side the pin action is carrying over to DG although I think DG is a much better store. 🙂

Bought to Close DLTR NOV 30 2018 80.5/83.5/86.5 Iron Flies @ 2.70 (sold for 2.59)

OLED

#ShortCalls #BullPutSpreads – Replacing this week’s with a half size for now…

Sold OLED DEC 7 2018 98.0 Calls @ .72

GME earnings analysis

#Earnings $GME reports tonight. Below are details on earnings 1-day moves over the last 12 quarters.

Sept. 6, 2018 AC 0.06%

May 31, 2018 AC 3.93%

March 28, 2018 AC -10.81%

Nov. 21, 2017 AC 3.82%

Aug. 24, 2017 AC -10.92%

May 25, 2017 AC -5.92%

March 23, 2017 AC -13.60% Biggest DOWN

Nov. 22, 2016 AC 8.08% Biggest UP

Aug. 25, 2016 AC -10.63%

May 26, 2016 AC -3.93%

March 24, 2016 AC -0.59%

Nov. 23, 2015 BO -4.20%

Avg (+ or -) 6.37%

Bias -3.73%, significant negative bias on earnings.

With stock at 14.90 the data suggests these ranges.

Based on current IV (expected move per TOS): 13.49 to 16.31

Based on AVERAGE move over last 12 quarters: 13.80 to 15.68

Based on MAXIMUM move over last 12 Q’s (13.6%): 12.74 to 16.74

Open for requests on other symbols.

AMBA earnings analysis

#Earnings $AMBA reports tonight. Below are details on earnings 1-day moves over the last 12 quarters.

Aug. 30, 2018 AC -3.62%

June 5, 2018 AC -12.93%

March 1, 2018 AC 13.46%

Nov. 30, 2017 AC 14.29% Biggest UP

Aug. 31, 2017 AC -22.35% Biggest DOWN

June 6, 2017 AC -10.24%

Feb. 28, 2017 AC -4.42%

Dec. 1, 2016 AC -11.27%

Sept. 1, 2016 AC -6.67%

June 2, 2016 AC 9.39%

March 3, 2016 AC -8.93%

Dec. 3, 2015 AC -1.64%

Avg (+ or -) 9.93%

Bias -3.74%, negative bias on earnings.

With stock at 34.30 the data suggests these ranges.

Based on current IV (expected move per TOS): 29.86 to 38.74

Based on AVERAGE move over last 12 quarters: 31.04 to 37.88

Based on MAXIMUM move over last 12 Q’s (22.4%): 26.76 to 42.16

Open for requests on other symbols.

DG

#ShortCalls #BullPutSpreads – Re-loading for earnings. Nice bounce is allowing a sale at 1.5x the expected move and well above the all time high. I may adjust this down prior to the announcement. Selling against bull put spreads.

Sold DG DEC 7 2018 122.0 Calls @ .60

UVXY

#LongPuts #LEAPS #ShortCalls – Selling a call now against where I will hopefully be able to sell a new batch of puts tomorrow. Ratio is now 16 long puts against 8 short puts against 3 short calls (calls spread out to only one per week for safety). Trying to generate as much cash as possible over the next 111 weeks.

Sold UVXY DEC 7 2018 60.0 Call @ 2.30

SQ calls rolled

#LongLEAPs #SyntheticCoveredCalls Rolled $SQ Nov 30th 66 calls to Dec 7th 67 calls for .10 credit

Earnings today

#Earnings A list of Bistro favorites… AMBA, GME, PANW, SPLK, VMW, WDAY. Not sure if I’ll be trading any, but let me know if you’d like analysis on any or all.

TQQQ

I rolled the 49 calls in December 21 out to February 54 calls for a credit of .15 cents. I was having some margin problems since I was long the 60 calls in 2021 and short the 49 calls in December.I am giving up 8 weeks of rolls but had 38 weeks covered so far.

#assignment again X Assigned on…

#assignment again X

Assigned on a 35 put, originally sold in May and rolled, cost basis of 31.37. Sold Dec. 7, 24.50 call for .28

#earnings #shortstrangle DLTR bought strangle…

#earnings #shortstrangle DLTR

bought strangle for .38, sold yesterday for .97.

ANF partially closed

#Earnings #LongStraddle Sold to close $ANF Nov 30th 17 calls for 4.20. Sold half of my position. Holding the other half to see how the morning shakes out. Bought the straddle yesterday for 2.58.

#closing #butterfly NFLX November 9,…

#closing #butterfly NFLX

November 9, sold Dec. 21, 250/260/265 put butterfly, closed today for a gain of .25 (edited)

DLTR Earnings

#Earnings #IronFlies – As usual…low risk and low probability but good reward if it works. Risk .41 to make 2.59 playing 3 wide on a 5.90 expected move.

Sold DLTR NOV 30 2018 80.5/83.5/86.5 Iron Flies @ 2.59

ANF trade

#Earnings Bought to open $ANF Nov 30th 17 #LongStraddle for 2.58.

TQQQ

#LongCalls #LEAPS – Lots of time left on this one so taking the small loss since it’s getting a little DITM and sold below the LEAPS.

Bought to Close TQQQ NOV 30 2018 47.0 Calls @ 2.90 (sold for 2.50)

TNA

#LongCalls #LEAPS – Just in case this rally has any follow through tomorrow I’m getting out of the way with a decent weekly profit. Looking to re-load higher at some point.

Bought to Close TNA NOV 30 2018 63.0 Calls @ 1.01 (sold for 2.45)

TQQQ

Rolled the 55 puts in January 2019 out to January 2021, 45 puts for a credit of 5.55

TQQQ

In my IRA, rolled December 21, 49 calls out to January 4, 49.5 calls for a credit of .35 cents. I am long the 60 calls in 2021 but now only need 9.33 cents to break even each week from January 4

UVXY

#LongPuts #LEAPS #ShortCalls – Even though UVXY is down today, it’s still historically high so booking and re-selling. Hoping to add another on any decent pop.

Bought to Close UVXY NOV 30 2018 60.0 Call @ .24 (sold for 4.40)

Bought to Close UVXY DEC 7 2018 70.0 Call @ .42 (sold for 4.10)

Sold UVXY DEC 14 2018 60.0 Call @ 2.25

#ironcondor CRM TastyTrade idea, sold…

#ironcondor CRM

TastyTrade idea, sold Jan. 18, 105/115/155/165 for 1.57.

#earnings #shortstrangles DLTR Sold Dec….

#earnings #shortstrangles DLTR

Sold Dec. 21, 70/95 strangle for .97, right at the max 1 day ranges.

BOIL

#BearCallSpreads – Adding one. Sold the first one into the panic for 4.27. Gonna be hard to match that…

Sold BOIL MAR 15 2019 50.0/60.0 Bear Call Spread @ 3.00

DG

#ShortCalls #BullPutSpreads – Just for safety booking a small gain on the weekly sale. I’ll reload for earnings next week…

Bought to Close DG NOV 30 2018 110.0 Calls @ 1.70 (sold for 2.00)

DLTR earnings analysis

#Earnings $DLTR reports tomorrow morning. Below are details on earnings 1-day moves over the last 12 quarters.

Aug. 30, 2018 BO -15.54% Biggest DOWN

May 31, 2018 BO -14.28%

March 7, 2018 BO -14.47%

Nov. 21, 2017 BO 2.41%

Aug. 24, 2017 BO 5.62%

May 25, 2017 BO 0.92%

March 1, 2017 BO 0.20%

Nov. 22, 2016 BO 8.15%

Aug. 25, 2016 BO -9.93%

May 26, 2016 BO 12.77% Biggest UP

March 1, 2016 BO 2.21%

Nov. 24, 2015 BO 6.62%

Avg (+ or -) 7.76%

Bias -1.28%, negative bias on earnings.

With stock at 83.30 the data suggests these ranges.

Based on current IV (expected move per TOS): 77.28 to 89.32

Based on AVERAGE move over last 12 quarters: 75.64 to 88.36

Based on MAXIMUM move over last 12 Q’s (15.5%): 69.26 to 94.74

Open for requests on other symbols.

TQQQ calls

#LongLEAPs #SyntheticCoveredCalls Sold $TQQQ Dec 7th 51.5 calls for 1.25.

LABU

I rolled the rest of my 61 calls in December 14, to January 18, 65 calls for a credit of .70 cents.

ANF earnings analysis

#Earnings I’m including this one because of my interest in a long straddle. The cost of an ATM straddle is about 2.60, which would be about a 15% move in the stock, which is its AVERAGE move over recent quarters. I’ll consider whether to sell in the last hour.

$ANF reports tomorrow morning. Below are details on earnings 1-day moves over the last 12 quarters.

Aug. 30, 2018 BO -17.15%

June 1, 2018 BO -8.72%

March 7, 2018 BO 11.90%

Nov. 17, 2017 BO 23.90%

Aug. 24, 2017 BO 17.06%

May 25, 2017 BO 8.99%

March 2, 2017 BO 13.94%

Nov. 18, 2016 BO -13.76%

Aug. 30, 2016 BO -20.30% Biggest DOWN

May 26, 2016 BO -15.66%

March 2, 2016 BO 3.64%

Nov. 20, 2015 BO 25.03% Biggest UP

Avg (+ or -) 15.00%

Bias 2.41%, positive bias on earnings.

With stock at 17.25 the data suggests these ranges.

Based on current IV (expected move per TOS): 14.60 to 19.90

Based on AVERAGE move over last 12 quarters: 14.66 to 19.84

Based on MAXIMUM move over last 12 Q’s (25.0%): 12.93 to 21.57

Open for requests on other symbols.

SPX 1-dte

#SPXcampaign Still working on this new approach… thought I’d share my big error on today’s spread.

I sold the $SPX Nov 28th 2590/2610-2710/2730 for 1.15 yesterday at 1:38p ET, when SPX was at 2672.

After selling, the SPX creeped higher into the close. Even so, my call spread side did NOT increase much. With the threat of a gap up opening, and a slow rise into the close, I could have closed the calls for about .70, and let puts expire today, for an overall profit on the trade, same day. But it didn’t rise enough to hit my stop, so I opted to stay in.

That turned out to be only a minor error: Consider taking profits same day if volatility drops enough in the last hour to exit with decent profit, and erase overnight risk. But, in this case, the gap up this morning wasn’t bad, and I could have closed at the open for a small loss.

Further more, my call side DID hit its stop this morning, when the expected move touched my 2710 short calls. This means I should have exited, and COULD have exited for a profit on the fade back down to 2685 area. But I didn’t. And as it bounced, I was not focused…. I should have realized the volatility risk with Powell’s comments, but I didn’t and was focused on record keeping and other non-trade issues.

Now I’m 10 points ITM. Faced with possibility of a chunky loss if there’s no fade. Don’t know how I’ll roll yet.

1. Take partial profits if they present themselves early.

2. Follow rules even if you believe that waiting for better exits will work.

3. Focus on market events you KNOW are coming. Don’t get distracted or complacent.

Not sure if there is…

Not sure if there is anything wrong with the site or is it just no posts? Last one was 2 hours ago.

CRM closed

#Earnings Closed $CRM 138/143 call spreads for .51. Closed short 118 puts for .04. Leaving long 113 puts as lottery ticket.

Condors sold yesterday for 1.09.

#earnings #closing #shortstrangles WB CRM Yesterday…

#earnings #closing #shortstrangles WB

WB Yesterday sold Dec. 21, 45/75 strangle for 1.45, bought today for .70.

CRM Yesterday sold Dec. 21, 105/145 strangle for 1.73, bought today for 1.20.

I’ve been using max move strikes from Jeff’s info, going out in time to get over 1.00 in premium, just a couple have bombed.

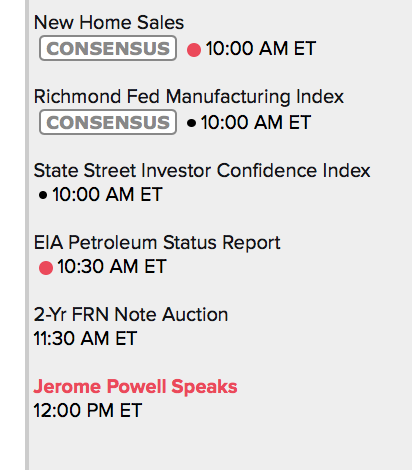

Fed’s Powell, and other market movers

Busy day; market movers with red dot.

Closed Z door

#Earnings #Assignment Closed remaining $Z stock, selling at 34.90. Cost basis 32.55. Waited for a couple weeks for stock to return to profit zone, and exited all this week.

Since we are on experiment…

Since we are on experiment discussion below again, here is one I have been paper trading. A twist on #pietrades. If we need a new term we could call them #lizardpies.

So obviously with the market rout all my #pietrades went ITM and to prevent a meltdown in margin I converted them all to #fuzzy. Which is great, has controlled the volatility and still have 111 weeks to manage them. But as @fuzzballl points out below, they are expensive. Cheaper than stock but my EXPE puts are now trading at 22.40 and 19.50. Not chump change.

The #pietrade idea is sound for income generation and even some capital gains long term as long as you sell the call ATM or OTM once assigned the stock. You also are typically only selling 1 side and as Karen the supertrader (now scam artist) figured out, selling the other side is what really improves long term returns and consistency. She may have been using some creative accounting but the idea is sound and has been proven by tasty trade.

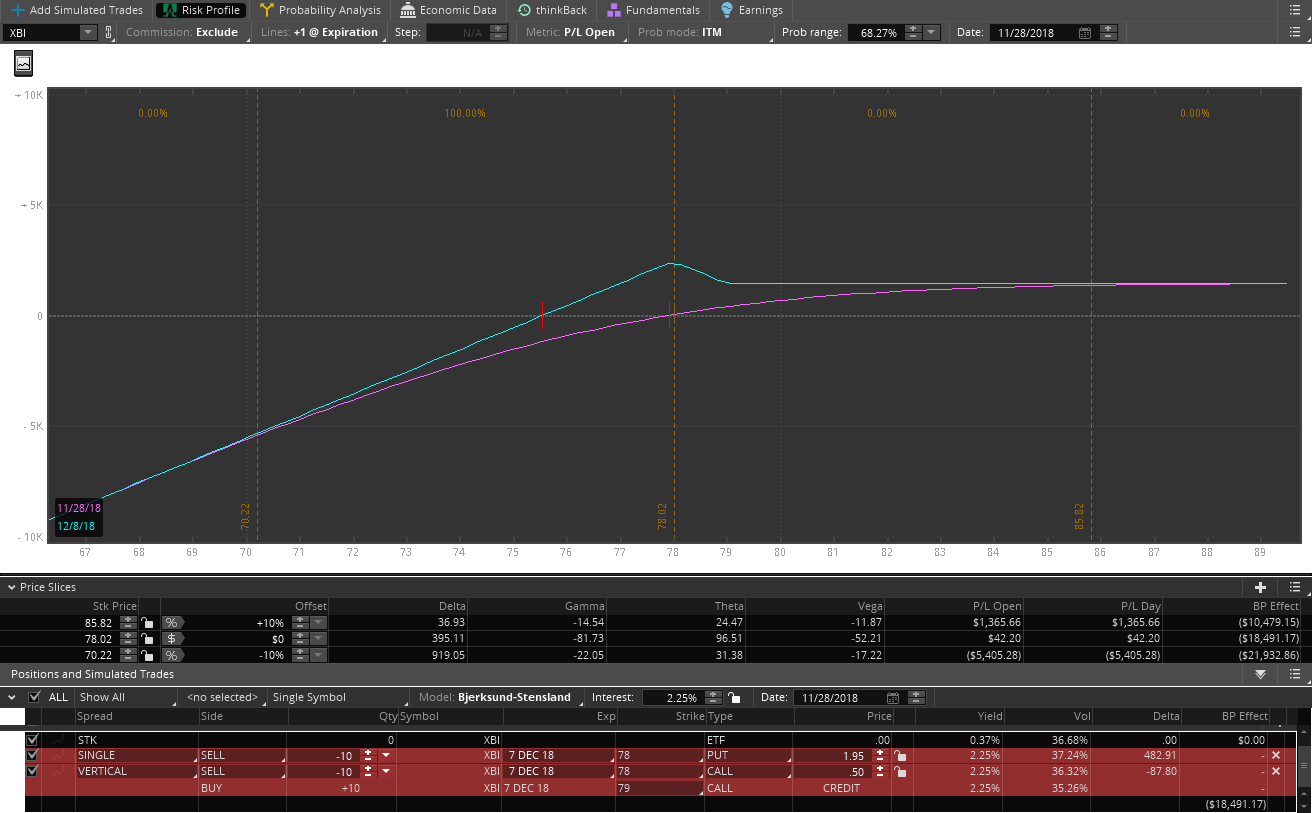

So here is the tweak I have been playing with. When you set up the trade, start it as a #jadelizard but set it up ATM. For example with XBI currently at 78.02 I would sell the 10 DTE 78 puts naked (cash secure) and then sell the 78/79 call credit spread. Total credit 2.55. No upside risk, downside break even is 75.55 which is lower than where I probably would have just sold the put.

3 possible outcomes

a: below 78 assigned shares on the put at 78 but cost basis 75.55. Can sell a next week call or call credit spread if you think rebound, then uncapped upside

b: Between the strikes max profit and you may be assigned on the call but can exercise your long call if needed.

c: above 79 everything cancels out and you keep the credit minus $1.

Here’s a graph on a 10 lot.

I have been trading it on paper and it would have had better loss control on the #pietrades than straight put sales the last 2 months.

Thoughts, holes in the strategy, other ideas to tweak it or make it better? If you wanted to be more conservative could sell strangles OTM instead or straddles ATM on the short sides but then less credit. Since my premise is income, I am trying to bring in as much credit as possible on the front end.

CRM trade

#Earnings Sold to Open $CRM Nov 30th 113/118/138/143 condors for 1.09. Leans slightly bullish.

Long Calls, LEAPS and a Fuzzy twist…

I’ve got a couple experiments going on that are kind of interesting. They came out of long term positions where the weekly calls got run over. I booked the LEAP calls for gains and then rolled the run over weekly calls into bull put spreads and continued selling against them.

While doing this I’m beginning to wonder if that would be a reasonable way to play something long term without having to buy anything. (nothing out of pocket 🙂 🙂 )

For instance let’s look at WYNN. A stock that’s pulled back a lot with great weekly premium.

How about selling a Jan 2021 ITM 140/110 bull put spread for 18 bucks. 30 wide for 18 bucks so the max risk is 12 dollars. Sell weekly calls against the spread for the next two years only needing to cover the 12 dollars to have a risk off trade. What could happen long term?

1. Stock rallies then all good (assuming weeklies aren’t in trouble)

2. Stock tanks but you easily cover the risk with weekly sales.

3. A combination of both where selling just 50 cents a week makes 44 dollars profit at the end no matter where the ITM spread ends up.

I think I like these since they can be done without any cash outlay and the minimum required to cover the risk is considerably less (Jan 2021 LEAP calls are 25 dollars so over twice the risk of the ITM spread). Profit is “sort of” capped but that’s ok. The real money is in the weekly sales anyway.

Whaddya think?

SPX 1-dte sold

#SPXcampaign Sold $SPX Nov 28th 2590/2610-2710/2730 condors for 1.15. Expires tomorrow.

#coveredputs #shortstock #rolling CLR Nov….

#coveredputs #shortstock #rolling CLR

Nov. 14, sold short 100 shares at 45.94. Nov. 15 sold a Nov. 23, 46 put for .60, Nov. 20 rolled it to Nov. 30 for 2.56, rolled it today to Dec. 7, have net 185 in premium, CLR is at 44.33.

#earnings #shortstrangles CRM Sold Dec….

Sold Dec. 21, 105/145 for 1.73, thanks again Jeff.